Image source: Pixabay

The UK jobs market is cooling, even if data quality issues make it hard to say anything too concrete about the latest figures. Assuming services inflation proves less surprising in data due next week, we think the Bank of England is on track for a rate cut in August.

The UK jobs market is cooling quite noticeably now, and that makes it all the more surprising that financial markets are pricing just a 7% probability of a rate cut next week and only 46% for August’s meeting. We think a summer rate cut is much more likely.

The latest hiring figures tend to back that up, though of course there are still major question marks surrounding the quality of the data. Taken at face value, the rise in the unemployment rate from 3.8% at the end of last year to 4.4% now is pretty eye-catching. But the very pronounced fall in the response rate to the Labour Force Survey and potential bias in the achieved sample means it is still hard to know how seriously to take these latest numbers.

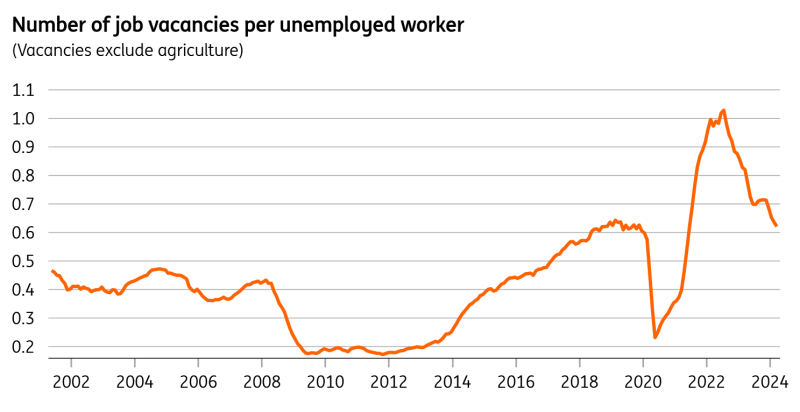

But the data on unemployment corresponds with the ongoing fall in job openings, and the vacancy-to-unemployment rate is now back down to pre-Covid levels. An alternative measure of employment using firms’ payroll data shows it flat to slightly negative so far this year.

The vacancy to unemployment ratio is back to pre-Covid levels

Macrobond, ING calculations

Wage growth is proving sticky, albeit the latest data was a tad below consensus. Private-sector wage growth is rising at 5.8% year-on-year and on a month-on-month basis is still showing decent momentum. Some of that is potentially linked to the recent 10% rise in the National Living Wage, though we think the overall impact of this policy change won't be huge.

Again there are some doubts over the data quality here. It’s not directly affected by the same sampling issues as the unemployment data, but policymakers are concerned that one-off cost of living payments that were paid 12-18 months ago were wrongly accounted for as permanent increases in pay. When those payments weren’t repeated this past winter/spring, in theory, this would show up in the data as an artificial slowdown in wage growth. While it's hard to say how much of the recent fall in pay growth is linked to this, the Bank has said that increased volatility in these wage numbers means it's paying less attention to them than it was just a few months ago.

So when it comes to the near-term direction of interest rates, next week’s inflation data, due a day ahead of the June policy meeting, will be much more important. Services inflation shocked to the upside in April’s data, but this was heavily linked to volatile one-off price hikes at the start of the financial year. We think May’s numbers should be less surprising, and we think the Bank is lining up for a rate cut at the August meeting.

More By This Author:

FX Daily: The Euro Faces A Long JuneThe Commodities Feed: Brent Back Above $80

Turkey Sees Temporary Increase In April’s Current Account Deficit

Comments

Log in or sign up to join the conversation.