Image source: Pixabay

The increase in Polish headline inflation in December turned out lower than market consensus as food price growth came in below expectations. The slight increase in annual CPI inflation stemmed mainly from a slower decline in gasoline prices. Inflation is projected to moderate in the second half of 2025, giving the MPC space for monetary policy easing this year.

According to the flash estimate, Poland's CPI inflation increased to 4.8% year-on-year in December from 4.7% YoY in November, in line with our forecast and well below the market consensus of 5.0% YoY. This slight increase stemmed from a shallower decline in fuel prices (-3.9% YoY in December vs. -6.0% YoY in November). In line with our expectations, the increase in food and non-alcoholic beverage prices was slower in December (0.2% MoM) than in November (0.7% MoM). This was despite soaring butter prices, which caught a lot of public attention but hold little importance for CPI due to their low share in the basket. Energy prices for households remained at the same level seen in November.

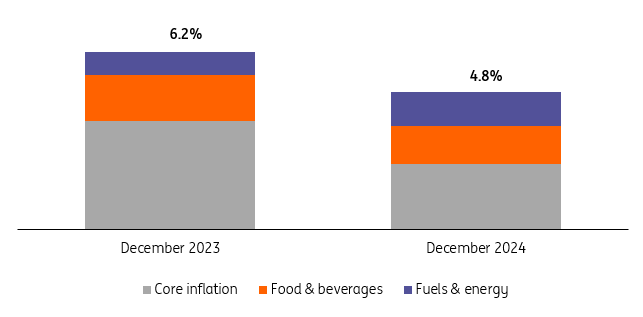

Looking back, progress in taming inflation was limited last year. At the end of 2024, consumer inflation amounted to 4.8% YoY vs 6.2% YoY at the end of 2023. Lower annual headline inflation resulted mainly from the decline in core inflation from very high to elevated levels (our estimate was 4.2% YoY at the end of last year). Food price inflation at the end of 2024 was lower than it was at the end of 2023, but the contribution of energy prices increased, as electricity and natural prices for households were partially unfrozen in July 2024.

Progress in taming inflation moderate in 2024

CPI, %YoY, prec. points.

Source: GUS, ING.

In the first months of 2025, we expect consumer inflation to increase further and reach its peak in March. This will be driven by hikes in excise duty on cigarettes and a low reference base – the VAT on food was at 0% in March last year compared to 5% today.

In the following months, headline inflation should decline and amount to 3.0-3.5% YoY at the end of the year. In our view, this will create space for monetary policy easing and cuts in National Bank of Poland rates by around 75-100bp. At the same time, we note that signals from the MPC have been rather hawkish in recent weeks, suggesting that policymakers intend to start cutting rates later than earlier this year.

More By This Author:

Benign Food Prices Help Turkey’s Disinflation PathFX Daily: More Of The Same To Start The Year

Czech PMI Falls Amid Stumbling Automotive Sector

Comments

Log in or sign up to join the conversation.