Image Source: Pexels

The nearly complete data from the real economy for 1Q25 indicates that annual growth was slower than the 3.4% year-on-year achieved in 4Q24. Both industrial output and retail sales have decelerated, with construction the only sector showing improvement. Due to elevated uncertainty, the mid-term outlook is shaky.

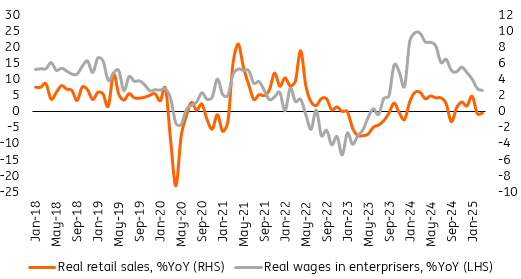

Retail sales fell by 0.3% year-on-year in March, following a 0.5%YoY decline in February. As expected, the “Easter effect” weighed on consumer spending on goods. In 2024, Easter purchases took place in March, which boosted the reference base, whereas in 2025 Easter was celebrated in mid-April. This dampened purchases of food (-9.4%YoY) and in the “other” category (-12.2%YoY).

On a positive note, purchases of durable goods were encouraging. Double-digit increases in purchases were reported in passenger cars (+18.4%YoY) as well as furniture, consumer electronics and house appliances (+12.9%YoY).

Sales eased with slower wages growth

Retail sales and wages in enterprises (real),%YoY

Source: GUS, ING.

The beginning of the year was not particularly impressive for the Polish economy. Annual growth of industrial production and retail sales eased in the first quarter of 2025 versus the fourth quarter of 2024. The only sector that showed some improvement was construction, albeit from a very poor performance in 2024. Based on the available data, we estimate that in the first quarter of the year, GDP growth fell short of the 3.4%YoY reported in the fourth quarter of 2024.

The state of the economy is evidently not indicative of a pro-inflationary boom, and the balance of risks for GDP growth ahead is tilted to the downside, partly due to uncertainty linked to American trade policy that may hinder international trade in goods.

At the same time, both CPI and core inflation at the beginning of 2025 were below both the March National Bank of Poland (NBP) projection and market expectations. Wage growth in enterprises also slowed in early 2025, and the spike in electricity prices for households in the final quarter of this year is unlikely.

In such an environment, the Monetary Policy Council is likely to ease monetary policy in May, and policymakers will debate whether the first rate cut should be 25bp or 50bp. In our view, the latter is more likely, and by the end of the year, interest rates may be reduced by 125bp.

More By This Author:

FX Daily: Bessent Throws US Assets A LifelineThe Commodities Feed: The Door Opens For Tariff De-Escalation

South Korean Consumer Sentiment Remains Weak, Weighing On Growth

Comments

Log in or sign up to join the conversation.