Following the new Kwarteng/Truss economic policies revealed in last week’s mini-budget, the widespread condemnation is a reflex Keynesian response from a world which has become hostage to erroneous economic and monetary groupthink in its major institutions.

Kwarteng has jogged the global statist establishment out of its complacent drift into totalitarianism. This is a wake-up call to markets everywhere, a catalyst for the unwinding of accumulated market distortions. Mounting criticism from all quarters is shooting the messenger, but the message has been delivered.

In one important respect, the criticism is valid. Kwarteng must address the budget deficit urgently by taking steps to reduce the size of the state as a proportion of the total economy. Only then, can inflation be conquered, and the pound stabilise. In another respect, the new policy is sensible: by plotting its own free market/Hayekian course, Britain can emerge out of the crisis sooner than other nations stuck in the current democratic-socialist paradigm.

If we assume that Kwarteng does address the size of the state and eliminate budget deficits as early as practically possible, he will have a practical plan for a post-crisis Britain. Economic recovery can than happen sooner rather than later, a major consideration given that the next general election is in a little over two years’ time.

It is too late to avoid the gathering global crisis, the financial consequences of which are bound to devolve in large measure on London’s financial centre. Indeed, Kwarteng’s wake-up call may be the trigger for a financial avalanche. But what he is unlikely to realise is that the gathering crisis is so severe that even the continued existence of fiat currencies will be threatened, with the euro and sterling being particularly vulnerable.

In this article, I also comment on the Bank of England’s failure as an institution, whose future role in monetary affairs should be strictly curtailed. And I advocate the abandonment of all trade tariffs, with the possible exception of agriculture for political reasons. These are fundamental reforms which must accompany free market policies.

We must proceed with our commentary ignoring the existential threat to currencies if it is to be relevant to the government’s economic policies and their global impact.

The Keynesians don’t like it…

The timing of Kwarteng’s mini-budget was calamitous, in that it happened while currency chaos was already roiling markets, not just for sterling, but the euro, yen, yuan, and a host of others which are all suffering from a mounting flight into the dollar. And it wasn’t just currencies. The increasing realisation that interest rates globally will continue to rise has driven a flight out of anything deemed riskier than short-term US Government debt.

Before Kwarteng took to his feet in Parliament last week, US Treasury yields were higher than the equivalent gilts. Even without intervention, this contravened market wisdom and needed correcting.

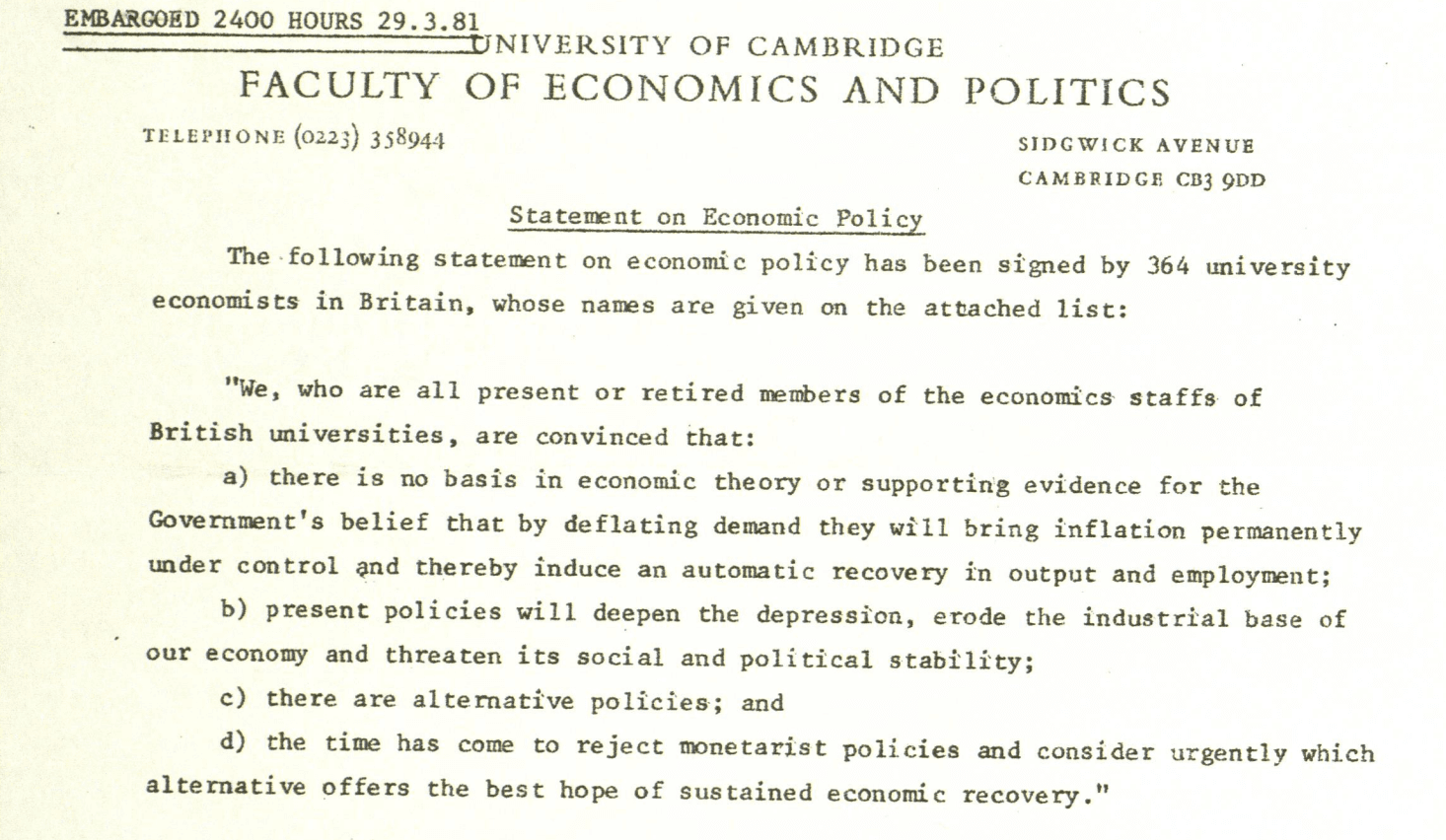

As a matter of fact, Kwarteng’s budget was mostly known in advance — only the detail needed filling in. The problem with it is not just febrile markets, but a tax-cutting, supply-side budget was launched in markets dominated by Keynesian actors. It is reminiscent of the 364 eminent economists (all Keynesians) who strongly criticised Sir Geoffrey Howe’s 1981 budget — and were proved wrong. The letter’s introductory paragraphs are reproduced below.

(Click on image to enlarge)

Lord Lawson, who followed Sir Geoffrey as Chancellor wrote in his autobiography that no sooner had these economists criticised the 1981 budget, than economic recovery began. And seven years later, he also wrote the following:

“We had to dispel the notion that the way to economic success lies through a sort of fiscal levitation. That was the abiding post-war delusion—that governments could spend and borrow their way to prosperity and fine-tune the performance of the economy through something known pretentiously as demand management…It used to be an establishment nostrum that you need a budget deficit to get economic growth. That was the belief which lay behind the notorious letter by 364 economists in March 1981. We have given the lie to that, decisively. There can no longer be any argument about it. Everyone—or almost everyone—now accepts that the proper role of macro-economic policy is to keep downward pressure on inflation and to maintain a stable framework in which the private sector can expand.” [i]

In defying Keynesian orthodoxy, Kwarteng faces a similar problem today. But impartial observers will have noted that before Kwarteng’s intervention, the establishment’s macroeconomic policies have failed — not just in the UK, but in all the G7 nations which coordinate economic and monetary policies.

But if Kwarteng is to replicate the success of Howe’s 1981 budget, he must bring the budget deficit under control as a matter of urgency. That is the source of inflation, and it is entirely the responsibility of the Treasury. The Bank of England may well be a waste of space, but it cannot be blamed for fiscal deficits.

The background to the mini budget

The political strategy was brave, as the cynics would have it. Kwarteng took the initiative and hit the ground running. As one of his first acts, he had already removed the incumbent permanent secretary to the Treasury, Sir Tom Scholar. In doing so, he has broken the Treasury out of the Whitehall group-thinking Keynesian bubble. Consequently, very few inside the Whitehall-Westminster establishment understand his economic strategy, and it is widely criticised.

But both Kwarteng and Truss have degrees in economics, and like Margaret Thatcher and Sir Keith Joseph in the late 1970s appear to be followers of Hayek rather than Keynes. Kwarteng is particularly interesting, having excelled at the heart of an Englishman’s environment. He was a King’s scholar at Eton, went on to get a double first in classics and history at Cambridge, and then to Harvard on a Kennedy scholarship where he gained a PhD in economic history.

Obviously, Kwarteng is no intellectual slouch, and probably understands the historic context of Keynesianism and John Law’s doppelganger economic and monetary policies which collapsed the French economy in 1720.

Only seventeen days after his appointment as Chancellor of the Exchequer, Kwarteng’s tax cutting budget certainly shows confidence in his approach. But that’s only half the job done. The other half must be to reduce the size of the state in the overall economy as rapidly as possible. A statement on that is scheduled for November, but there is now mounting pressure to bring that forward.

The story emanating from the media is that the budget will be balanced by boosting the private sector rather than radically cutting public spending. It is a familiar strategy, pursued successfully by President Reagan. But circumstances are different now. In Reagan’s time, interest rates were in a long-term downtrend, and the dollar’s hegemony was rising after the calamitous seventies. Now, global interest rates are in a long-term uptrend, and sterling has no hegemony. However, Reagonomics did show the economic power of lower taxes as a positive driver of economic performance.

More recently, President Trump tried his version of Reaganomics by increasing the budget deficit and imposing trade barriers against Chinese imports. That merely set up the budget deficit to be even greater when covid came along, and Trump’s failure opened the door to Biden-led wokeness and accelerating monetary inflation.

Commentators also compare the Truss/Kwarteng budget policy with that of Margaret Thatcher. But in her Chancellor’s first budget in 1979 which was similarly introduced within weeks of gaining office, Sir Geoffrey Howe increased VAT offsetting some of the immediate income tax cuts. Reductions in public spending were also announced, with Sir Geoffrey stating that “We cannot go on avoiding difficult choices”. In those days, the Treasury set interest rates and they were increased from 12% to 14%.

In Kwarteng’s budget, public spending is being increased significantly, principally to cap energy prices. Some tax increases announced for the next fiscal year (6 April 2023 to 5 April 2024) will be dropped, and income tax reduced slightly as well. His plan is to contain consumer price inflation with energy caps and loan guarantees to businesses through the banking system, while freeing up domestic energy production through fracking and granting a new round of North Sea oil licences. This bears very little resemblance to the Thatcher government’s first budget, or indeed to any that followed.

As announced, Kwarteng’s growth plan is to stimulate the supply side of the economy by cutting red tape, removing bureaucratic waste, and encouraging private investment. We have heard all this before. And thirty-eight new investment zones, benefiting from tax incentives and planning liberalisation have been identified, presumably a variation on Boris Johnson’s free trade zone concept.

Will it work?

The politics are a problem, as the statist establishment and political opponents get their thoughts together. Through disruptive strikes, public sector and rail trade unions will fight it tooth and nail. By pursuing a less left-wing approach, the Labour party is hoping to gain electoral support from the middle ground. And sterling’s immediate response, falling over 3% against the US dollar on the day of the speech and with the sharp rise in gilt yields signalled that the days of cheap government funding are over. Other governments should take note.

Intentions to radically reduce public spending were not even touched upon. It is hard to imagine that the combined intellects of Truss and Kwarteng are unaware of this elephant in the room. But with most public spending mandated by parliament, the room for manoeuvre is limited without enabling legislation. Health and social care accounts for 36% of total departmental expenditure limits, education 16%, defence 9%, Scotland 6%, and Wales and Northern Ireland 7%. That’s about three-quarters of all departmental spending, which is commonly regarded politically as no-go areas for significant expenditure cuts.

We are due hear more on the subject of expenditure reductions in November unless an announcement is brought forward. Clearly, cutting public spending in order to balance the budget is not going to be achieved easily. But these are not the only problems, and the new government will have to manage its way through some contentious issues, the most pressing of which are the consequences of rising interest rates and the Bank of England’s failure to anticipate and control inflation.

The Bank of England’s failures.

In its monetary policies, the Bank of England has failed in its primary objective, which is to control inflation, or more specifically, the rate of increase in consumer prices. Besides the budget deficit being beyond the Bank’s control, its attempts to manage economic outcomes have always failed. Quite simply, the bank’s activities must be severely curtailed if Kwarteng is to succeed, and he has already delivered a warning shot across the Governor’s bows.

The Bank’s directors have demonstrated that they are captured by the groupthink that is common to other major central banks, rejecting free markets in favour of ever-increasing interest rate suppression. Having followed these policies for decades, they failed to anticipate the change from declining interest rates, when markets began to reassert themselves. Blindly following the Office for Budget Responsibility’s forecasts, the Bank’s directors still hope that consumer price inflation will return to a targeted 2% in due course.

We can identify four major policy areas that have led to the fiasco created by the Bank’s inflation policies:

- Consumer price inflation is wrongly believed to be predominantly set by changes in supply and demand within the economy, and consumer confidence is thought to be the dominant variable. The role of credit is poorly understood and consequently ignored.

- The Bank appears to believe that changes in the quantity of currency and credit in the economy has only a limited impact on prices and that inflation of consumer prices can be managed primarily though interest rates. It fails to understand that interest rates reflect the time preference of savers, which in turn includes an assessment of the future loss of a currency’s purchasing power. As empirical evidence has demonstrated, it is an error to think interest rates are just the “cost” of borrowing money.

- Monetary policy management is set by international cooperation between central banks, which is intended to reduce exchange rate fluctuations. The errors in this approach are that policy becomes a subset of a larger groupthink and that if the concepts behind it are flawed, a global currency crisis ensues.

- Systemic bank risk has been notionally brought under control by internationally agreed bank regulations. The belief that this risk is now contained is reinforced by the erroneous conviction that international banking regulation is effective.

I shall expand on these issues in turn.

Managing consumer price inflation

The stated objective of monetary policy is to influence the behaviour of consumers so that the economy can grow at a rate that allows prices to gently rise at about 2% per annum. Central bankers believe that a positive trend of consumer price increases is necessary to ensure that a healthy level of demand for goods and services can be stimulated without leading to overheating, and that the condition can be managed.

But nowhere in the Bank of England’s analysis does there appear to be consideration given to the bank credit cycle, the root cause of economic instability. It is a cycle that has been evident for as long as reasonably reliable statistics have been available on periodic booms and busts, even under the gold standard. The business cycle, which is driven by the bank credit cycle, is what drove Keynes and others to invent macroeconomics as a tool for managing the consequences. No regard was given to the actual causes of periodic business slumps. Rather like quack doctors believing that bloodletting was the only cure for a wide range of illnesses, Keynes and his fellow statists failed to discern the true causes behind economic slumps, when the correct diagnosis was already made by Hayek, his contemporary at the London School of Economics: excess credit leads inevitably to an artificial boom and its correction is the slump.

Instead of identifying the problem, the evolution of econometrics as the statistical measurement of everything took economists further away from a correct diagnosis. Gross domestic product was invented to quantify the economy. It is certainly useful for a government trying to determine the tax potential of its electorate, but that is all. Using it for management of the economy is a gross error and must be ceased if genuine economic progress, which is not the same thing, is to be permitted.

Furthermore, Keynesians make the mistake of thinking that a downturn in nominal GDP is driven by consumers withholding their spending. This is why they associate a recession with falling prices. The error is to not understand that all GDP transactions are settled in commercial bank credit, and it is the withdrawal of bank credit, reflected in vanishing deposits, which leads to its contraction. The solution is to avoid overexpansion of bank credit in the first place: but central banks always condone overstimulation to encourage recovery from the previous credit downturn.

Therefore, the credit contraction phase of successive cycles tends to be increasingly destructive. And we have certainly seen that since the dot-com crash, the Lehman crash, and now the emerging crisis today.

By suppressing interest rates to zero or negative values, even into the end of the bank credit expansion phase, central banks have added unprecedented monetary distortions into the mix. Now that interest rates are inexorably rising, we can expect the contraction of bank credit, and therefore the collapse of GDP, to be even more destructive than in previous cycles. In anticipation of this systemic calamity, the book values of many global systemically important banks (G-SIBs) are little more than call money on their survival. In the UK, Barclay’s price to book is 38%, HSBC’s is 53%, and Standard Chartered 34%. If the directors of these banks discharge their duty of care to their shareholders, they will be contracting their balance sheet ratios radically from nearly 20 times for Barclays, and 15 times for both HSBC and Standard Chartered. To return to more normal levels of leverage for these banks and the UK’s domestic banks (Lloyds, NatWest etc.) probably requires bank credit to contract by up to a third.[ii] While the financial sector is bound to be badly undermined by credit withdrawal as well, there can be little doubt that the nominal GDP statistic faces substantial contraction.

Almost certainly, the Bank of England’s response will be to replace contracting bank credit with central bank currency and credit. But the effect on sterling’s purchasing power is bound to be to undermine it either on the foreign exchanges (as we are already seeing), or in the minds of its domestic users. Expansion or contraction of bank credit certainly have their effects on a currency’s purchasing power, but not nearly as much as the very public actions of a central bank’s inflationary policies.

The assumption adopted by policy planners, that consumer prices are only driven by the balance of production supply and consumer goods, is demonstrably false. These errors will continue to be made by the Bank of England as it attempts to manage the emerging crisis.

International cooperation and policy groupthink

International cooperation started when Benjamin Strong at the Fed conspired with Montague Norman, his opposite number at the Bank of England, to manage gold reserves and sterling in the aftermath of the First World War. Following the Bretton Woods agreement, central bankers have increasingly cooperated with each other in attempts to reduce exchange rate volatility and manage market outcomes.

Besides setting themselves up against free markets and thereby suppressing them, today’s forums such as G7 and G20 are simply aimed at collaborative control. At the core is entrenched arguments, where participants learn by relying on in-group sources for their information and ideas, and they tend to summarily dismiss information and ideas from outsiders. Prior beliefs promote confirmation bias and the dismissal of contrary evidence.

This leads to classic groupthink. Central bankers and their advisers exclude all contradictory evidence that challenges their underlying assumptions. And these shared beliefs are promoted into becoming an unchallengeable consensus. Anyone who confronts the consensus by not agreeing is simply excluded from further discussion, since dissent cannot be tolerated. Thus, consensus is used to control the membership of central banking committees, both within the Bank of England and with other central banks.

Clearly, these strictures lead to the idea that a Governor of the Bank of England should be a safe pair of hands. But the safe pair of hands merely parrots the group-thinking party line. From the top down, statements emanating from the Bank unconsciously confirm this group-thinking flaw, which extends through the offices of the Bank for International Settlements into common policies being pursued by central banks everywhere and regularly endorsed at G7 and G20 meetings. It is the three wise monkeys’ syndrome written large.

I have described above how the cycle of bank credit expansion destabilises an economy by injecting excess credit into it and then withdrawing credit when the interest outlook deteriorates. The top-down management of this credit cycle is being conducted by central banks, which by following Keynesian theories have collectively blinded themselves to its existence. The errors that have and continue to be made by this cabal are obvious to prescient outsiders, but they have no voice. They are seeing a Greek tragedy unfolding, whereby in common with other central banks the Bank of England is falling into a chasm of disaster though institutionalised failure and evolving circumstances with which the bank cannot deal.

Systemic risks are rapidly increasing

We learned the lack of awareness of the Bank of England to systemic threats from the financial system in the last cyclical credit crisis. In September 2007, the Financial Times reported that Jon Moulton, a prominent private equity investor, told of a breakfast meeting with senior Bank of England officials. “It became clear that they did not know what a CLO was [collateralised loan obligation]. I had to show a senior man by drawing a diagram on the back of a napkin.” Speaking ironically, Mr Moulton said, “It was really reassuring to see they did not know what was going to explode on them.” He said that the Bank “had no weapons to control CLOs.”

At that time, the Bank was not responsible for bank regulation, but someone in the Bank should have mustered intelligence on the developing situation, which exploded in the form of the Lehman failure eleven months later, just as Moulton predicted. Today, the Bank is responsible for bank regulation. Nevertheless, the evidence is that officials still fail to grasp the systemic risks in the financial system they oversee. Instead, they rely on the groupthink behind internationally agreed Basel regulations, now in their third iteration.

Basel 3 focuses mainly on bank liquidity, paying less regard to the commercial responsibilities of bank directors. Other than mandating that Tier 1 capital (shareholders’ equity and retained earnings) must not be less than 3% of assets, along with a supplemental buffer for G-SIBs, and so long as attention is paid to minimising risk-weighted assets, banks can easily leverage their balance sheets up to thirty times. Their response to zero and negative interest rate regimes has been to retain profitability by leveraging their balance sheets within Basel rules, so that the average G-SIB in the Eurozone and Japan, where negative rates were and still are imposed, now exceeds twenty times. The leverage ratios for the three British G-SIBs have already been mentioned above.

These ratios are highly profitable while business conditions are healthy. But when interest rates start rising and economic prospects sour, substantial losses are bound to mount, wiping out Tier 1 capital as much as twenty times faster on the underlying balance sheet. This is what drives bank directors to contract their loan books as fast as possible all at the same time when they perceive potential losses.

On the liability side of a bank’s balance sheet, as well as equity and retained profits there are loans to the bank, mostly in the form of depositors’ funds. Though, as noted in endnote 2 there are usually other liabilities loaned to the bank. The depositors’ funds are originally created as contra entries against lending funds to borrowers. When a depositor has not taken out a loan, his deposit will have been novated to him from someone who has, likely through a chain of novations.

When an entire commercial banking network contracts its total bank credit, it does this by calling in loans, and selling down financial assets. Just as deposits were originally created through a process of balance sheet expansion, balance sheet contraction reverses the process. Broad money supply contracts and there is less credit available for economic transactions. Nominal GDP contracts accordingly.

Unless the effect is minor, highly leveraged banks can rapidly find themselves insolvent in respect of their losses relative to balance sheet equity. These conditions are mounting not just for the UK G-SIBs and domestic banks, but even more so for their counterparties in Europe and Japan. Being the international clearing centre for commercial banks, London is exposed to widespread settlement failures.

A primary duty for the Bank of England is to ensure that the commercial banking system does not fail. Furthermore, since quantitative easing led to increased bank reserves on its own balance sheet, they would be called in by liquidators of failed banks if they are not rescued. Therefore, systemic failures being a mounting problem, and London being the clearing centre for European banks amongst others, the new trend of rising interest rates risks collapsing the entire UK and international banking system, which would have to be rescued by the Bank of England.

And in charge of all this is group-thinking central planners, who made a major contribution to creating this mess in the first place. The Treasury will end up with the liabilities from the Bank’s policy errors, which will have to be managed. It is essential that in doing so, Kwarteng moves UK monetary policy away from the influence of the Bank for International Settlements group-thinking cartel, and the Bank of England.

Trade policy

From her previous office as foreign secretary, Liz Truss is fully aware of the difficulties in negotiating free trade agreements. There is a far better policy approach: simply abolish all trade restrictions and tariffs, with the exception of agriculture which can be addressed later.

The motivation for trade agreements is pure protectionism. There is an erroneous belief that trade imbalances arise from unfair competition, and that deficits can be reduced by promoting exports. Trade deficits arise not from these factors but are the counterpart of government budget deficits financed by inflationary means. Put very simply, budget deficits result in monetary inflation, which gives the private sector the financial resources to spend more than it earns. In national accounting terms, the trade balance is equal to the sum of the national budget deficit adjusted for the change in total savings.

Therefore, the solution for a trade deficit is to not run a budget deficit. Lobbying by exporters should be disregarded. Instead, individuals should be free to spend their earnings and profits as and where they please and thereby benefit from comparative advantage. Not only will this encourage unsubsidised competition but it focuses businesses on what can be provided to consumers most efficiently in the context of available capital resources.

Furthermore, free trade encourages capital inflows from foreign businesses seeking to benefit from the free trade environment. For empirical evidence, look no further that Peel’s abolition of trade tariffs in the nineteenth century and the economic benefits that followed. And look no further than the remarkable success of Hong Kong which rose rapidly from the ashes of Japanese occupation to become one of the wealthiest states per capita in less than fifty years.

Genuine free trade is an essential part of a new Hayekian economic policy and an important break from the destructive grasp of international socio-economic group thinking and control.

Conclusion

The Bank of England was given its independence from the Treasury on the basis that the political class knew less about monetary affairs than the experts, and the experts should be independent from political considerations. Clearly, the policy has failed, and consequently leaves the Treasury without the levers to correct the situation. This is a dilemma for markets, which understand the incompetence of politicians in monetary matters, but have yet to recognise the incompetence of central bankers.

This new era of rising interest rates, driven by an accelerating collapse of the purchasing powers of all fiat currencies, is exposing the fallacies concealed by increasing suppression of free markets by governments and their central banks. The current generation of market participants know nothing else. They are frightened of free markets, preferring their losses to be limited by remedial actions taken by the authorities.

When sterling was traduced following Kwarteng’s mini-budget, Keynesian insecurity was exposed. There was already a general flight underway out of everything into dollar cash and short-maturity dollars, driven by a growing realisation that the central banks’ comfort blankets were not emanating their usual reassuring smells. Interest rates and bond yields are now going to go higher, much higher.

Kwarteng has touched raw nerves in markets. His budget, perhaps, is the catalyst for an eventual rejection of Keynesian macroeconomics. But he will need to follow it up by cutting public spending, balancing the budget, and reducing the role of the state in the overall economy if Britain is to survive the financial holocaust he has triggered.

That kind of stimulus, permitting businesses and consumers to keep more of the fruits of their entrepreneurship and labour, is the path to lasting benefits for all. Instead of the disaster claimed by establishment Keynesians, it is actually a break for freedom. And the earlier it is done, the sooner the British economy will improve. This is forward planning for the next general election.

[i] Source: https://quotepark.com/quotes/1795588-nigel-lawson-we-had-to-dispel-the-notion-that-the-way-to-econom/

[ii] Bank balance sheet liabilities also include loans to them not classified as customer deposits as well as financial liabilities. The latter are more prevalent in G-SIBs than domestic banking. In practice, domestic banks will be under greater pressure to reduce lending and therefore deposits, while G-SIBs will be under pressure to reduce their exposure to financial markets.

More By This Author:

Gold Has Never Been So Attractive

Inflation Is Turning Hyper

An Asian Bretton Woods?

Comments

Log in or sign up to join the conversation.