Photo by Jacek Dylag on Unsplash

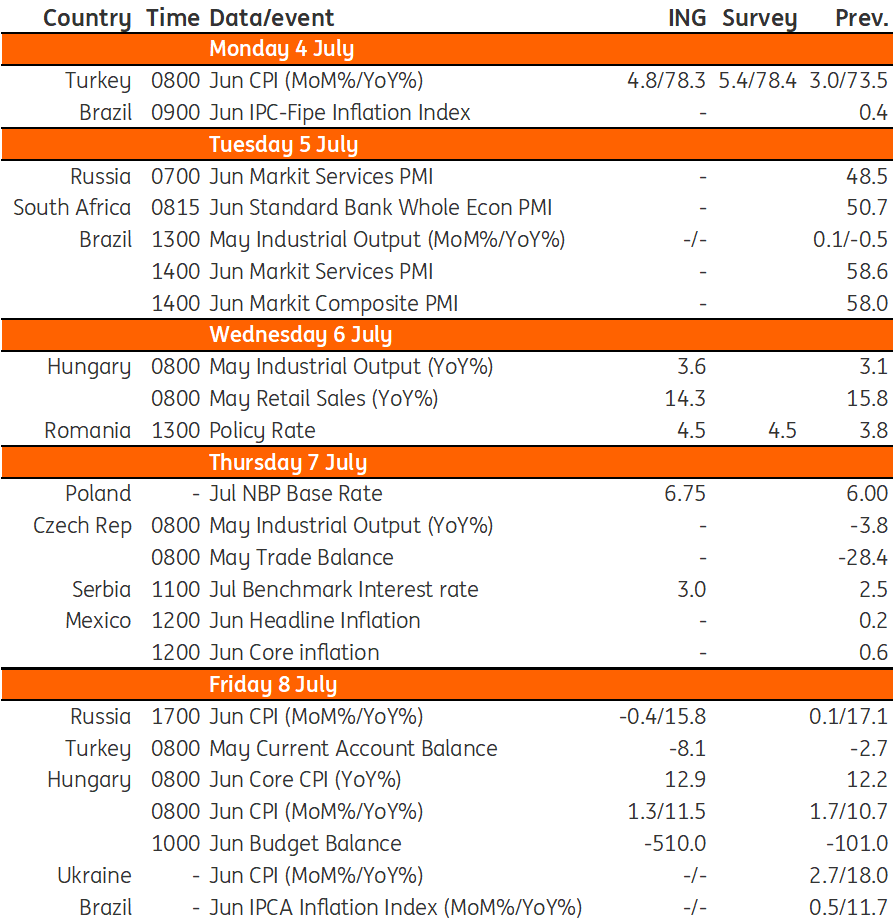

In Turkey, we expect annual inflation to further increase next week, while Poland's central bank is expected to deliver a 75bp rate hike amid ongoing inflationary risks.

Hungry: Higher than the historical average price increase

Next week will be quite dense in terms of data from Hungary. We expect some further slowdown both in retail sales and industrial production on a monthly basis in May. This would be in line with the latest changes in soft indicators. However, the year-on-year indices will be significantly skewed by base effects. Nonetheless, we don’t see any reason to worry about our above 5% 2022 GDP forecast. What will be even more important than the economic activity is the June inflation print. After causing a huge upside surprise in the previous month, we expect some slowdown in the monthly inflation reading. Yet, the 1.3% month-on-month price increase will be much higher than the historical average, showing the impact of rising producer prices, booming wages, and the high pricing power of companies. On a yearly basis, this will translate into an 11.5% headline figure, while core inflation is expected to be just shy of the 13% mark (as the majority of the price caps are effective in the non-core basket). Last but not least, we see the budget balance showing further deterioration due to seasonal patterns and the country’s rising energy bill.

Turkey: Further increase in annual inflation

We expect annual inflation for June to further increase to 78.3% (4.8% on monthly basis) from 73.5% in May, driven by food and transportation prices, while pricing pressures will likely remain broad-based with a largely supportive policy framework leading to currency weakness, and external factors weighing on import prices.

Poland: Upcoming central bank decision on rates

In May, National Bank of Poland (NBP) Governor Adam Glapiński suggested that monetary tightening is coming to an end, and conditions for rate cuts could arise already in 2023, yet price developments (CPI above 15%YoY in June) and inflationary risks call for another rate hike this month. What's more, the external environment leaves little room for doubts about the need to continue tightening. In June, the Czech National Bank hiked rates by 125bp and the Hungarian National Bank by 185bp, so the NBP is lagging behind with respect to the level of the policy rate. Therefore, we expect the monetary policy council to deliver a 75bp rate hike, however, markets may bet on an even more decisive policy move. Anything less than 75bp would lead to Polish złoty weakening.

EMEA Economic Calendar

Image Source: Refinitiv, ING

Comments

Log in or sign up to join the conversation.