Rates: Pricing A Dovish Shift From The ECB

Rates markets are going into the March European Central Bank meeting looking for a dovish bias. Unless all ECB tightening is off the table, something that will take time to assess, we expect the dip in euro rates to be temporary. Even with a more dovish ECB, however, peripheral bonds are in a precarious position.

What rates markets will be watching at this meeting

Euro rates are having a hard time establishing a new range. If we were to simplify, we would say that markets are torn between pricing two radically different scenarios; one where the hit to the eurozone economy from the war in Ukraine is severe enough to remove the need for policy tightening altogether, and one where tightening is merely delayed.

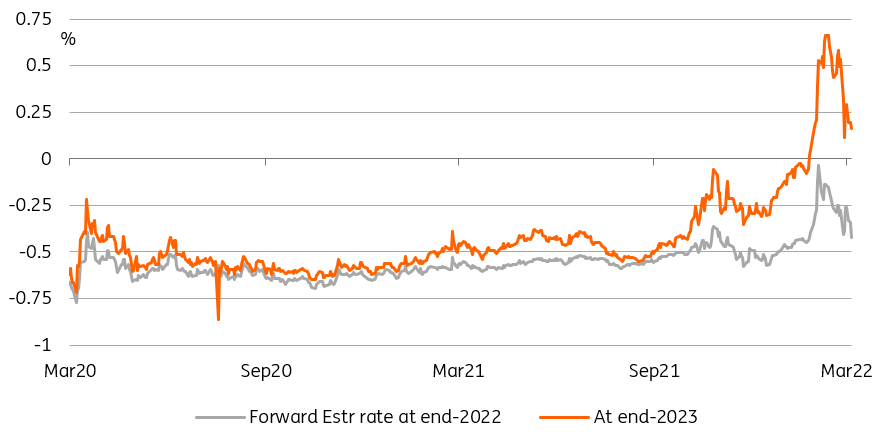

The euro curve has sharply lowered the hikes it expects from the ECB

Source: Refinitiv, ING

According to our economics team, markets are unlikely to get answers to this question. The ECB is in the same position as every economic forecaster, only with far more staff. It can only guess what the impact to growth will be, especially since it depends on whether geopolitical tensions rise again. Even with a central bank trying as hard as it can to keep its options open, investors will be tempted to find signals in its forecast.

With inflation likely to stay well above target for a while, the key question, as raised by ECB member Mario Centeno last week, is whether the hit to growth makes second-round effects more or less likely. As a result, the focus will be squarely on the 2023 and 2024 core inflation projections. If they are at 2% or above, markets will conclude that ECB tightening is on track, even if its timing is uncertain. There has been a clear dovish bias in the way rates have reacted to ECB communication since the beginning of the Ukraine invasion. Any core HICP forecast below 2% would allow markets to retain that bias.

Core rates: as long as there’s hikes

For the 10Y Bund, the line separating the two scenarios seems to be 0%. We regard this symbolic level as an unhappy medium between two worlds that have little in common. In the adverse scenario, flight to safety, and an economic hit to growth serious enough to rule out tightening in the foreseeable future, would justify yields settling durably in negative territory. This isn’t our base case.

Negative German yields are justified only if ECB tightening is entirely off the table

Source: Refinitiv, ING

Our base case is that policy normalization is merely delayed and that the ECB will raise the deposit rate to at least zero. The prospect of the ECB calling time on its negative interest rates policy (NIRP), even if this occurs one or two quarters later than the market envisioned last month, means negative yields are a thing of the past. We can conceive that a flight to safety, and bond scarcity, keeps Bund yields below the 0% line for some time if geopolitical tensions remain high, but we think they will rise eventually. This is all the more true as a hawkish Fed ensures there is an upward drift in core yields globally.

Peripheral debt: careful what you wish for

The set of circumstances that would justify durably tighter peripheral spreads is harder for us to picture. Consider that the spread tightening that occurred since the onset of the war in Ukraine has only come as a result of delayed ECB tightening hopes. In the event that tapering is only delayed by a quarter or two at most, as we think will be the case, we struggle to see how the situation is fundamentally changed. At a push, we can imagine carry traders enticed by the benefit of holding riskier bonds for one or two quarters longer but one has to be mindful of the broader context.

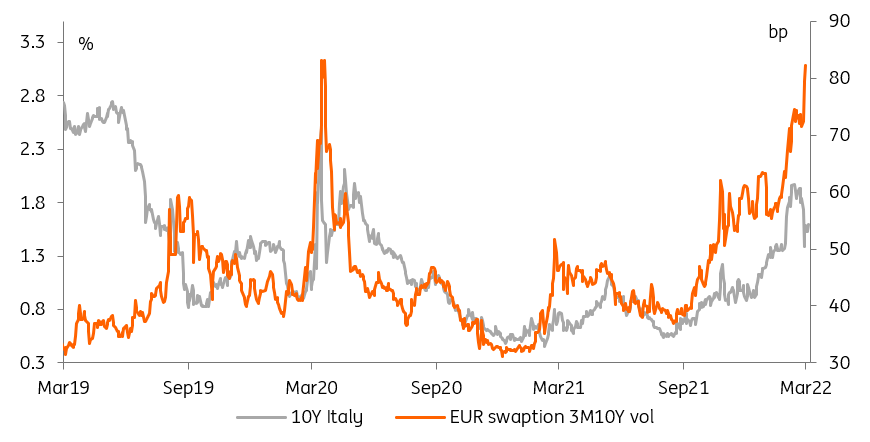

Peripheral yields and rates volatility have moved in opposite directions

Source: Refinitiv, ING

The broader context is that the only reason markets re-priced their ECB tapering expectations is because of a sharp escalation in geopolitical tensions, and their economic impact. The same drivers have seen a sharp jump in rates volatility, and a sharp widening of credit spreads, not to mention the underperformance of equities. All these factors normally go hand in hand with wider peripheral spreads. Ultimately, all sovereign bond valuations care about is quantitative easing and a mere one- or two-quarter delay to its end does not fill us with confidence that the wider macro backdrop can be safely ignored by peripheral debt. A positive correlation between core and peripheral debt cannot be taken for granted.

Disclaimer: This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information ...

more