Tokyo CPI inflation rose 3.5% YoY in April (vs 2.9% in March, 3.3% market consensus)

Tokyo inflation increased a much hotter-than-expected 3.5% year on year in April as services prices surprised to the upside. Markets had expected a significant pick-up partly due to increases in education fee waiver programs relative to a low base from last year. Education prices rebounded to 1.6% YoY from -9.3% in March. But inflationary pressures were broader than expected.

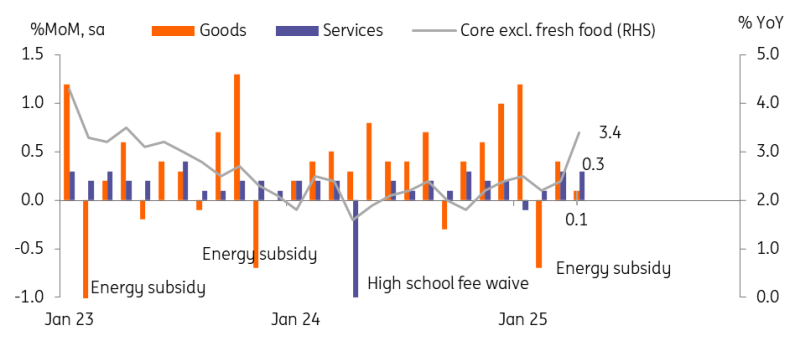

Fresh food prices eased significantly to 4.1% from 13.2% in March, thanks to government support programmes. But prices increased broadly in other sectors. Thus, core inflation, excluding fresh food prices, jumped to 3.4% in April (vs 2.4% in March, 3.2% market consensus). Notably, entertainment and housing prices rose firmly by 2.8% and 1.5%, respectively. In terms of monthly comparison, inflation growth accelerated to 0.5% month on month, seasonally adjusted, from 0.4% in March. Services rose for a third month in a row, up 0.3% in April. Goods prices rose 0.1% following a 0.4% gain in March.

April is when companies raise product prices, and this year's increases were higher than expected. We interpret this price-setting behaviour as firms clearly moving to pass on input cost increases to consumers. With solid wage growth expected this year, it appears that the sustainable inflation the Bank of Japan hoped for has finally arrived. Thus, the accelerated rate of increase has us expecting that the BoJ will continue raising interest rates.

Service prices rose firmly for the past three months

Source: CEIC

BoJ is expected to stand pat next week, but likely to signal additional rate hikes coming

Given the high level of uncertainty surrounding US trade policy, the BoJ is likely to keep its policy rate on hold at next week’s meeting. But with inflation set to remain high in the coming months, the BoJ will resume its rate hikes in the summer. During US-Japan bilateral talks, discussions of the yen have been muted. Yet this doesn't mean the US won't target the weak JPY during the next round of negotiations. We believe that the BoJ will tighten when things become clearer, which will see the JPY appreciating further. This seems a better way to respond to US criticism of the weak JPY, rather than Japan directly intervening in the foreign-exchange market. Uncertainty over US tariff measures complicates the BoJ’s rate hike cycle. We’ve pencilled in a hike in July, but the possibility of a June hike is increasing.

More By This Author:

South Korea GDP Contracts More Than Expected, Increasing Odds Of Recession And Rate CutsMood In Czech Industry Turns Gloomy

FX Daily: Revenant Dollar Needs Constant Flow Of Good News

Comments

Log in or sign up to join the conversation.