Mexico: Still An Outlier In Its Policy Response

Mexico’s central bank should extend the easing cycle with another 50bp rate cut this week. Still, the country’s unusually modest counter-cyclical policy effort continues to stand out. This should exacerbate the risk of greater permanent damage to the economy stemming from the ongoing health crisis and delay the eventual recovery.

Another modest rate cut expected by Mexico’s central bank

The monetary policy meeting in Mexico, this Thursday, should end with policymakers, once again, reducing the policy rate by 50bp to 5.0%. This should not be an especially controversial meeting, as signaled by the widespread consensus among analysts about the meeting’s outcome.

But, like we’ve discussed before, Mexico’s central bank often appears to waver between the desire to signal moderation in its monetary easing effort and the need to stimulate the economy and offset the widening slack in the local economy, which has been intensifying for more than a year now.

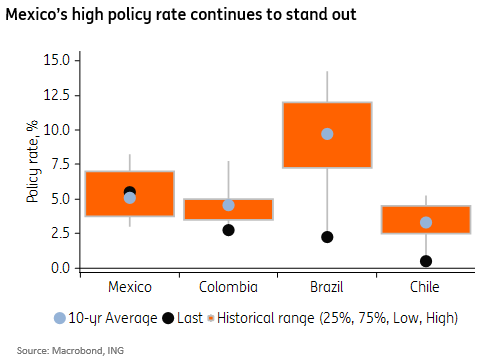

The bank’s more hawkish tendency is evident in the chart below, which shows that, despite the long-simmering recession, Mexico still has the highest policy rate among LATAM majors, by a wide margin.

(Click on image to enlarge)

More surprisingly still, at its current level, Mexico’s policy rate is higher than the average that prevailed in the country over the past 10 years. This is, perhaps, close to a unique situation across EM.

Economic outlook seems consistent with greater stimulus

Banxico’s policy stance can be hardly justified by Mexico’s economic cycle prospects, given the grim outlook for economic activity and the relatively benign inflation trends. As a result, it reflects, presumably, an effort to support the stability of domestic financial markets, especially the Mexican peso.

This long-simmering dilemma between supporting the currency, or the economy, has resulted in frequent splits within the board, with dissents on both sides of the hawkish-to-dovish spectrum, depending on the meeting.

However, as the economic impact of the Covid-19 crisis is fully incorporated into Banxico’s inflation outlook, we expect the majority within the bank to side with their more dovish members. Bank officials already recently acknowledged that 2020 could end with GDP contracting as much as 9%. This would be roughly in line with consensus estimates and represents one of the largest drops in GDP expected in LATAM in 2020.

A terminal rate of 4.0%

Even though policymakers still characterize the balance of risks for inflation as “uncertain”, the disinflationary impact of the recession and the difficult economic reality created by the health crisis should push policymakers to mover closer to the stance adopted elsewhere across EM and DM, and extend the easing cycle beyond this week.

(Click on image to enlarge)

Beyond this week’s meeting, we expect two consecutive 50bp rate cuts to the reference rate. One of these cuts could possibly take place during another off-schedule meeting, which would bring the policy rate to 4% by August.This compares with a market consensus that is closer to a terminal policy rate of 4.5%.

Timid counter-cyclical effort raises the risk of “scarring effects”

Even though our monetary policy call is more dovish than the market consensus, we continue to characterize Mexico’s economic policy relief efforts as modest, at best.

In fact, with the policy rate still closer to the upper-bound of its neutral range and a small commitment by the federal government to boost fiscal spending, Mexico’s policy-relief efforts is a clear outlier across major economies in the world.

In our view, this policy response is somewhat inconsistent with the facts that Mexico does not face obvious imbalances on the inflation or balance of payment fronts, and that Mexico’s GDP is likely to face one of the deepest slumps in LATAM this year.

For now, the MXN’s yield-advantage suggests that some local assets may continue to appeal to a broad range of investors and perform relatively well. However, we believe that the country’s timid policy response has increased the downside risk to economic activity, which should eventually stress fiscal accounts and increase the risk of credit-rating downgrades, adding important long-term downside risk to local assets.

Disclaimer: This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information ...

more

Comments

No Thumbs up yet!

No Thumbs up yet!