Image Source: Pexels

Headline inflation moderated in November thanks to a high reference base in fuel prices last year, but the decline was only temporary. At the end of the year, CPI inflation is projected to bounce back to 5% YoY and continue rising in the first quarter of next year. We expect the National Bank of Poland to deliver its first rate cut in the second quarter of 2025.

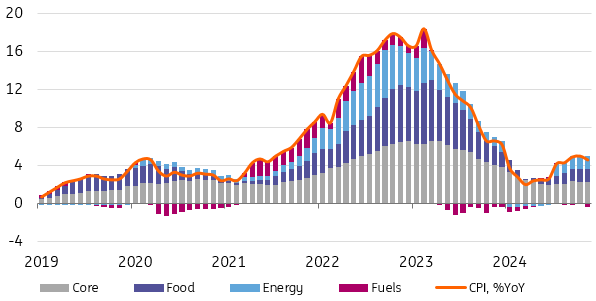

As expected, Polish CPI inflation eased in November to 4.6% year-on-year from 5.0% YoY in October. This was mainly due to the high reference base from fuel prices, which increased by 8.8% month-on-month in November last year following the end of promotions in September and October. This November, fuel prices rose by 2.3% MoM, and the contribution of fuel prices to annual inflation was -0.4 percentage points, compared to 0.0ppt in October.

November was another month of rising food prices. They increased by 0.7% MoM, the same as in October but slightly lower than the same time a year ago (0.9% MoM). Energy prices remained at the same level in November as in the previous month. We estimate that core inflation (excluding food and energy prices) did not change significantly compared to October, amounting to 4.1-4.2% YoY.

CPI down in November on high reference base in fuel prices

%YoY, percentage points

Source: GUS, ING

The decline in inflation in November is a temporary phenomenon. In December, we expect that inflation will return to around 5% YoY. We project that it will rise in the first quarter of 2025, which will prevent the Monetary Policy Council from beginning its monetary easing cycle until then. We expect the first rate cut to occur in the second quarter of next year once the Council is convinced that the inflation trend has reversed and it will head towards the central bank's target in a systematic and sustainable manner. In 2025, National Bank of Poland (NBP) interest rates may be reduced by a total of approximately 100bp.

More By This Author:

FX Daily: Limited Activity Amid Diverging SignalsAsia Morning Bites For Friday, Nov 29

Asia Week Ahead: PMIs And CPI Data Take Centre Stage

Comments

Log in or sign up to join the conversation.