"Peak Silver" Is About To Rock Markets And Bring Huge Profits To Smart Buyers

It's Economics 101. Price works to balance supply and demand. Limited supply causes higher prices; higher prices help curb demand.

Well, a potentially very profitable twist on that equation is playing out right now in the silver market. Mined silver supplies have been drying up over the past few years, while silver prices have climbed 20% in the same time frame.

But the exciting opportunity for investors is that precious metals, like silver, are among the only assets that can see higher demand when prices rise. It's just not what normally happens in "regular" markets.

But, to be fair, silver (and gold) are anything but normal markets.

Silver supplies risk falling short of demand for some time to come. In mid-December 2017, I said silver would likely tack on steady double-digit gains before entering a "Tulip Mania"-style profit frenzy.

I think these charts confirm my suspicions. It's likely we're in the early innings of spiraling silver prices as more and more investors decide they simply can't let this bull leave them behind…

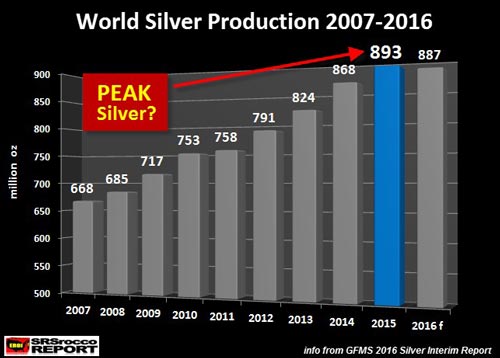

Silver Production Won't Ever Be as High Again

2015 may well have marked a long-term peak in global silver production. That's when the world's mines produced 893 million ounces.

The following year, 2016, saw the first drop in a decade, with output falling to 887 million ounces.

2017 was no better, with production falling another 30 million ounces, to just 857 million ounces.

Forecasts point to a very small increase of 867 million ounces in 2018, up only 1% over the 2017 haul.

But… there's a very big "if" attached to that small increase.

You see, some of the market's most significant silver producers face considerable obstacles all over the world.

Tahoe Resources Inc.'s (NYSE: TAHO) Escobal Mine in Guatemala has shut down due to a suspended mining license, while workers at Hecla Mining Co.'s (NYSE: HL) Lucky Friday Mine near Mullan, Idaho, have been on strike since March 2017.

So, if these mines can get back to producing, that will help boost silver output this year… but it's not quite that simple.

Here's why…

Silver Mining Is a Tough Game… and Getting Tougher

According to recent research by SRSrocco Report, two of the world's largest primary silver mines have been facing some very stiff headwinds.

The troubles come mainly in the form of falling ore grades, expressed in ounces of silver per ton of ore mined, combined with rising production costs.

At Fresnillo Plc.'s Fresnillo mine, in Zacatecas, Mexico, 2010 silver production stood at 35.9 million ounces. The ore grade: 14.1 ounces per ton.

By 2015, it had fallen to less than half the 2010 haul. That year, output was 15.6 million ounces, at an average ore grade of 6.5 ounces per ton.

That means they had to mine more than twice as much rock to get at less than half as much silver. Not a great scenario, though in the last two years output is up slightly, and the yield in ounces per ton has also improved marginally.

The world's largest primary silver mine is South32 Ltd.'s (ASX: S32) Cannington Mine, in Queensland, Australia.

Between 2004 and 2014, its output fell from 44 million ounces produced at an average grade of 18 ounces per ton all the way down to 22.6 million ounces at nine ounces per ton.

So, in that 10-year span, the Cannington mine, one of the world's most important, lost half its output.

In the last three years, Cannington's output has plummeted even further, down to 12 million ounces produced at an average grade of 6.2 ounces per ton.

So as you can see, some of the biggest mines are working a lot harder and still see their output falling.

Now let's look at it from a country perspective.

Silver Production Has Plummeted All Over the World

The following table (we only have numbers up to 2016 for now) ranks countries by annual silver output.

The takeaway here: Fully eight of the top 11 silver-producing nations have seen their production fall.

As we said earlier, supply would normally rise to meet higher prices. The average silver price was $15.68 in 2015, then rose to $17.14 in 2016. And yet, world silver production fell.

That's not a normal response, which suggests that 2015 may, in fact, have been the moment of peak silver production.

It's also true that, meanwhile, silver demand has fallen… but that won't last, either.

Global Industry Will Drive Demand Like Never Before

Physical silver demand has retreated in the last couple of years, but I don't think that's going to last.

Investors bought less silver coins and bars last year, I believe mostly due to the attraction of rapidly rising stocks and Bitcoin as alternatives.

Bitcoin has already been chopped in half from its $20,000 peak, and stocks have begun to fall apart over the past week or so, as indexes slid into "correction" territory.

There may yet be some gains there, but the bull's getting long in the tooth. In any case, as I'll show you, investors are likely to make a renewed flight to the safety that precious metals offer.

Jewelry demand was up slightly in 2017, with slower Chinese buying partially offset by stronger Indian and North American demand.

But industrial demand surged 3%, mostly due to rapidly expanding production in the solar industry.

I think the industrial sector will help drive stronger demand for silver in the next couple of years, as solar panels, automotive, and electronics continue to see strong gains.

Meanwhile, HSBC Bank has said it sees a potential for investors to seek protection in silver. James Steel, chief precious metals analyst for HSBC, said, "Any resurgence in risk may spark 'safe-haven' demand and aid prices." Steel also noted, "Tighter supply/demand balances are an important factor in our outlook."

Here's How You Can Profit on Scarce, Expensive Silver

So here's one of the best ways you can play the inevitability of peak silver, coupled with rising demand.

The Global X Silver Miners ETF (NYSE Arca: SIL) is my preferred "peak silver" proxy.

The ETF has over $400 million in assets spread globally across 27 silver mining companies. Of those we do find both Tahoe Resources and Hecla Mining, both of which could see their silver output challenged until outstanding issues are resolved. But together, they only represent about 8% of the allocation, so I'm not overly concerned about their impact.

Geographical allocation is nicely balanced. It works out to 39.07% in Canada, 17.72% in Mexico, 12.89% in Russia, 12.52% in United States, 11.61% in South Korea, and 6.19% in Peru.

It's true that silver producers will find they have a challenging environment in which to grow their output as grades continue to deteriorate. However, this is the mining sector: I expect many will end up doing deals to take over smaller players in the exploration and/or development stages in order to grow production.

The bottom line: Silver is in a massive bull market, and important production challenges will only add to the metal's irresistible attractiveness and price gains in 2018.

Disclosure: None.