Weak economic data dents the European Central Bank’s ability to push rates up. Even if July and September hikes were fully priced in, Bund and swap will find it hard to rise above the top of their recent range. Direction is far from clear, but our preference is to position for upward pressure on yields.

Soft economic data dents ECB hawkish rhetoric

For financial markets, a flurry of weak economic activity data – most prominently in the manufacturing sector such as yesterday’s German factory orders and today's industrial production – sits awkwardly with the European Central Bank's (ECB) message that more monetary tightening is needed. The pre-meeting quiet period starts tomorrow, making today the last opportunity to skew investor expectations but markets pricing a 25bp hike at this meeting are unlikely to move much. Another important clue as to future policy moves will be in the staff forecasts released at the same time as next week’s policy decision. The 2025 headline and core inflation projections at the March meeting stood at 2.1% and 2.2% annualized, above the ECB’s target and a clear signal that more tightening is needed – even above and beyond the path for interest rates priced by the market in late February.

Dovish-minded investors can point to a decline in oil and gas futures since the March meeting, as well as a downtick in consumer inflation expectations in the most recent survey released yesterday. Will this be enough for the ECB to no longer signal that it has ‘more ground to cover’? Probably not, but markets may not care. The focus among hawks is squarely on core inflation and the modest decline from a 5.7% peak in March to 5.3% in May hasn’t been met with much relief by the Governing Council, but it has pushed euro rates down relative to their dollar peers.

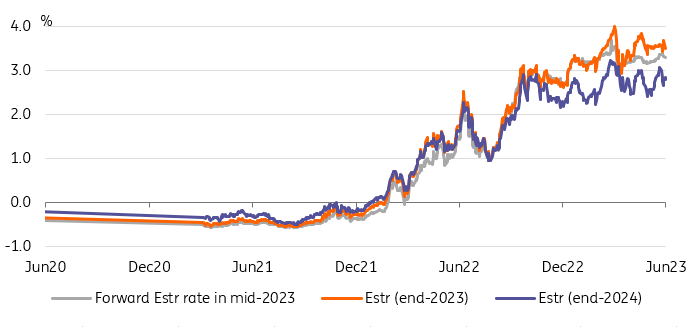

Estr forward swaps never managed to rise above their February levels

Refinitiv, ING

The recent range is a tough ceiling to break for euro rates

Even if ECB hawks continue to talk up the odds of July and September hikes, with the former still flagged as a more than even probability even by centrist members, it will take a pick-up in activity data for markets to price a terminal rate above 4%, as they did before the Silicon Valley Bank failure in March. We’re not expecting a huge change in communication in short, and markets will focus on changes in economic data instead to infer how many more hikes the ECB has under its belt. In that context, we think longer-dated rates struggle to break above the top of their recent range, which roughly sits at 2.54% for 10Y Bund and 3.16% for 10Y swaps against 6m Euribor.

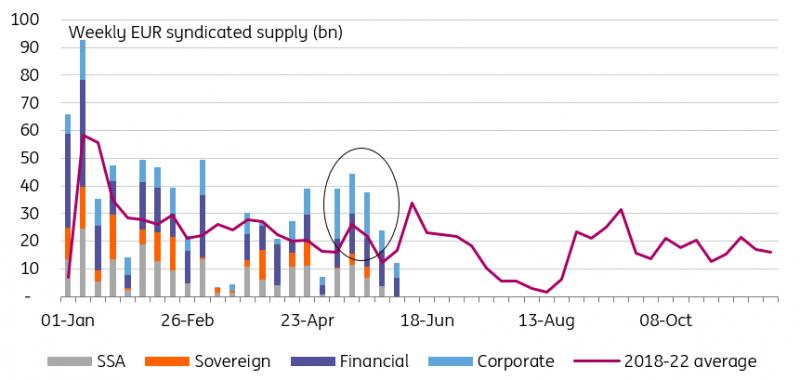

In light of the current lack of direction in financial markets, these levels may seem difficult to achieve, but the pre-ECB and Federal Reserve meeting lull is proving a fruitful time for primary market activity. On the sovereign side, Spain and France announced deals yesterday which we think will add to other deals in pushing yields up today. Taking a step back, May has seen issuance volumes above historical averages every single week as opportunistic borrowers used this window of calm to push deals. We don't think this week will be any different. This shouldn’t be mistaken for a conviction macro trade, but we think the benign market conditions should continue to result in higher bond yields and weaker safe havens as investors feel more comfortable with owning riskier alternatives.

Every week since May supply has been higher than historical averages

Bond Radar, ING

Big debate on direction from the US. We look for upward pressure on yields for now

In the US, there is a stark juxtaposition between strong ongoing payroll growth versus PMIs and ISMs entering recessionary territory (low 40s for some components of the manufacturing PMI). On the inflation front, there is evidence of more subdued pipeline pressure while core inflation remains elevated (in the area of 5%).

Our model for US "rates" pitches fair value at 6% when we take everything into account. That has drifted up from 5.75% in the past week or so. Relative to this, the funds rate (ceiling at 5.25%) is not too deviant from that. But longer tenor rates are quite low relative to the big figure of 6%, reflecting ongoing deep inversion of the curve.

While there are some good reasons to expect market rates to fall (weak PMIs for example), our preferred expectation from here is to see some further upward pressure on market rates first. The 4% area for the 10yr Treasury yield for example remains a generic target that could well be hit in the coming month or so.

Today’s events and market view

Today’s session should be relatively light on economic releases with only US trade standing out. Instead, we expect the focus to be on the Bank of Canada’s meeting in the afternoon. Consensus is for no change in policy rates but the surprise Reserve Bank of Australia hike yesterday, as well as a greater skew towards a hike in the most recent contributions to the Bloomberg survey, means markets are on high alert.

Bond supply will be concentrated in the 3Y sector with sales from the UK and Germany (a green bond in the latter’s case). Spain and France mandated banks for the sale of 10Y and 15Y linker bonds via syndication.

ECB speakers on the last day before the pre-meeting quiet period will be VP Luis de Guindos, Klass Knot, Fabio Panetta, and Boris Vujcic.

More By This Author:

The Commodities Feed: China’s Imports RecoverFX Daily: A Close Call On The Bank Of Canada Today

Australia’s Reserve Bank Lifts Cash Rate Again

Comments

Log in or sign up to join the conversation.