Image Source: Pexels

After the shortest possible pause in the easing cycle, the NBH was back in business, cutting its key rate by 25bp in September. The change in forward guidance suggests an unchanged view on the future path of interest rates, so our base case remains one more cut over the rest of the year.

Time to cut again came fast

The National Bank of Hungary’s well-telegraphed menu card again offered two options for the September rate-setting meeting. The choice was between no change and a small (25bp) cut, in line with the careful, patient and stability-oriented approach of the monetary easing cycle.

The outcome of the September rate-setting meeting was a 25bp rate cut, with the policy rate being brought to 6.50% on 24 September. The central bank also kept the interest rate corridor symmetrical, with 25-25bp cuts at either end of the range. With 100% of analysts (based on a Bloomberg and also a local survey) expecting exactly this outcome, this may have been the least exciting meeting for a while.

All four main factors supported a small cut

Back in August, the National Bank of Hungary gave the markets a very practical playbook for the upcoming decision. It highlighted four key factors that would play a role in the outcome of the rate-setting meeting. Spoiler alert: all four were highlighted in green in the presentation shown at the press conference.

First, the August inflation readings helped to improve the near-term inflation outlook as disinflation continued, while none of the incoming information changed the medium-term outlook in a significant way. Moreover, energy prices have fallen significantly over the past month, which is also a good sign.

Developed market interest rates have fallen since the last rate-setting meeting, with the ECB and the Fed cutting rates by 25bp and 50bp respectively. While the central bank stressed that market expectations were moving towards further rate cuts for the rest of the year, it added that these expectations were highly volatile in the past. In addition, Deputy Governor Virág telegraphed the Monetary Council's stance not to overreact to the Fed's recent jumbo rate cut.

On Hungary's risk perception, the key message was clear: there has been a slight improvement, but it can change in a minute. So there is no room for complacency. Last but not least, the gradual strengthening of economic agents' confidence is also a welcome development. Between us, this seemed like an ad-hoc reference to make the decision a little more certain. Now that this reference is missing from the newly announced playbook, this statement seems even more true. But that is water under the bridge.

A new forward guidance

Speaking of which, we are now back to three factors on the watch list ahead of the October decision (on 22 October). The inflation outlook is the first, with the main focus on factors that could change the medium-term forecast and the re-pricing of services. Hungary's risk perception is also key, with a focus on the external balance and fiscal policy developments. Last but not least, financial market stability is in the crosshairs, where the sustained maintenance of positive real interest rates is necessary and the shift in global investor sentiment is important.

The Monetary Council decides on the level of the key interest rate on a monthly basis, maintaining its cautious, patient and stability-oriented approach. The menu card remains unchanged, i.e. no change or a moderate (25bp) easing. Since June, every meeting has been a live meeting. So this is nothing new and clearly not dovish. Moreover, the track record shows that we've had both cuts and a hold, so this news doesn't automatically mean that the NBH is ready to ease three more times.

In contrast, we think the main message was the following: “Since the previous interest rate decision, we have not identified any factor that would warrant a persistent shift in the path of the base rate”. As a reminder, the message in August was that market expectations of a terminal rate in the range of 6.25-6.50% by 2024 seemed realistic. Against this backdrop, we see room for one more rate cut in the fourth quarter.

This view is also supported by the change in the press statement, where the Monetary Council removed the line that there may be room for further cautious rate cuts in the period ahead. In the absence of this sentence, we think the guidance is clear: The Monetary Council doesn't want the markets to see multiple rate cuts as a realistic scenario, as of now.

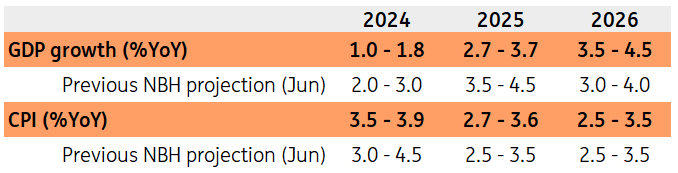

The updated GDP & CPI forecasts

The full macroeconomic assessment and outlook will be published with the September Inflation Report on 26 September. The NBH has significantly narrowed the inflation forecast range in 2024. Such a range is in line with our forecast and is based on the latest incoming data, which makes it statistically unlikely that average inflation will be close to 3% or significantly above 4% this year. The forecast for 2025 CPI has been slightly updated. The upward revision of around 0.2ppt reflects the pro-inflationary impact of recent fiscal measures. Meanwhile, the inflation outlook for 2026 remained unchanged. While the outlook for 2024 is in line with our baseline projection, the forecast for next year is seen as somewhat optimistic, with inflation accelerating from 3.8% in 2024 to 4.2% on average.

The forecast range for GDP growth this year and next has been revised significantly lower as a result of incoming GDP, high frequency economic activity data and worsening external outlook. The central bank sees the performance of the Hungarian economy in a range of 1.0-1.8% on average in 2024, which includes our baseline forecast (1.5%). For 2025, the NBH lowered the GDP growth forecast range by 0.8ppt. In contrast, the outlook for economic activity in 2026 was raised by 0.5ppt. In 2025-2026, we forecast economic activity at 3.6% and 4.4% respectively, which is at the upper end of the central bank's updated forecasts.

National Bank of Hungary forecasts

Source: NBH

One more rate cut is realistic in the fourth quarter

There was a lot of smoke screening, but we were trying to read even the tea leaves. Deputy Governor Virág made it clear in response to a question back in August that the year-end interest rate target remains unchanged at 6.25-6.50%. Fast forward to recent messages and the new forward guidance, where he said that the rate path hasn’t changed fundamentally and the Monetary Council scrapped the reference of room for further cuts. In practice, this leaves us with a maximum of one more cut in the fourth quarter, as of now.

We see the year-end rate at 6.25%, so an unchanged call from our side. In the very short run and having a way too early call on that, but we see October as an on-hold meeting. The ECB is unlikely to deliver a cut in October, while the Fed meets only in early November. With the NBH meeting being exactly two weeks before the US election, there might be a minefield out there from an investor sentiment and market stability perspective. Moreover, our short-term inflation forecast suggests a looming upside surprise versus the central bank’s inflation path.

Our market views

The forint's first reaction during the press conference was to strengthen but the discussion of rate cuts in the Q&A session seems to have changed the direction of the market and the initial gains have been erased. EUR/HUF moved up already yesterday to 395 and is almost unchanged at the end of today but higher compared to the beginning of the week. On the other hand the rates market is suggesting a dovish outcome from the meeting as well, which should continue with more repricing in the days ahead and indicating a weaker HUF later on.

Like we mentioned in the NBH preview, we don't see room to go above 400 now on the local side due to the NBH reaction function but also on the global side due to higher EUR/USD which may move further up, dampening the depreciation pressures on CEE currencies. Thus, we continue to see the 392-400 EUR/HUF range as the playing field at least until the US election and a weaker HUF later next year. In the short term, pressure for a weaker HUF is likely to return to the market but should remain subdued in the 394-396 EUR/HUF range for now.

HUF rates are moving down the entire curve with a strong steepening bias. The IRS curve is already the steepest in the CEE region and there is still room for further steepening, which seems like the way to go after this meeting. The market is pricing in 2-3 additional rate cuts for this year for the next three meetings and most of the repricing is happening in the next year segment. The terminal rate has moved to 4.75% around the end of next year, assuming normalisation of the BUBOR premium. This still seems like a realistic scenario to us under some conditions, but we can expect the market to price in more after today's meeting but key is the reaction of FX and next inflation print. Moreover, with core rates rebounding, further steepening of the curve is the clear direction here for now.

More By This Author:

The Commodities Feed: Supportive Measures From ChinaThe PBOC Has Unveiled A Monetary Policy Easing Package In A Bid To Support Growth

Asia Morning Bites For Tuesday, Sept 24

Comments

Log in or sign up to join the conversation.