Fully stocked warehouses, the higher cost of working capital, and a gradual return of just-in-time management will likely weigh on inventory building in the coming months. That will be a modest headwind for economic growth in the first half of the year.

From just-in-time to just-in-case

The last few years have been crazy times for inventory managers. After a long trend of declining inventory-to-sales ratios on the back of more integrated supply chains and “just-in-time management” the pandemic proved to be a brutal wake-up call. Suddenly companies were confronted with disrupted supply chains and shortages of inputs. And this was at a time when consumers spent much more on goods (especially durable goods) because of services consumption being hampered by lockdowns. The scramble for inputs, fostered by a new “just-in-case-management” philosophy might even have led to a “bullwhip effect”: a situation where firms, in the wake of uncertainty, order more inputs than they actually need. This of course added to economic growth.

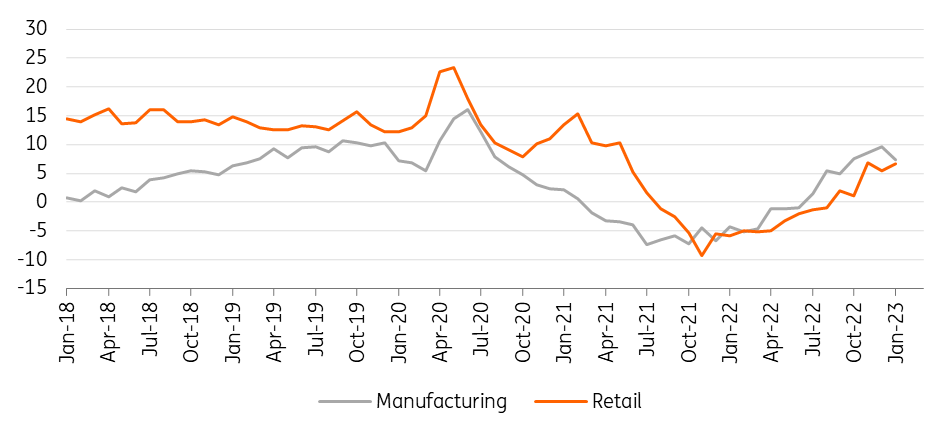

Industry and retail survey: volume of stocks

Image Source: Refinitiv Datastream

Services strike back

However, from the end of 2021 onwards consumer demand started to soften on the back of rising energy prices, and with the pandemic petering out, a gradual shift from goods consumption to services took place. People preferred to go on holiday or dine out at a restaurant than spend money on yet another fitness tool for the home gym in the attic. No wonder the assessment of inventory levels at factories and retailers, which were deemed low at the end of 2021, is now rather high. With fewer supply chain hiccups and delivery times falling, there is also less need to hold high inventory levels. On top of that, the significant increase in the cost of working capital, courtesy of ECB tightening, is also pushing companies to be more efficient in their inventory management. The PMI report for February signaled a sharp drop in purchases by factories as firms remained focused on inventory reduction.

Modest headwind

How will this impact GDP growth? Inventories are a strange animal in GDP accounting as it is not the level of inventory building that impacts GDP, but the change in the speed of stock building. In other words, companies don’t need to destock to have a negative impact on growth, they just need to add less to inventories than in the previous period. To make things even less transparent, inventories in the GDP accounts also include two completely unrelated items, namely discrepancies (a “residual” component) and the net acquisition of valuables. That makes it even more difficult to forecast. That said, based on a number of survey indicators, we think that inventories might shave off 0.5 percentage points from year-on-year GDP growth in the first quarter. However, net exports will probably partially compensate for this as inventory building usually has a big import component. The bottom line is that inventories are likely to be a modest headwind in the first half of the year, but not sufficient to halt the expansion.

More By This Author:

FX Daily: Geopolitical Risk Strikes BackEurozone PMI Shows Strong Increase In February

Rates Spark: Looking Backward To Economic Data And Forward To Geopolitics

Comments

Log in or sign up to join the conversation.