Rates Spark: Can’t Keep A Bund Down

The bond market rally is returning with a vengeance. Lower implied volatility and inflation expectations justify the move but we think the macro underlying assumptions are questionable

The ‘everything rally’ resumes…

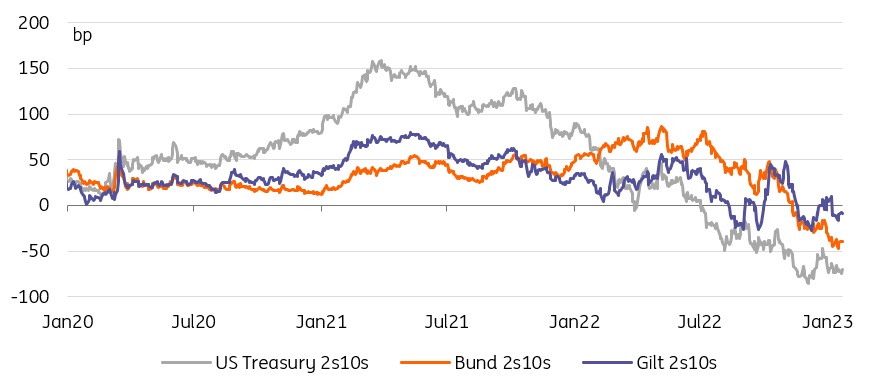

Government bond markets, and rates in general, continue to display a strong bias toward greater risk appetite. This is visible in the outperformance of longer-dated bonds over their shorter counterparts, for instance, the flattening of the 2s10s curve. This is also evident in the tightening of various credit spreads, not least sovereign spreads.

ECB officials, have called into question the macro assumptions that underpin this ‘everything rally’

We, and more importantly European Central Bank officials, have called into question the macro assumptions that underpin this ‘everything rally’, from risky stocks to safe government bonds. In short, the fall in energy prices and so better growth prospects reduce the downward impact that negative real wage growth should have on core inflation. In simple terms, either the economy converges to higher growth, a higher inflation regime that would be positive for some risk assets but not for core bonds, or growth disappoints and inflation converges lower but then risk assets are under threat and core bonds continue to rally. The current Goldilocks macro environment is more likely to be a temporary state of affairs.

Flatter yield curves this year also reflect a better appetite for duration

Image Source: Refinitiv, ING

… despite our, and central bank, caution

Along these lines, Gediminas Simkus shared his view yesterday that not all of the past energy price jump has yet fed through to core inflation. His prime concern, which we assume is shared by other hawks, is that more wage gains are in the pipeline, thus lengthening the time it will take for inflation to revert to the ECB’s 2% target.

More wage gains are in the pipeline

Looking at the PMIs released yesterday, his fears are justified. Respondents reported higher selling prices despite lower input costs, in part to reflect higher wages. Higher employment growth will do little to ease these concerns. This of course is only one data point, and responses to the more manufacturing-orientated Ifo survey to be released today will be informative. Note also that German Manufacturing PMIs yesterday surprised to the downside, unlike other sectors and other countries.

Declining implied rates volatility and inflation expectations explain improving risk appetite in euro markets

Image Source: Refinitiv, ING

Back to first principles: inflation and volatility explain the rally

We continue to think the everything rally is liable to reverse but there are very few signs of that yet. Going back to the first principles, the regain in risk appetite seems to be justified by the lower forward-looking view on implied rates volatility (derived from options) and by lower market inflation expectations (derived from inflation swaps). The first explains why investors have no qualms about buying assets with lower rates of return, ie lower yields, given the more benign environment expected. The latter also illustrates why markets are happy to challenge central banks’ hawkish tone.

Investors have no qualm buying assets with lower rates of return

None of this precludes a bond sell-off but at least it shows no obvious discrepancy within rates markets. It is easy to see when rates are falling too low compared to, for instance, our central bank call. It is more difficult (to us at least) to point to mispricing in riskier asset classes so our suspicion is that they may well outperform once rates have converged to the most dovish scenario and don’t have much further to drop. This in our view will only be a temporary state of play, however.

Today’s events and market views

Today’s German Ifo should confirm the improvement in sentiment visible in Zew and PMI surveys, and in the ‘everything rally’ that characterized markets in January. Note however that German manufacturing has been one of the few areas where PMIs disappointed yesterday.

Germany is scheduled to sell 15Y and 20Y debt in a week that has already seen plenty of long-end core supply (from the Netherlands and the EU yesterday). Spain mandated banks for the sale of a new 10Y benchmark via syndication.

Other data releases include US mortgage applications.

More By This Author:

Eurozone PMI Improves As Mild Winter Helps EconomyFrench Companies Expect Just A Short-Lived Economic Slowdown

FX Daily: PMIs Lead The Way

Disclaimer: This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information ...

more