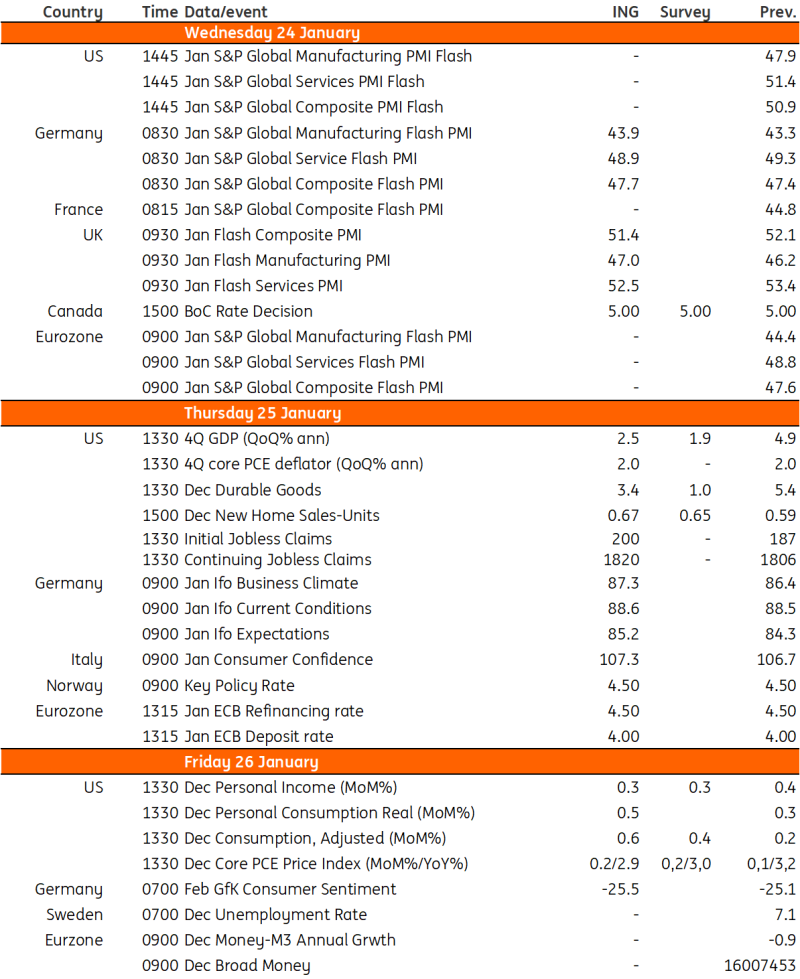

All eyes will be on the release of fourth-quarter US GDP figures on Thursday, which we expect to come in at around 2.5%. Over in the eurozone, the ECB will likely stress a focus on data dependency as markets gear up for rate cuts. In Canada, inflation looks set to soften further in the coming months and we're favouring rate cuts from the second quarter onwards.

Image Source: Unsplash

US: Fourth quarter GDP growth is expected to come in at around 2.5%

Market confidence in the March Federal Reserve interest rate call that had been fully priced in has waned over the past week and is likely to be pared back even further over the week ahead. We continue to favour May as the starting point for the first rate cut from the Fed. We expect fourth-quarter GDP growth to come in at around 2.5% on Thursday – and with the unemployment rate ending 2023 at just 3.7% and inflation still well above target in year-on-year terms, there seems to be little pressure to start cutting rates imminently. Fed officials do acknowledge that they will likely end up cutting interest rates this year, but they too are pushing back on the time and scale of that first move. Their individual forecasts suggest three 25bp rate cuts this year versus the 150bp of rate cuts markets are discounting.

While we disagree on the market’s timing of the first move, we too expect 150bp of rate cuts this year. Inflation in YoY terms is above the 2% target, but the December month-on-month core personal consumer spending deflator reading should come in below 0.2% for the sixth month out of the past seven. This is the key threshold that we consistently need to be under to be confident YoY inflation will return to 2%. The Fed itself suggests neutral policy interest rate is 2.5%, so we have 300bp to play with just to get back to “neutral”. Consequently, we see downside risks to the central bank's current prognosis and see the Fed funds rate ending this year at 4%, then hitting 3% in the first half of 2025.

Eurozone: ECB to stress data dependency as markets gear up for imminent rate cuts

Back in December, the European Central Bank basically announced the end of the current rate hiking cycle. Financial markets took that signal and the current economic weakness as clear signs of imminent rate cuts. However, even if actual growth continues to turn out weaker than the ECB had expected every single quarter, as long as the eurozone remains in de facto stagnation mode and doesn’t slide into a more severe recession – and as long as the ECB continues to predict a return to potential growth rates one or two quarters later – there is no reason for the central bank to react. Certainly not as long as inflation remains off target.

The irony of market pricing right now is that it makes the need for actual policy rate cuts less urgent. Financing conditions have eased since early December, doing the work that actual rate cuts should do, supporting growth but also pushing up inflation risks. Consequently, the more aggressive the market prices future rate cuts, the less needed and likely those cuts will be. At the same time, given the high degree of uncertainty surrounding both the growth and inflation outlook, any more explicit forward guidance the ECB might give next week could easily become outdated by actual macro developments. Therefore, the most likely outcome of next week’s ECB meeting will be to stress data dependency and to give some insights into potential conditions for a rate cut without pre-committing to anything.

Canada: Rate cuts from the second quarter onwards

Canadian core inflation came in hotter than expected in December and rules out the Bank of Canada shifting meaningfully in a dovish direction at the January policy meeting. However, higher interest rates are biting. The latest BoC Business Outlook Survey reported softening demand and “less favourable business conditions” in the fourth quarter with high-interest rates having “negatively impacted a majority of firms”, leading to most firms not planning to add new staff. As such, inflation looks set to soften further in coming months and so we favour rate cuts from the second quarter onwards, most likely starting in April.

Key events in developed markets next week

More By This Author:

Key Events In EMEA For The Week Of January 22Bank Of Canada Preview: Too Early For A Radical Pivot

The Commodities Feed: IEA Sees Well Supplied Oil Market

Comments

Log in or sign up to join the conversation.