Poland: Solid Industrial Performance In August Despite Energy Shock

Industrial output expanded by 10.9% YoY in August even though manufacturers face soaring energy prices and uncertainty about the availability of energy sources this winter. At the same time, producers’ prices continued running at ¼ level higher than in the corresponding period of 2021 and higher costs will continue to be passed on to retail prices.

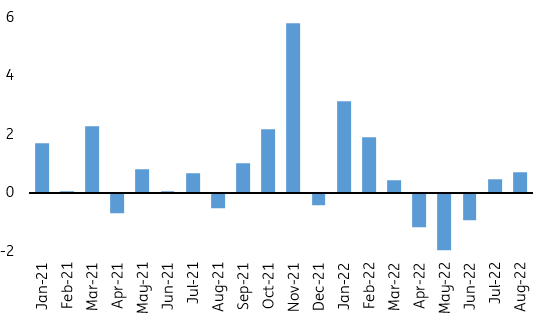

Industrial production rose by 10.9% year-on-year in August (ING: 9.8%YoY; consensus: 9.7%YoY), following an increase of 7.1%YoY in July (revised from 7.6%YoY). The higher annual growth rate than the month before was due in part to calendar effects (a negative pattern of working days in July). Production was also supported by a smaller scale of shutdowns in the automotive and house appliances sectors in August. Production of motor vehicles, trailers and semi-trailers increased by 40%YoY and electrical appliances by 23.9%YoY. Interestingly, while the second quarter saw month-on-month declines in seasonally-adjusted production, the third quarter has brought a rebound in the level of output.

No manufacturing recession in 3Q22

Industrial output (MoM SA)

We find the August production reading a positive signal of economic resilience, given poor leading indicators, weaker orders and high energy and commodity prices as well as uncertainty about the availability of energy in the autumn-winter period. We observe a gradual cooling down rather than a sudden and abrupt halt in activity as suggested by the latest manufacturing PMI index readings. We estimate that there will be an increase in 3Q22 GDP on a quarter-on-quarter seasonally-adjusted basis and that annualized growth will be close to 3%. In other words, we do not see a technical recession in 3Q22, but we still expect the second half of the year to be markedly worse for the Polish economy than the first with the most risk still in winter.

Producer prices increased by 25.5% YoY in August, i.e. at the same pace as in July (after revision), despite another marked decline in fuel production prices (-6.5% month-on-month). Prices in manufacturing increased by 20.2%YoY and in mining and quarrying by 30.4%YoY. However, the greatest pressure was seen from energy prices, which rose in August at a double-digit rate (10.0%MoM) for the second month in a row and are already nearly 80% higher than a year earlier.

Overall, the producers’ prices index (PPI) is around ¼ higher than a year ago, and the process of passing on rising production costs to final prices will continue in the coming months. This confirms our concern that the next few months will bring a new wave of retail price increases. We do not share the optimism of the Monetary Policy Council representatives who speak of a stabilization or decline in CPI inflation before the end of the year. We rather expect an adjustment of prices and the economy to face another price surge, this time an energy shock. In our view, the expansionary nature of fiscal policy will even increase beyond what we see in 2022, making it easier to still pass on high costs to retail prices.

Nevertheless, rate hikes are coming to an end. Recent comments show that the National Bank of Poland (NBP) is rather targeting a decline in the annual CPI (in our view possible by the end of 2023) and a 'soft landing' of the economy, while CPI at 2.5%YoY is a seemingly forgotten target. An important factor that reduces the effectiveness of the rate hikes so far is fiscal expansion. Currently, the total policy mix is only slightly restrictive despite inflation at 16.1%YoY.

With such a definition of NBP targets, we can imagine a rate cut in 2023. With that in place, we may face another cycle of rate hikes in 2024. The way to fight inflation on the monetary and budgetary policy fronts in Poland differs from the approach of other countries, where central banks and governments communicate that domestic demand and labor market need to cool down and wage growth to moderate below the rate of inflation. All of this is to avoid a repeat of the 1970s scenario in the US when it took a couple of cycles of rate hikes to bring inflation down to required levels. The ultimate cost of fighting it was greater than the cooling of the economy at the start of a period of high inflation.

More By This Author:

Why We Expect A ‘Hawkish’ 75bp Hike From The FedKey Events In Developed Markets For Week Of Sept. 19

Key Events In EMEA For Week Of Sept. 19

Disclaimer: This publication has been prepared by the Economic and Financial Analysis Division of ING Bank N.V. (“ING”) solely for information purposes without regard to any ...

more