The European Central Bank looks determined to follow in the Federal Reserve's footsteps. After the start of aggressive rate hikes, and with no end in sight yet, the next milestone is a reduction of its bond portfolio. However, we think the ECB's hawkishness might be premature. Quantitative tightening will come, but not just yet.

QT is on The ECB's Radar, But It's Still a Distant Prospect

The minutes of the ECB's September meeting delivered a couple of interesting insights: the decision to hike rates by 75 bps was not taken unanimously, so 75 bps increments should not be the new normal. However, the ECB was clearly determined to continue hiking rates significantly.

Also, looking beyond the configuration of the key ECB interest rates, the minutes underlined that the Eurosystem's large balance sheet was continuing to provide significant monetary policy accommodation by compressing term premia.

The Governing Council felt it appropriate to reiterate that it stood ready to adjust all of the instruments within its mandate to ensure that inflation returned to its medium-term target of 2%. This is a clear signal that reducing the ECB's balance sheet has become an issue.

Quantitative tightening (QT) - how to reduce the size of the balance sheet - was also apparently on the agenda at this week's non-monetary policy meeting in Cyprus. However, so far, no information has been leaked from this meeting.

A discussion is one thing, an actual decision is another. Just a little more than a week ago, ECB President Christine Lagarde said that the ECB would only start to consider QT when the ECB had completed its monetary policy normalization. At the same time, bond yields have already increased significantly in recent months without any QT.

Also, given the very uncertain economic outlook and more pressure on governments to deliver additional fiscal stimulus, QT at the current juncture could trigger an unwarranted widening of bond spreads, a.k.a, a new euro crisis. This is something the ECB clearly does not want.

A premature QT decision also has other risks. It could raise the bar for triggering the Transmission Protection Instrument (TPI) even higher, a development that could actually spark a new euro crisis. As such, an actual decision on QT is very unlikely as it would add to financial stress and uncertainty. However, it's good to at least have a plan for when this is really needed.

How the ECB's QT Could Work

Though quantitative tightening currently looks unlikely, it will come eventually. Given the complicated structure of the ECB's bond purchases across countries, sectors, and durations, an outright selling of the bond portfolio will not be an easy one without disturbing markets. Also, don't forget that the ECB's balance sheet not only comprises the bond portfolio but also the series of liquidity operations to support bank lending.

These bank lending operations (TLTROs) will be repaid by banks, automatically reducing the balance sheet. Still, when financial markets think of QT, they think of reversing the ECB's asset purchases. In this regard, the option of gradually and more passively reducing its asset portfolio looks the most attractive.

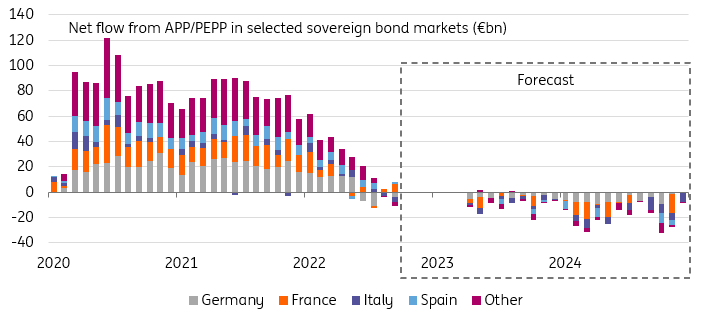

A possible first step would be to (gradually) stop the reinvestments of the Asset Purchase Program (APP). One way to phase in QT would be to first cap APP reinvestments at 50% of their normal amount during, say, the second and third quarters before ending them in the fourth. In this scenario, the resulting balance sheet reduction would be a manageable EUR155 billion in 2023, doubling to EUR300 billion in 2024.

The next step would be to end the reinvestments under the Pandemic Emergency Purchase Program (PEPP). These would add to the balance sheet reduction in 2025, leading to a total reduction of EUR388 billion (along with the APP reductions). In addition, the ECB could speed up the process with outright sales, but we doubt peripheral bond markets would be able to stomach the impact.

In terms of timing, we take Christine Lagarde's recent comments for granted and expect a gradual end to the APP reinvestments between Q2 and Q4 next year. PEPP reinvestments will stop by the end of 2024.

QT Could Reduce the ECB's Balance Sheet by EUR155 Billion in 2023 and EUR300 Billion in 2024

Refinitiv, ING

Whenever it happens, we expect QT to be felt across three dimensions of rates markets: duration, credit (and sovereign) premia, and money markets (through the price of liquidity).

Impact on Core Yields: Moderate at the Start

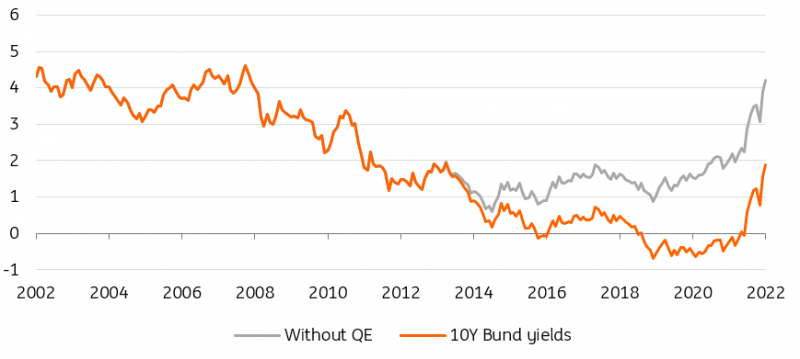

One of the channels through which QE influenced markets was by suppressing the compensation for a certain number of risks, including duration risk. At face value, this means that, when the ECB reduces its balance sheet, long-dated yields will rise. So far so good. There is empirical evidence for that.

For reference, we find that a EUR155 billion reduction in the ECB's bond portfolio size in 2023 would push 10-year Bund yields up by only 7 bps, and a EUR300 billion reduction in 2024 would reduce them by 14 bps. If this sounds unimpressive, note that without the EUR5 trillion of ECB purchases, 10-year Bund yields would be 230 bps higher by this, admittedly rough, estimate.

Note also that QT would add to the amount of debt that private markets would have to absorb if European governments were to significantly increase their borrowing to finance energy support packages. This is another argument for a delayed start to QT.

What is much more difficult to track is the impact this will have on the shape of the yield curve. On paper, the longer the maturity point, the more QE suppresses yields. We're not expecting a re-steepening as a result of QT, however.

The experience of the US and UK has shown that yield curves can invert even in the context of QT. The reason is that other factors have a greater influence, namely that base rates are going above their long-term neutral levels. In short, we're still expecting a German curve inversion next year irrespective of QT.

Without QE, 10-Year German Bund Yields Would Be Over 200 Bps Higher

Refinitiv, ING

Sovereign Spreads: Adding Fuel to the Fire

When one moves away from so-called ‘risk-free’ markets, the main impact of QE is suppressing credit compensation. In the case of sovereign bonds, QE was instrumental in suppressing eurozone break-up risk in the sovereign crisis of 2010-12, and in subsequent periods of market stress.

Our analysis of German yields above implies that the stock rather than the flow of purchases is the relevant variable to assess market impact. This isn’t so simple for sovereign spreads, where both variables matter.

In plain English, we think the impact of QT on sovereign spreads will occur a lot faster than on core yields, once flows turn negative. This explains why spreads already started widening before QT was even discussed, as QE purchases drew to a close in mid-2022. We fear the ECB following through with QT would compound the worries of already stressed financial markets.

We struggle to see how peripheral markets would cope with rising interest rates and QT at the same time. This is a key reason why we expect QT to start only once the phase of rising base interest rates is over. Additionally, the ECB keeping spread-support programs, such as the TPI, at hand would go some way to reassuring markets. It would also mean a slower reduction in the ECB's bond portfolio if it is forced to temporarily buy peripheral bonds.

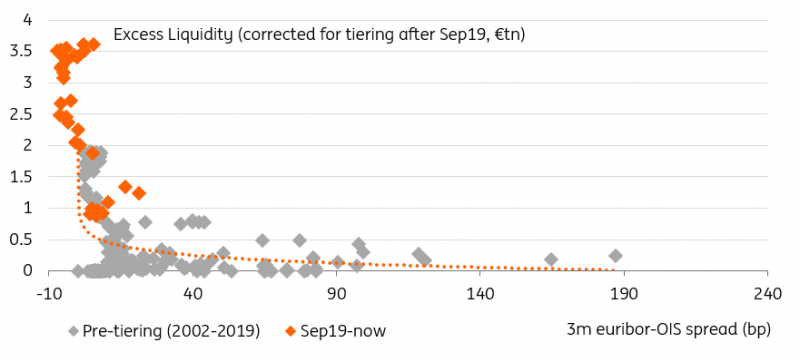

QT Will Reduce Excess Liquidity and Help Widen Money Market Spreads, such as Euribor

Refinitiv, ING

Money Markets: Taking Away the Comfort Blanket

A large chunk of money market rates also has a credit and duration component, which we covered in the sections above. But the compensation in money markets is even more heavily suppressed by the tide of ECB Excess Liquidity (EL) introduced during successive rounds of QE and loans to banks (TLTROs).

As QT begins, EL will shrink by the same amount. In 2023, the estimated EUR155 billion reduction in excess liquidity from QT will pale in comparison to the nearly EUR2 trillion reduction coming from targeted longer-term refinancing operations (TLTRO) loan repayments.

After that date, however, each incremental reduction in liquidity will make money market rates more sensitive to other risk factors. The widening of money market spreads, for instance Euribor fixings compared to overnight index swaps (OIS), is not linear.

The first EUR2 trillion reduction will probably have little effect. After that, at the latest after mid-2023, the impact of EL reduction will accelerate. This effect could even be magnified if the ECB decides to effectively lock away a portion of EL using tiered bank reserve remunerations.

More By This Author:

German Economy Weakens In AugustAnother Inflation Shocker From Germany

Germany: September Ifo Sends More Recessionary Signals

Comments

Log in or sign up to join the conversation.