The UK economy in 2024 presents a blend of promising growth figures and underlying concerns, leaving many to wonder: Is this a sustainable rebound or merely a temporary upswing?

While the country has shown resilience in recovering from recent economic challenges, a closer look reveals potential vulnerabilities that could undermine this progress.

Key factors such as retail performance during the men’s Euros football tournament, political uncertainty, and the direction of inflation are crucial to understanding the true state of the UK economy.

Economic growth: Strong numbers, but for how long?

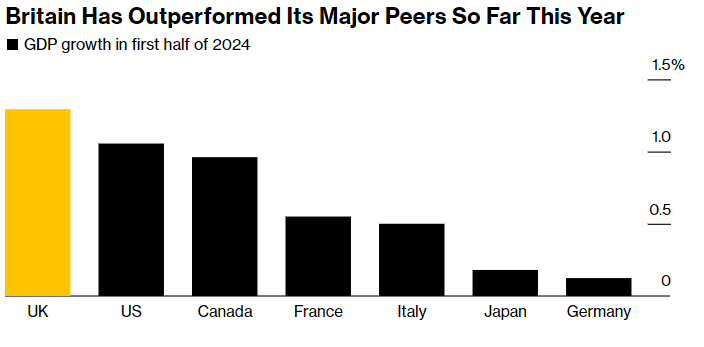

In the first half of 2024, the UK economy posted robust growth, outpacing its G7 peers and offering a glimmer of hope for sustained recovery.

The Office for National Statistics (ONS) reported a 0.7% GDP increase in the first quarter, followed by a 0.6% rise in the second quarter, signaling a strong economic performance compared to other major economies like the U.S., Japan and Germany.

(Click on image to enlarge)

Source: ONS, Eurostat, Bloomberg

However, the Bank of England (BoE) remains cautious about the sustainability of this momentum. Despite these encouraging figures, business surveys suggest that the economy’s underlying strength may not be as solid as it appears.

The growth observed in the first half of the year might be masking deeper issues, such as labor market constraints and a longstanding productivity problem, which could hinder the economy’s ability to maintain this pace in the long run.

Football’s effort to revive retail spending

July saw a significant boost in retail sales, providing a much-needed lift after a sluggish June. The ONS reported a 0.5% increase in retail sales volumes, largely driven by consumer spending linked to the men’s Euros football championship and summer discounts that enticed shoppers back to the high streets.

However, this apparent retail recovery is more complex than it seems. Despite the July uptick, sales volumes remained 0.8% below their pre-pandemic levels in February 2020.

Moreover, the recovery across retail sectors has been uneven. While department stores and sports equipment shops benefited from the Euros, clothing retailers experienced a 0.6% decline in sales volumes.

This mixed performance indicates that while consumer spending is returning, confidence remains fragile, particularly in sectors dependent on discretionary spending.

What lies ahead for inflation and interest rates?

Inflation has been a persistent concern in the UK over the past two years, but recent months have shown signs of relief. After peaking in 2022 and 2023, inflation has now eased to around the BoE’s target of 2%. In July, inflation slightly exceeded this target, but wage growth in the second quarter outpaced inflation by the widest margin since mid-2021.

In response, the BoE cut interest rates earlier this month, reducing them from a 16-year high. This move aims to support continued economic growth and consumer spending.

However, the BoE remains cautious; cutting rates too aggressively could reignite inflation, particularly if economic growth outstrips sustainable levels, further highlighting the uncertainty that still looms over the UK economy.

New government, same challenges?

The recent victory of the Labour Party under Keir Starmer introduces new dynamics into the UK’s economic outlook. Starmer’s government has vowed to “take the brakes off Britain” by implementing reforms aimed at boosting growth and addressing long-term economic challenges. These include changes to planning regulations and efforts to increase labour market participation, particularly in the wake of significant workforce reductions following the pandemic.

While these initiatives are ambitious, they must confront deeply rooted issues such as low productivity and underinvestment, problems exacerbated by Brexit and ongoing global economic uncertainty.

Achieving sustained high growth will require more than just policy adjustments; it will necessitate a comprehensive approach to resolving these structural weaknesses that have long hindered the UK economy.

Additionally, the new government’s push for reforms could benefit sectors like construction and infrastructure, but the impact of these changes will take time to materialize.

As such, while there is a growing optimism in the UK economy, investors would be wise to not get ahead of themselves and wait for further positive signals.

In conclusion, while the UK economy in 2024 shows encouraging signs of recovery, the underlying challenges highlighted by the BoE and the uneven retail recovery indicate that this is not the time for complacency.

A new political regime in the country could shift the narrative either way, but as of now, UK citizens and investors have reasons to be optimistic.

More By This Author:

Asia-pacific Markets Edge Up As China Maintains Loan Prime RatesRio Tinto, BHP Shares Are At Risk As Iron Ore, Copper Prices Sink

Nio Stock Price Analysis: Brace For A Key Event On Aug. 22

Comments

Log in or sign up to join the conversation.