Robust labor market conditions appear to be supported by solid consumer activity following the reopening of the economy. However, the unemployment rate is likely to rise over the next few months as the initial impulse gradually dissipates.

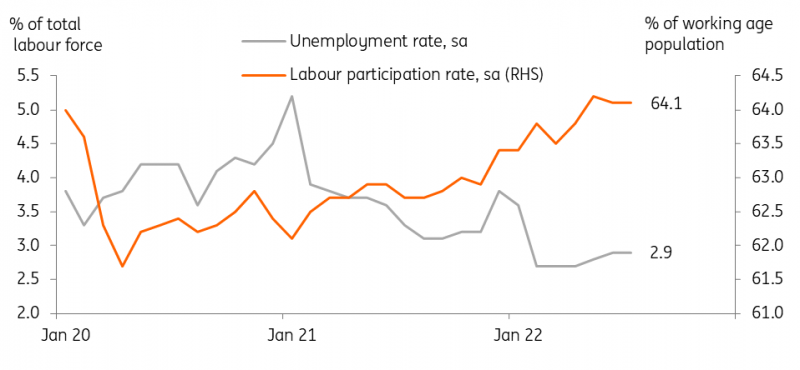

Unemployment rate stays at 2.9% in July, in line with market consensus

Despite the recent re-emergence of COVID-19 cases, the impact on people's mobility and consumption activity appears to be very limited. Labor market conditions have remained relatively healthy, benefiting from the reopening of the economy. Meanwhile, the labor participation rate stood at 64.1% for the second month, returning to the pre-pandemic level. Therefore, we believe that additional advances in labor participation should be limited from now on.

Both unemployment rate and labor participation rate unchanged in July

Source: KOSTAT

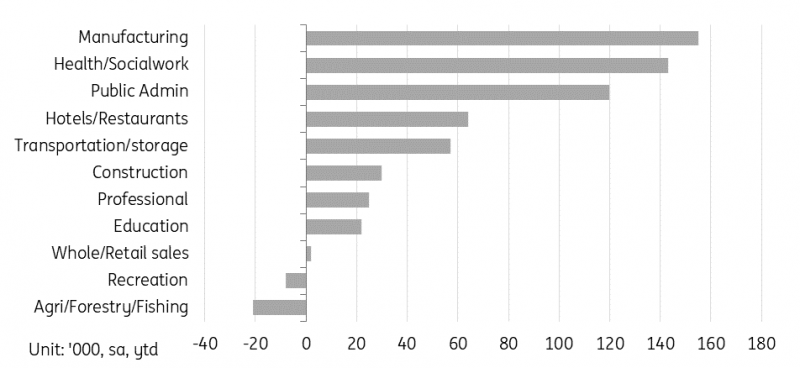

By industry, manufacturing added jobs for the second month while construction shed jobs the most in August probably due to the temporary suspension of a large-scale housing construction site. Among the services sector, hotels/restaurants continued to add jobs, but the recreation and transportation sectors lost jobs unexpectedly despite the holiday season. By employment type, the number of regular workers (with a contract of 12 months or longer) increased significantly, while that of daily workers (with a contract of less than one month) decreased. As such, we believe employment stability improved in July.

Manufacturing added jobs the most YTD 2022

Source: KOSTAT

Bank of Korea is expected to deliver 25bp hike in August

Today's labor market report shows that the economy remains resilient amid growing concerns at home and abroad. However, the recovery of consumption is expected to weaken and employment in major service sectors declined slightly amid a cloudy outlook. Therefore, we expect the Bank of Korea to return to its usual 25bp hike mode in August.

However, the main risk factor notable to our current BoK outlook is the price of fresh food. With recent bad weather and the full-moon holiday in September, fresh food inflation is likely to rise more than expected in the coming months. If August CPI inflation rises above the current 6.3% year-on-year rate (August ING forecast: 6.1%), we could consider a further 25bp increase in November or a 50bp increase in October.

More By This Author:

Hungarian Inflation Continues To Climb

Rates Spark: Following The US Data Cues

FX Daily: Window Of Carry Sees Renewed Interest In EMFX

Comments

Log in or sign up to join the conversation.