Image source: Pixabay

Poland's first estimates of GDP growth at the end of 2024 confirmed that its economy gained momentum as household consumption improved. In 2025, we see GDP expanding at 3.2% vs 2.9% last year on the back of a rebound in fixed investment, boosted by RRF and EU cohesion funds. We also see real disposable income growth slowing.

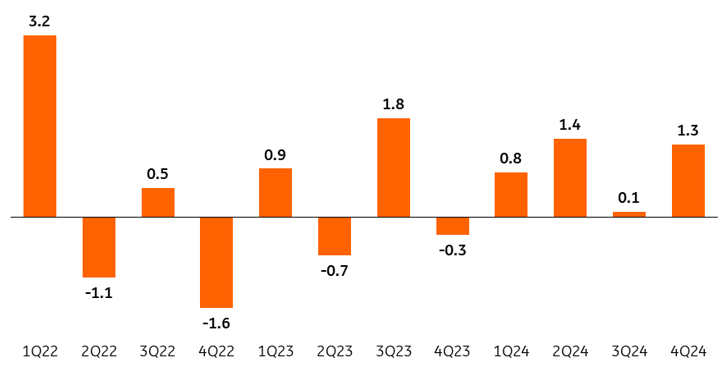

The flash estimate of Poland's fourth quarter GDP growth at 3.2% year-on-year wasn't too surprising to us, as annual data released earlier allowed to calculate the fourth quarter as a residual. The reading was, however, at the lower bound of estimates. Nevertheless, it was visibly stronger than the 2.7% YoY growth we saw in the third quarter; the seasonally adjusted data indicates that the economy gained some momentum, expanding by 1.3% quarter-on-quarter vs an increase of 0.1% QoQ in the third quarter of last year.

GDP growth quickened in 4Q24

GDP, QoQ (SA)

Source: GUS.

Poland's StatOffice will publish the detail fourth quarter GDP breakdown on 27 February. According to our calculations, household consumption rose by about 3.2% YoY (vs 0.3% YoY in the third quarter), public consumption jumped up by some 3.4% YoY (vs 4.5% YoY), while fixed investment increased by around 0.6% YoY (vs 0.1% YoY). The picture is complemented by a negative contribution from net exports (-1.1ppt) and positive impact of change in inventories (about 2.0ppt).

In 2025 we expect Poland's economic recovery to continue. Our forecast of 2025 economic growth is at 3.2%, as compared with 2.9% growth reported for 2024. We expect this year to bring a breakthrough in investment activity, supported by projects financed through the Recovery and Resilience Fund (RRF) and faster absorption of the EU cohesion funds. Purchases of military equipment will also support fixed investment. We see household consumption growth this year at 3.0% vs 3.1% in 2024, but we do see some downside risks. Our forecast assumes a gradual decline in the household savings rate, which surged in 2024. The growth of real disposable should slow this year, so if consumers remain frugal, the role of private consumption in driving economic growth may fall short of expectations.

More By This Author:

The Commodities Feed: Oil Edges LowerFX Daily: Prospects Of A Ceasefire Lift European FX

Rates Spark: A U.S. CPI shocker – Yields Up

Comments

Log in or sign up to join the conversation.