Tuesday, June 8, 2021 8:50 AM EDT

Despite the reopening, the central budget posted a significant shortfall in May. Expenditures are mounting on a new set of measures to re-start the economy.

People on the Széchenyi Chain Bridge, Budapest

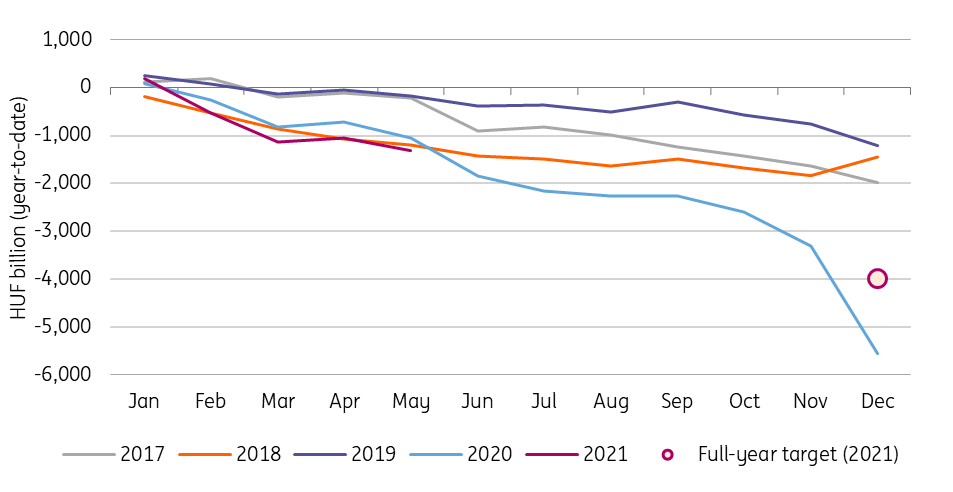

Hungary's budget posted a HUF 269bn deficit in May 2021. This can be seen as a slight negative surprise as we expected the higher revenues from reopening to counterbalance the expenditure impact of stimulus measures. With the May shortfall, the year-to-date budget sits at HUF 1.3126tn, reaching 33% of the adjusted deficit plan. In this respect, we don’t need to push the panic button.

Cash-flow based year-to-date central budget balance

(Click on image to enlarge)

Ministry of Finance, ING

When it comes to the revenue side, the ministry highlighted that during the first five months of 2021 revenues from corporate, value added and personal income and social security taxes increased on a yearly basis. This hardly comes as a surprise considering the effect of the pandemic and the reopening this year.

On the expenditure side, the ministry didn’t share details about the extra spending. It only highlighted that the budget ensures the resources necessary to re-start the economy. In practice, this means some tax reductions as well as support for cheap loans and ramping up investment activities.

The government officially amended the deficit goal to 7.5% of GDP and eyes a 79.9% debt-to-GDP ratio in late May. However, these figures are based on a quite outdated macro projection which forecasts only 4.3% GDP growth in 2021 with 3.6% inflation. The reality however could be economic activity above 7% paired with a 4.4% average price increase. This would mean extra revenues for the budget compared to the plan, as well as a higher nominal GDP, so a higher denominator in the fiscal ratios.

Against this backdrop, the only question remains what the government would like to do with the extra wiggle room during the fourth quarter. Considering that Hungary is facing a parliamentary election in spring 2022, we think the government leans towards spending the extra money and reaching the fiscal goals, rather than using the cash to reduce the deficit and debt at a faster pace.

Disclaimer: This publication has been prepared by the Economic and Financial Analysis Division of ING Bank N.V. (“ING”) solely for information purposes without regard to any ...

more

Disclaimer: This publication has been prepared by the Economic and Financial Analysis Division of ING Bank N.V. (“ING”) solely for information purposes without regard to any particular user's investment objectives, financial situation, or means. ING forms part of ING Group (being for this purpose ING Group NV and its subsidiary and affiliated companies). The information in the publication is not an investment recommendation and it is not investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Reasonable care has been taken to ensure that this publication is not untrue or misleading when published, but ING does not represent that it is accurate or complete. ING does not accept any liability for any direct, indirect or consequential loss arising from any use of this publication. Unless otherwise stated, any views, forecasts, or estimates are solely those of the author(s), as of the date of the publication and are subject to change without notice.

The distribution of this publication may be restricted by law or regulation in different jurisdictions and persons into whose possession this publication comes should inform themselves about, and observe, such restrictions.

Copyright and database rights protection exists in this report and it may not be reproduced, distributed or published by any person for any purpose without the prior express consent of ING. All rights are reserved. ING Bank N.V. is authorised by the Dutch Central Bank and supervised by the European Central Bank (ECB), the Dutch Central Bank (DNB) and the Dutch Authority for the Financial Markets (AFM). ING Bank N.V. is incorporated in the Netherlands (Trade Register no. 33031431 Amsterdam). In the United Kingdom this information is approved and/or communicated by ING Bank N.V., London Branch. ING Bank N.V., London Branch is deemed authorised by the Prudential Regulation Authority and is subject to regulation by the Financial Conduct Authority and limited regulation by the Prudential Regulation Authority. The nature and extent of consumer protections may differ from those for firms based in the UK. Details of the Temporary Permissions Regime, which allows EEA-based firms to operate in the UK for a limited period while seeking full authorisation, are available on the Financial Conduct Authority’s website.. ING Bank N.V., London branch is registered in England (Registration number BR000341) at 8-10 Moorgate, London EC2 6DA. For US Investors: Any person wishing to discuss this report or effect transactions in any security discussed herein should contact ING Financial Markets LLC, which is a member of the NYSE, FINRA and SIPC and part of ING, and which has accepted responsibility for the distribution of this report in the United States under applicable requirements.

less

How did you like this article? Let us know so we can better customize your reading experience.