Image Source: Pixabay

Poland’s current account surplus and Hungarian inflation figures are set to be the key highlights in a quieter week ahead in the EMEA region.

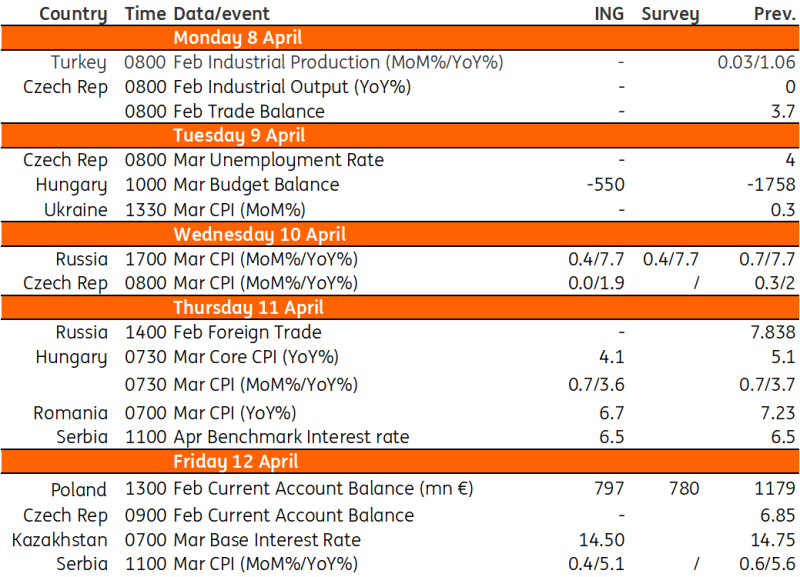

Poland: Current account surplus from strong trade in goods

Current account (Feb): €797m

We forecast a €797m surplus for Poland's current account in February 2024, but it will be smaller than in February 2023 (€147m) amid a deterioration in the foreign income balance. As a result, the cumulative 12-month current account surplus will narrow to 1.3% of GDP, down from 1.4% of GDP after January this year. Still, we expect a solid surplus in trade in goods, and we hope to see positive annual dynamics for both exports and imports.

Nevertheless, net exports are projected to contribute negatively to economic growth in 2024; the anticipated rebound in imports is expected to be stronger than the improvements seen in exports. The former will be fuelled by surging domestic demand and buoyant consumption, while the latter is likely to be curbed by weak external demand, particularly from Germany.

Hungary: March inflation to decelerate to 3.6%

In Hungary, we will see the latest budget figures for March as well as the March inflation print. On the fiscal side, we expect another monthly deficit but a much more consolidated figure than in the previous month. Some one-off burdens on the expenditure side will be taken off the books, and the revenue side is expected to improve as domestic demand slowly but surely strengthens. On the price side, we see another strong monthly repricing, with the third 0.7% print in a row.

Services will remain the main driver of monthly inflation, especially holiday packages and telecommunications services. On top of that, further increases in fuel prices will also add to inflationary pressure. Looking at the year-on-year rate, we see a further slight deceleration to 3.6% due to the still relatively high base. The lion's share of annual price increases (around 70%) will come from services inflation. The slight deceleration is the result of opposing forces, with fuel and household energy prices contributing positively to the change from February to March, while a change in food, alcoholic beverages and tobacco prices will weigh on the year-on-year reading.

Key events in EMEA next week

Refinitiv, ING

More By This Author:

FX Daily: Clues Vs. EvidencePhilippine Inflation Moves Higher As Rice Stays Pricey

Rates Spark: Rolling The Payrolls Dice

Comments

Log in or sign up to join the conversation.