Image Source: Pexels

Economic recovery is progressing on the back of buoyant consumption, while inflation remains elevated. The Monetary Policy Council suggests it may be more open to debate on rate cuts in 2025, especially if the government extends measures to contain electricity price increases next year. We see room for 100bp of rate cuts in 2025.

In second quarter 2024 GDP grew by 3.2% YoY, beating market and our expectations. Growth was still driven by private but also public consumption that rose by 4.7% year-on-year and 10.6% YoY respectively. The former was underpinned by substantial improvement in real disposable income of households, while the latter by wage hikes in the public sector. Fixed investment also surprised to the upside, rising by 2.7% YoY vs -1.8% YoY in 1Q24. Since investment outlays of enterprises performed even worse than in the first quarter, we attribute the rebound in total investment to public outlays (most likely defence spending). Inflation remains elevated and rose to 4.3% YoY in August vs 4.2% YoY in July.

Rates are broadly expected to remain unchanged in 2024; we see room for 100bp cuts in 2025. NBP Governor Glapiński, who in July suggested rates could remain flat till 2026, made a pivot and joined the emerging MPC majority calling for cuts in 2025.

We expect the governor’s tone after the September meeting to be somewhere between his hawkish tone from July and the dovish MPC majority, which we heard over the summer. Second quarter GDP was strong, and the Ministry of Finance revised up its 2024 and 2025 deficit forecasts. Inflation is rising in the second half of 2024. Those are arguments calling for maintaining a hawkish tone. At the same time, average inflation in 2025 should be below the July NBP projection as the government wants to halt electricity prices increase in January 2025. As the main central banks start (Fed) or continue (ECB) easing cycles, Glapiński presumably does not want to be outvoted by the rest of the MPC.

FX and Money Markets: The zloty was unable to extend 2024 lows despite a significant weakening of the US dollar, typically supportive for CEE FX. We see risk of €/PLN moving above 4.30 after the summer. The domestic and European macro backdrop should not sway the market away from a relatively aggressive NBP easing scenario anytime soon. With global risks at least partly priced in, for now we don’t expect €/PLN to move significantly above 4.35 in the year-end unless a substantial deterioration in EM sentiment occurs.

Domestic Debt and Rates: We see curve steepening in 2H24. The 2025 central budget hints at record-high borrowing needs and POLGBs’ issuance. With limited foreign interest in local debt, domestic buyers may prove insufficient to prevent a rise in yields. On the other hand, borrowing needs are high but distributed to many sources of funding, which gives the Ministry of Finance many alternatives. We also think that the market is pricing an overly aggressive NBP easing path, ie, given the expansive fiscal policy domestically. Still, with lacklustre domestic data both domestically and from the eurozone, a repricing of the NBP easing path may not come this year.

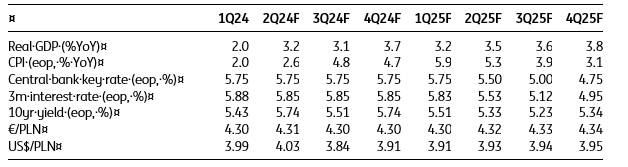

Quarterly forecasts

Source: Macrobond, ING estimates

More By This Author:

Manufacturing And Construction Slowdown Puts The Focus On US ServicesSecond Quarter Contraction In Hungary Confirmed

Turkish Inflation Slows, But Services Remains An Issue

Comments

Log in or sign up to join the conversation.