Image Source: Pexels

Although services inflation continues to be a concern, the recent decline in overall inflation has brightened Hungary’s near-term inflation outlook. Consequently, we have revised our CPI forecasts for 2024 and 2025 downward, albeit with some risks for the coming year. The door is now open for a September rate cut by the central bank.

Flat prices in August are a welcome surprise

Inflationary pressures in Hungary eased in August. The latest data was better than expected when compared to the market consensus. Year-on-year inflation fell from 4.1% to 3.4% in August. The further moderation in inflation was partly due to the stagnation of the average price level on a monthly basis (MoM) and the high base from last year. Therefore, the strong monthly increase in July seems to have been an exception, as the stagnation in the monthly inflation rate seen in previous months has returned.

In recent months, inflation has been contained mainly by favourable developments in items outside the core inflation basket, and in August the main items of core inflation also turned more favourable. How long this will last remains to be seen, but the inflation picture is certainly improving.

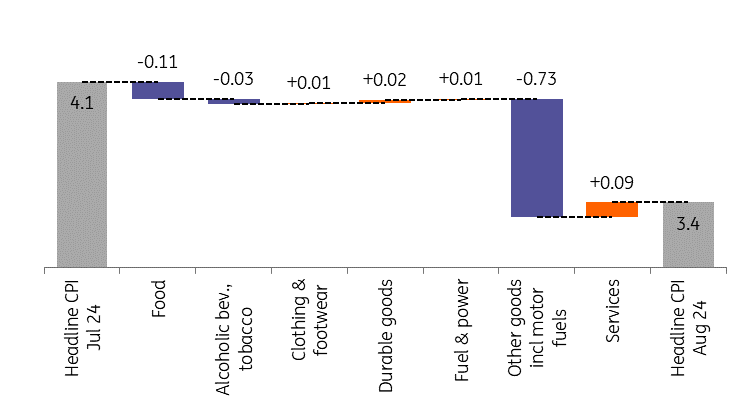

Main drivers of the change in headline CPI (%)

Source: HCSO, ING

The details

- Food prices did not continue to rise in August (0.0% MoM) after a surge in July (0.6% MoM), meaning that the removal of price caps and the end of mandatory in-store discounts appear to have led to a one-off repricing rather than a sustained, trend-like price increase. As a result, food inflation slowed to 2.4% YoY.

- Fuel prices fell sharply in August (-0.8% MoM), following a sharp rise in July, which was widely expected. The contribution to the turnaround in inflation is therefore also significant. On the other hand, the 0.1% monthly fall in household energy is clearly a surprise, contrary to the expected rise.

- Prices of durable goods rose by 0.1% on a monthly basis, in line with the global easing of pressure on these items due to lack of demand. At the same time, the price of clothing and footwear fell by 1.3% MoM, the largest fall since January.

- Services should also be included among the items improving the short-term inflation picture. On a monthly basis, the increase was only 0.4%. However, due to an exceptionally low base last August, the year-on-year figure rose to 9.5%. This means that services inflation accounts for 73% of headline inflation.

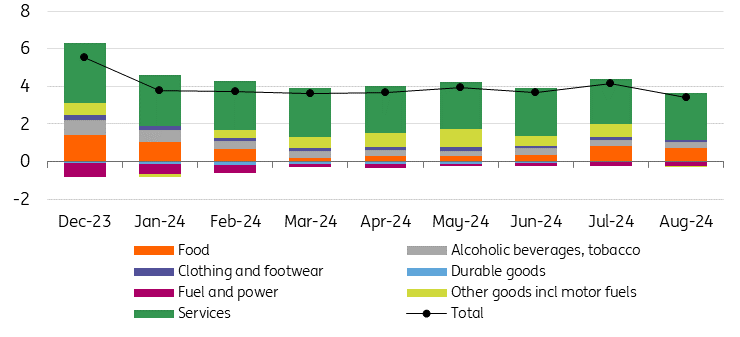

The composition of headline inflation (ppt)

Source: HCSO, ING

Good news as the underlying inflation picture stabilises

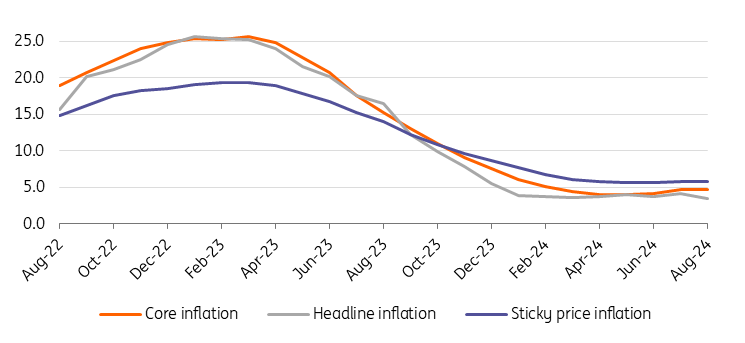

Contrary to expectations, the core inflation indicator did not rise but fell slightly compared with July. The 0.3% month-on-month increase is close to the inflation target on an annualised basis. With this moderated repricing of the core basket, year-on-year core inflation was 4.63%, an improvement of 0.04ppt on the previous month. So the slowdown was just enough to help reduce the indicator due to rounding to one decimal place.

The good news continues with the National Bank of Hungary's measure of sticky price inflation, which remained unchanged at 5.8% year-on-year in August. Moreover, an important short-term indicator, the three-month annualised core inflation measure (3M/3M saar), has declined. Therefore, we can conclude that several indicators signal that the underlying inflation picture is at least stabilising, although there is still work to be done from a monetary policy perspective.

Headline and underlying inflation measures (% YoY)

Source: HCSO, NBH, ING

We revise down the inflation path

Looking ahead, we expect next month's inflation to be broadly similar to today's, with perhaps some moderation. Thereafter, however, the year-on-year rate could rise more sharply due to the low base. From October it could temporarily exceed 4% again. Looking at current inflation trends, we see the rate of price increases creeping back up to 4.8% by December 2024. This implies a significant downward revision on our part (from the 5.0-5.5% forecast range).

Given today's services inflation and the August fiscal data, we believe that the Hungarian economy could perform even more weakly in the second half of this year than previously expected. This will limit the ability of companies to reprice meaningfully, even in an environment where they face significant cost increases.

In the short term, therefore, inflationary pressures from the domestic demand side are unlikely to be significant. At the same time, inflationary risks are rising next year: the expected pick-up in consumption, continued dynamic wage growth (especially after a possible further significant increase in the minimum wage in 2025) and the government's recent tax measures are likely to be passed on to consumers in the form of price increases next year. We expect average price increases of 3.8% in 2024 and 4.2% in 2025.

The door is open for a 25bp cut in September

From a Hungarian monetary policy perspective, the incoming inflation data opens the door for a 25bp rate cut in September. A 50bp cut by the Fed (our low-conviction base case) and a dovish tone from the ECB (alongside its 0.25ppt rate cut) would reinforce this call.

On the other hand, "only" a 25bp cut by the Fed and a hawkish message from the ECB that the September cut will certainly not be followed by another one in October would make the decision between a hold and a 25bp cut in Hungary a bit more nuanced.

Ultimately, the EUR/HUF exchange rate could be the deciding factor and here the latest negative news (renewed and escalating disharmony between the government and the National Bank of Hungary) increases the country’s risk premium, which is also a key factor in the careful, patient and now stability-oriented monetary policy.

More By This Author:

Asia Morning Bites For Tuesday, Sept 10Think Ahead: Great Minds Think Alike

US Payrolls Fails To Resolve The 25 Or 50bp Rate Cut Call

Comments

Log in or sign up to join the conversation.