Markets are waiting for clearer signals from the data to move their cut discounts. Until then, curves can still flatten, with officials reluctant to provide guidance. French spreads are still elevated but don’t look excessive, with political uncertainty more likely to remain even after the elections.

Still waiting for clearer signals from the data

10-year US Treasury yields are probing the downside towards 4.20% but overall, rates markets remain rangebound ahead of Friday’s big releases and the looming political risks. The few data points we have received in the last session have been inconclusive, with the Conference Board’s consumer confidence falling only subtly to 100.4, thus still staying above estimates.

Commentary from Federal Reserve speakers was slightly on the hawkish side, with Michelle Bowman warning of upside risks and shifting her view on rate cuts to 2025. We still think there is a good chance that the pieces will fall into place for rate cuts as early as September, but for now, such cautionary tones can see the curve flatten until data provides a clearer signal.

Eurozone political uncertainty likely to last beyond the French elections

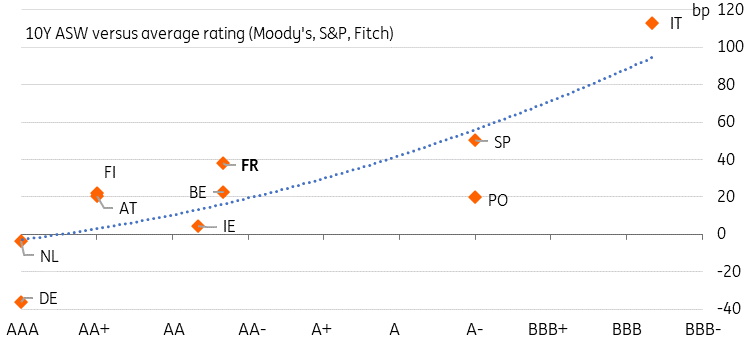

The situation surrounding the upcoming French elections remains stable, with spreads consolidating at somewhat elevated levels. As before, French spreads are the ones that stand out, which also becomes clear when looking at a plot of government bonds’ 10Y ASW levels versus their average sovereign rating. The French data point, which used to sit alongside its Belgian peer, is displaying a clear discount, which would actually be more in line with a rating one notch lower around ‘A+’. The fact that spreads are in line with ratings just one notch lower means we do not think spreads have much narrowing potential given the uncertain outlook.

France's ratings were lowered to ‘AA-‘ last year by Fitch and only shortly before the election by S&P also to ‘AA-‘. Part of the rationale for that latest downgrade was the political fragmentation and uncertainty, along with higher deficit expectations. The outlooks on these ratings are ‘Stable’. Arguably, that situation is now becoming more acute, but while markets are discounting France’s growing struggles to rein in deficits, rating agencies will likely wait to see how any new government will interact with the EU fiscal rules. Moody’s still rates France one notch higher at ‘Aa2’ and had already warned soon after the snap elections were called that this was credit negative with the outlook possibly lowered from its current Stable status if the country’s debt metrics were to deteriorate further. Clearly, markets would not be surprised now.

Excessive deficits proceeding? The market's discount of French credit deterioration

Source: Refinitiv, rating agencies, ING

Today’s events and market view

It is a quiet day in terms of data releases with the US releasing only its mortgage applications and new home sales numbers. The main focus, therefore, will be the European Central Bank speakers scheduled for today, including the central bank’s chief economist Philip Lane.

In primary markets, the US will sell a new 5Y note today for US$70bn alongside reopening a 2Y floating rate note. The UK tops up a 14Y gilt for £3bn.

More By This Author:

FX Daily: Don’t Forget Policy Divergence

The Commodities Feed: US Oil Stocks Build

Asia Morning Bites For Wednesday, June 26

Comments

Log in or sign up to join the conversation.