Image Source: Pexels

The Polish economy grew by 3.4%YoY in the second quarter, compared to 3.2%YoY in the first quarter. While the flash estimate did not provide a breakdown of growth components, high-frequency indicators suggest continued expansion in the services sector, stagnation in industry, and a contraction in construction.

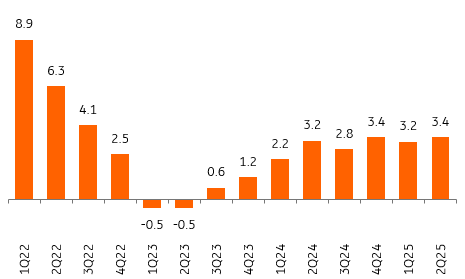

Poland’s GDP rose by 3.4% year-on-year (ING: 3.5%; consensus: 3.4%), according to the flash estimate, beating the 3.2%YoY growth posted in the previous quarter. Seasonally adjusted data indicate that the economy gained momentum as GDP rose by 0.8% quarter-on-quarter following the 0.7%QoQ rise in 1Q25.

Annual GDP growth improved in 2Q25

GDP, %YoY

Source: GUS.

The second-quarter flash GDP release did not include a breakdown of the economic growth composition (detailed data will be published on 1 September). However, based on monthly data available so far, we estimate that economic expansion was mostly driven by the services sector, while manufacturing activity remained subdued and construction output declined in annual terms in 2Q25.

On the expenditure side of GDP, growth was primarily fueled by household consumption, which – based on our estimates – rose by around 4%YoY, up from 2.5% in the first quarter of 2025. This trend is supported by a strong increase in retail sales during the previous quarter (up 5.8% YoY compared to 1.4% YoY in 1Q). The surge in goods demand was partly driven by the shift in Easter-related spending from March 2024 to April 2025. Rising consumption likely coincided with an increase in fixed investment (mainly public), a positive contribution from inventory changes, and a negative impact from net exports.

The Polish economy has accelerated and is on track to expand by 3.5% this year. Economic activity in 2Q25 was underpinned by the Easter effect, and maintaining buoyant growth in the second half of the year will require a further revival of fixed investment, especially in the private sector. The ongoing cycle of monetary easing, coupled with recovering credit demand and increased absorption of EU funds, is expected to bolster investment activity. The main headwind to economic recovery, especially in the industrial sector, is still the subdued demand in key export markets.

More By This Author:

FX Daily: Laser Focused On A September CutThe Commodities Feed: Oil In Wait-And-See Mode Ahead Of Trump Vs. Putin

South Korean Unemployment Falls, But Weak Private Hiring Still A Concern

Comments

Log in or sign up to join the conversation.