We’ve long stated the importance of a robust telecom industry in the EU, and the much-anticipated Draghi report echoes that view. Revenues have dropped in recent years, and a strong financial profile will be crucial for navigating challenges and boosting investments – something that companies like Telefonica and BT should keep in mind

View of the Telefónica Building in Madrid, Spain

The EU telecom industry needs more meat on the bones

It's no secret that several European sectors are currently facing a host of individual challenges and collective headwinds – and the telecom sector is no exception. The European Commission's long-awaited report on European competitiveness – steered by former president of the European Central Bank, Mario Draghi – sheds light on the intricacies of those challenges. Over time, European telecom companies have accepted a lower creditworthiness, primarily due to competition policy put in place to achieve lower consumer prices.

But while lower credit ratings were generally acceptable in an ultra-low interest rate environment, funding costs are now moving up, and we think it's time for some companies to pay closer attention to their cash flow profiles.

In this article, we delve into why and how higher-rated telecom operators are better positioned to withstand risks from competition and higher interests than high-yield companies with lower credit ratings.

We've recently witnessed severe financial stress at Altice France, while Italy and Denmark have lost their incumbent, integrated telecom operators. Telecom Italia, for instance, has been broken up into a network company and a consumer-facing services business. We also saw this in Denmark a couple of years ago. Telefonica is another company also at risk of being broken up in the coming decade, while companies in the UK need better cash flows to be able to accelerate investments. For example, we expect that clearance of the Vodafone-Three merger will aid investments in the UK. It's also interesting to note that BT has a relatively weak cash flow profile, while TalkTalk's financial distress is a further testament to the competitiveness of the UK market. In short, more leverage comes at a cost – which Altice France and TalkTalk are now finding out.

Strong competition reduced the health of telecom companies

Over the years, we have witnessed strong competition in European telecom markets, driven by regulation. But while strong competition laws successfully lowered consumer prices, they also had a detrimental effect on the profitability of some companies. We provide examples of steep, annual declines in profitability below.

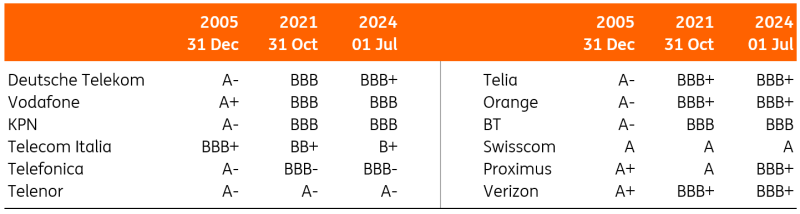

As we can see in the charts below, the credit quality of telecom companies took a hit from 2005 until approximately 2021. However, more recently, the ratings have largely stabilised. Explanations for this include an improved competitive environment due to new commercial strategies around fibre upselling. Profitability and cash generation were also aided by lower interest costs, largely driven by central bank policies. But the monetary environment with ultra-low interest rates was probably a one-off, and there is no certainty that price competition remains at bay.

Our research shows that companies with (strong) investment grade ratings are well positioned to weather headwinds while high-yield companies may find themselves cornered, especially if they have sold their assets.

Credit ratings have stabilised

Source: S&P ratings

Strong investment grade companies can withstand headwinds easily

Around the turn of the century, it was common for telecom companies to operate with modest leverage and a strong single A rating, reflecting excellent profitability, a strong balance sheet, healthy cash flows and, sometimes, government ownership. This helped to mitigate the pressure on the industry that would play out in subsequent years. Regulatory action has substantially reduced profitability in the sector since the turn of the century. Most measures were focused on increasing competition but regulators have also regulated wholesale broadband access and roaming tariffs. Moreover, spectrum auctions have often been expensive, while sometimes allowing for new operators to enter the market. These measures together have reduced the profitability of telecom operators.

At the same time, investments in fibre networks and new mobile technologies reduced free cash flow as capital expenditures went up. Many incumbent operators see better profitability from fibre-based fixed/mobile-coverged products (bundles combining a fixed broadband and mobile products) but we see no large increase in free cash flow generation. This is probably caused by a need for further investment in fixed and fibre networks, as investments have not yet been completed in many countries.

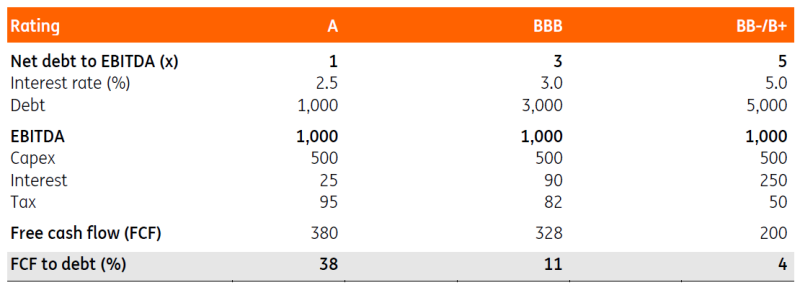

Before the regulatory action, free cash flow generation was high for companies with relatively low leverage, as shown in the figure below. For a single A-rated company (second column), Free Cash Flow could almost be approximated by EBITDA-Capital expenditures given low interest costs (where EBITDA is a measure of profitability and a proxy for operating cash flow generation before paid taxes). Cash taxes were another notable expense line weighing on cash flows.

This healthy cash generation matters a lot when EBITDA comes under pressure, as we have seen historically. We’ll provide some examples below. Obviously, Free Cash Flows are lower when companies are more indebted. This can be seen in the far right column, for a BB-/B+ rated company. The Free Cash Flow-to-Debt ratio, in particular, is lower for more leveraged companies. A solid ratio matters if a company wants to pay down debt from free cash flow. This is necessary when leverage needs to be stabilised in the event of an EBITDA decline. One could argue that free cash flow yields improve once network upgrades are completed. Nevertheless, there will remain a notable difference among the very financially-sound companies and telecom operators relying more on debt funding.

Lower ratings imply weaker cash flows (stylised example)

Interest expenses consume most FCF

Source: ING

Note that the indicated rating also depends on the strength of the business profile

Companies with a low rating have less meat on the bones

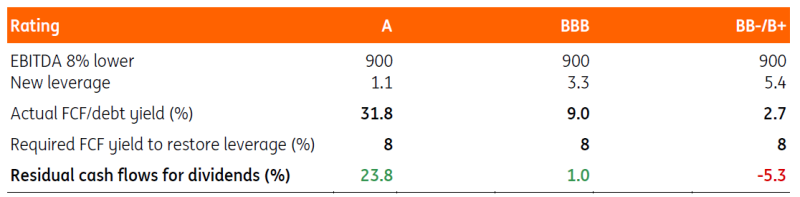

As illustrated in the stylised example, companies with a lower rating have less meat on the bones. Operating profitability is the same. However, the company generates less cash because the higher indebtedness requires it to make larger interest payments. In the example above, one sees that free cash flow is €180 lower (€380 versus €200) because of higher interest payments (balanced by somewhat lower taxes). When evaluating the free cash flow-to-debt ratio, one sees that the ability to reduce leverage from cash flows is more challenging. While an A-rated company could pay down all its debt within three years, it takes much longer for a BB-/B+ rated company. More leveraged business models are often dependent on EBITDA expansion to reduce leverage. Nevertheless, when an industry faces strong underlying headwinds, strong free cash flow yields can be a cornerstone for a company.

Material declines in EBITDA do happen

The European telecom industry is no longer the golden goose it was in my teenage years. Below, we’ll briefly provide some examples of companies that faced material headwinds to EBITDA. We focus on TDC and Telecom Italia. In the past, these companies suffered a lot from regulation and fierce competition. TDC reported a domestic decline in EBITDA of -12.7% in 2016 and -10.5% in 2015. Telecom Italia reported a domestic EBITDA decline of -9.8% in 2013, -9.6% in 2014, -20.6% in 2015 and -12.8% in 2021.

Outside Denmark and Italy, Altice France reported a -7.6% YoY EBITDA decline in the second quarter of this year. Below, we’ll show how this impacts the leverage of companies. We deem it especially interesting to evaluate the impact from different degrees of initial leverage. But it is also a warning sign to telecom regulators that the telecom marketplace needs to remain profitable. A focus solely on lower consumer prices leads to the break-up of telecom companies, eventually.

Leverage increases by 8% if EBITDA drops by -8%

Unless cash flow is used to lower debts

Source: ING

Indebted companies are challenged in the event of headwinds

Let’s analyse how companies with different degrees of indebtedness are impacted by a substantial -8% EBITDA decline. In the figure above, we provide some stylised figures again.

In this table, you can find the Free Cash Flow-to-Debit ratio taken from the examples in the earlier figure. As discussed previously, these ratios are much better for companies that have incurred low levels of debt, with an A-rated company being able to redeem c.32% of its debts out of generated cash flows (assuming there are no dividend payments). For a company with a BB-/B+ rating, this ratio is only 2.7%, because interest expenses are higher. This matters a lot when EBITDA declines, in our example by 8%. To stabilise the Debt-to-EBITDA ratio at the level before the shock to EBITDA, debts need to decrease by 8% as well. As the example above shows, this can be done within a year for companies with a FCF-to-Debt yield above 8% – companies with an A or BBB rating. However, for a company with a FCF-to-Debt ratio below 8%, leverage will increase following the drop in EBITDA from the example.

Of course, one could make the analysis somewhat more realistic by introducing dividend payments and longer time horizons to reduce debt. Nevertheless, we prefer to keep matters simple and just want to show that there are material differences in the ability of companies to handle balance sheet pressure. We will briefly touch upon the possibility of asset sales below. A strong asset base – such as ownership of networks and towers – has always provided comfort to lenders, as it acted as collateral.

Trade-off return on equity versus cost of debt

In this article, we purposely do not discuss the higher return on equity derived from higher leverage as we want to explain the debt trap companies may find themselves in once EBITDA comes under pressure. It is, however, straightforward that the cost of debt rises with higher leverage. Rating agency S&P provides data for the step-up in interest costs for corporate credit issuers. Looking at recent data, credit spreads increase by more than 2% when firms go from an A- to a BB- rating. This reflects a double-digit percentage point increase in spreads for every notch downward from BBB+ to BB.

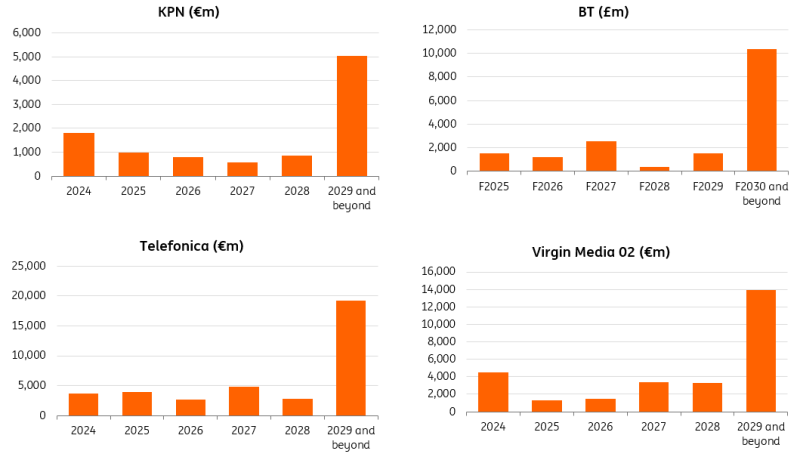

Debt maturities have been termed out

Despite the argument made above that risks increase with higher debt levels, we also like to note that the impact of higher market interest rates on the P&L occurs slowly. That is because most companies in the TMT space have termed-out their debt profiles during the era of low interest rates. When looking at the debt redemption profiles, one can see that the bulk of maturities comes after five years. Note that one-year liabilities are often substantial because they could include payables. Nevertheless, annual redemptions of senior debt are a fraction of the total outstanding liabilities. Therefore, the impact of higher funding costs will materialise slowly.

Debt maturities have been termed out

Source: Companies' data

Other potential action to improve the balance sheet

Of course, other action is possible to restore balance sheets or enhance free cash flow. Cash expenditures could be lowered to enhance free cash flows – although this is not good for network quality and the competitive position, and in turn, this measure therefore erodes the business profile. In our example, we have already set the dividend to zero, but relatively high dividends often reduce the amount of cash flows available for debt reduction further. The dividend payout ratio for telecom operators is a potential topic for a separate discussion.

Finally, asset sales used to be part of the risk mitigation plan. Historically, investors took comfort from a strong asset sales base, the selling of which could be used to shore up financials. Telefonica is a company that has sold towers and (minority interests) in other assets. Proceeds were intended to reduce indebtedness, with limited success, as leverage remains high. Part of the explanation is that companies that sell towers have to incur higher lease expenses, reducing free cash flows. Going forward, we have to see how asset-light business models will fare. Telecom Italia no longer owns its fixed network, which will be an interesting litmus test.

For Altice France, leverage was too much

Investors in Altice France were spooked when the company announced its intention to bring the proceeds from asset sales outside of their borrowing group. While few investors doubt that leverage at Altice France is too high right now, our point is that other companies could find themselves cornered as well if enough attention is not paid to risk management and financial leverage. Solid financials are a strong argument for companies to favour a BBB+ or A- rating, in our opinion.

More By This Author:

Asia Week Ahead: Central Bank Developments And An Incoming Data FloodThe Fed’s Set For A 25bp Cut, But It’s A Close Call

Poland’s Current Account Balance Significantly Worsens In July

Comments

Log in or sign up to join the conversation.