Image Source: Unsplash

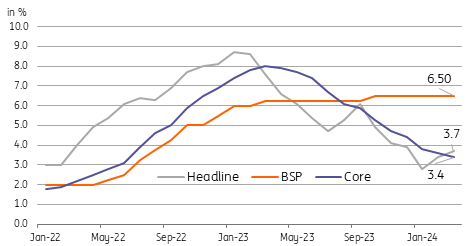

March inflation at 3.7%

Headline inflation for the month of March edged higher to 3.7% year-on-year, up from 3.4% in the previous month but slightly slower than the market had expected. The consensus forecast had headline inflation rising to 3.8%YoY. Compared to the previous month, CPI was up a modest 0.1%, a bit of a moderation after two straight periods where prices rose 0.6% on a month-on-month basis. Core inflation, which strips out volatile food and energy items, slowed to 3.4% YoY from 3.6% previously.

The main driver for the pickup in prices was the index-heavy food and beverage subsector, which posted inflation of 5.6% YoY, accelerating from 4.6% YoY in February. Rice reported inflation of 24.4% YoY, the fastest pace since 2009 and accounting for a whopping 2.2 percentage points to overall headline inflation. On top of expensive food items, transport and restaurants were additional drivers for inflation in March, rising 2.1% YoY (from 1.2%) and 5.6% YoY (from 5.3%), respectively.

Philippines inflation heats up again as rice inflation tops fastest pace since 2009

PSA and BSP

BSP to hold rates at 6.5% next week

Bangko Sentral ng Pilipinas (BSP) rescheduled their policy meeting to 8 April (from 4 April) reportedly to wait for the latest inflation data. With inflation settling close to the upper end of the inflation target and with the Federal Reserve still on hold, we expect the BSP to keep rates unchanged at 6.5%. Despite the March inflation report showing inflation slightly below expectations, BSP indicated that the risks to the inflation outlook remain tilted to the upside.

BSP indicated that it expects inflation to edge past the upper end of its 2-4% inflation target band in the coming months due to tight supply for agriculture products because of the El Nino induced drought. Thus we believe the BSP may extend its pause beyond the upcoming April meeting with a potential rate cut only likely in the second half of the year.

More By This Author:

Rates Spark: Rolling The Payrolls DicePolish Central Bank Keeps Rates On Hold; Governor Likely To Stay Hawkish

Asia Week Ahead: Important Inflation Reports And Key Central Bank Decisions

Comments

Log in or sign up to join the conversation.