S&P futures and European stocks rebounded from Friday’s selloff while Asian shares fell, as investors took comfort in reports from South Africa which said initial data doesn’t show a surge of hospitalizations as a result of the omicron variant, a view repeated by Anthony Fauci on Sunday. Meanwhile, fears about a tighter Fed were put on the backburner.

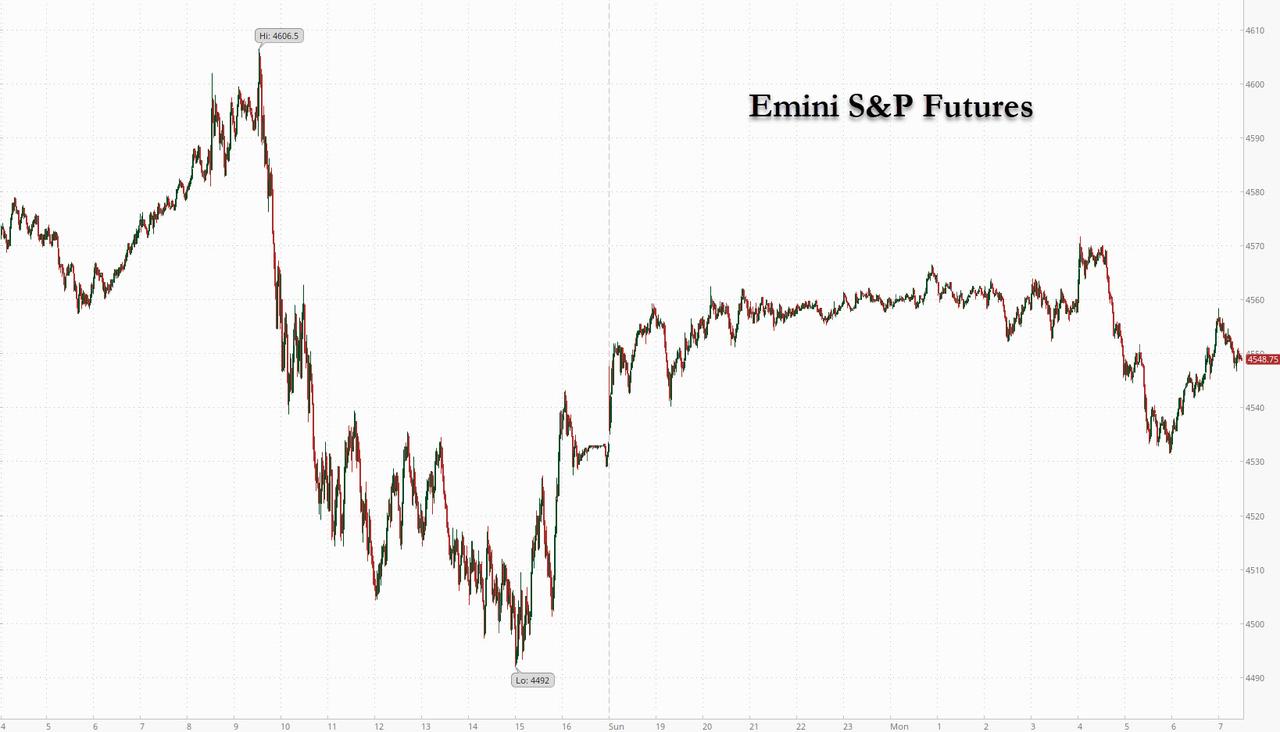

Also overnight, China’s central bank announced it will cut the RRR by 50bps releasing 1.2tn CNY in liquidity, a move that had been widely expected. The cut comes as insolvent Chinese property developer Evergrande (EGRNY) was said to be planning to include all its offshore public bonds and private debt obligations in a restructuring plan. US equity futures rose 0.3%, fading earlier gains, and were last trading at 4,550. Nasdaq futures pared losses early in the U.S. morning, trading down 0.4%. Oil rose after Saudi Arabia boosted the prices of its crude, signaling confidence in the demand outlook, which helped lift European energy shares (OIL). The 10-year Treasury yield (SPTL) advanced to 1.40%, while the dollar was little changed and the yen weakened.

“A wind of relief may blow the current risk-off trading stance away this week,” said Pierre Veyret, a technical analyst at U.K. brokerage ActivTrades. “Concerns related to the omicron variant may ease after South African experts didn’t register any surge in deaths or hospitalization.”

As Bloromberg notes, the mood across markets was calmer on Monday after last week’s big swings in technology companies and a crash in Bitcoin over the weekend. Investors pointed to good news from South Africa that showed hospitals haven’t been overwhelmed by the latest wave of COVID cases. Initial data from South Africa are “a bit encouraging regarding the severity,” Anthony Fauci, U.S. President Joe Biden’s chief medical adviser, said on Sunday. At the same time, he cautioned that it’s too early to be definitive.

Here are some of the biggest U.S. movers today:

- Alibaba’s (BABA) U.S.-listed shares rise 1.9% in premarket after a 8.2% drop Friday prompted by the delisting plans of Didi Global. Alibaba said earlier it is replacing its CFO and reshuffling the heads of its commerce businesses

- Rivian (RIVN) has the capabilities to compete with Tesla and take a considerable share of the electric vehicle market, Wall Street analysts said as they started coverage with overwhelmingly positive ratings. Shares rose 2.2% initially in U.S. premarket trading, but later wiped out gains to drop 0.9%

- Stocks tied to former President Donald Trump jump in U.S. premarket trading after his media company agreed to a $1 billion investment from a SPAC

- Cryptocurrency-exposed stocks tumble amid volatile trading in Bitcoin (BITCOMP), another indication of the risk aversion sweeping across financial markets

- Laureate Education (LAUR) approved the payment of a special cash distribution of $0.58 per share. Shares rose 2.8% in post-market Friday

- AbCellera Biologics (ABCL) gained 6.2% post-market Friday after the company confirmed that its Lilly-partnered monoclonal antibody bamlanivimab, together with etesevimab, received an expanded emergency use authorization from the FDA as the first antibody therapy in COVID-19 patients under 12

European equities drifted lower after a firm open. Euro Stoxx 50 faded initial gains of as much as 0.9% to trade up 0.3%. Other cash indexes follow suit, but nonetheless remain in the green. FTSE MIB sees the largest drop from session highs. Oil & gas is the strongest sector, underpinned after Saudi Arabia raised the prices of its crude. Tech, autos and financial services lag. Companies that benefited from increased demand during pandemic-related lockdowns are underperforming in Europe on Monday as investors assess whether the omicron COVID variant will force governments into further social restrictions. Firms in focus include meal-kit firm HelloFresh (-2.3%) and online food delivery platforms Delivery Hero (-5.4%), Just Eat Takeaway (-5.6%) and Deliveroo (-8.5%). Remote access software firm TeamViewer (-3.7%) and Swedish mobile messaging company Sinch (-3.0%), gaming firm Evolution (-4.2%). Online pharmacies Zur Rose (-5.1%), Shop Apotheke (-3.5%). Online grocer Ocado (-2.2%), online apparel retailer Zalando (-1.5%).

In Asia, the losses were more severe as investors remained wary over the outlook for U.S. monetary policy and the spread of the omicron variant. The Hang Seng Tech Index closed at the lowest level since its inception. SoftBank Group Corp. fell as much as 9% in Tokyo trading as the value of its portfolio came under more pressure. The MSCI Asia Pacific Index slid as much as 0.9%, hovering above its lowest finish in about a year. Consumer discretionary firms and software technology names contributed the most to the decline, while the financial sector outperformed. Hong Kong’s equity benchmark was among the region’s worst performers amid the selloff in tech shares. The market also slumped after the omicron variant spread among two fully vaccinated travelers across the hallway of a quarantine hotel in the city, unnerving health authorities.

“People are waiting for new information on the omicron variant,” said Masahiro Ichikawa, chief market strategist at Sumitomo Mitsui DS Asset Management in Tokyo. “We’re at a point where it’s difficult to buy stocks.” Separately, China’s central bank announced after the country’s stock markets closed that it will cut the amount of cash most banks must keep in reserve from Dec. 15, providing a liquidity boost to economic growth. Futures on the Nasdaq 100 gained further in Asia late trading. The underlying gauge slumped 1.7% on Friday, after data showed U.S. job growth had its smallest gain this year and the unemployment rate fell more than forecast. Investors seem to be focusing more on the improved jobless rate, as it could back the case for an acceleration in tapering, Ichikawa said.

Asian equities have been trending lower since mid-November amid a selloff in Chinese technology giants, concern over U.S. monetary policy and the spread of omicron. The risk-off sentiment pushed shares to a one-year low last week.

Overnight, the PBoC cut the RRR by 50bps (as expected) effective 15th Dec; will release CNY 1.2tln in liquidity; RRR cut to guide banks for SMEs and will use part of funds from RRR cut to repay MLF. Will not resort to flood-like stimulus; will reduce capital costs for financial institutions by around CNY 15bln per annum. The news follows earlier reports via China Securities Daily which noted that China could reduce RRR as soon as this month, citing a brokerage firm. However, a separate Chinese press report noted that recent remarks by Chinese Premier Li on the reverse repo rate doesn't mean that there will be a policy change and an Economics Daily commentary piece suggested that views of monetary policy moves are too simplistic and could lead to misunderstandings after speculation was stoked for a RRR cut from last week's comments by Premier Li.

Elsewhere, Indian stocks plunged in line with peers across Asia as investors remained uncertain about the emerging risks from the omicron variant in a busy week of monetary policy meetings. The S&P BSE Sensex slipped 1.7% to 56,747.14, in Mumbai, dropping to its lowest level in over three months, with all 30 shares ending lower. The NSE Nifty 50 Index also declined by a similar magnitude. Infosys Ltd. was the biggest drag on both indexes and declined 2.3%. All 19 sub-indexes compiled by BSE Ltd. declined, led by a measure of software exporters. “If not for the new omicron variant, economic recovery was on a very strong footing,” Mohit Nigam, head of portfolio management services at Hem Securities Ltd. said in a note. “But if this virus quickly spreads in India, then we might experience some volatility for the coming few weeks unless development is seen on the vaccine side.” Major countries worldwide have detected omicron cases, even as the severity of the variant still remains unclear. Reserve Bank of Australia is scheduled to announce its rate decision on Tuesday, while the Indian central bank will release it on Dec. 8. the hawkish comments by U.S. Fed chair Jerome Powell on tackling rising inflation also weighed on the market

Japanese equities declined, following U.S. peers lower, as investors considered prospects for inflation, the Federal Reserve’s hawkish tilt and the omicron virus strain. Telecommunications and services providers were the biggest drags on the Topix, which fell 0.5%. SoftBank Group and Daiichi Sankyo were the largest contributors to a 0.4% loss in the Nikkei 225. The Mothers index slid 3.8% amid the broader decline in growth stocks. A sharp selloff in large technology names dragged U.S. stocks lower Friday. U.S. job growth registered its smallest gain this year in November while the unemployment rate fell by more than forecast to 4.2%. There were some good aspects in the U.S. jobs data, said Shoji Hirakawa, chief global strategist at Tokai Tokyo Research Institute. “We’re in this contradictory situation where there’s concern over an early rate hike given the economic recovery, while at the same time there’s worry over how the omicron variant may slow the current recovery.”

Australian stocks ended flat as staples jumped. The S&P/ASX 200 index closed little changed at 7,245.10, swinging between gains and losses during the session as consumer staples rose and tech stocks fell. Metcash was the top performer after saying its 1H underlying profit grew 13% y/y. Nearmap was among the worst performers after S&P Dow Jones Indices said the stock will be removed from the benchmark as a result of its quarterly review. In New Zealand, the S&P/NZX 50 index fell 0.6% to 12,597.81.

In FX, the Bloomberg Dollar Spot Index gave up a modest advance as the European session got underway; the greenback traded mixed versus its Group-of-10 peers with commodity currencies among the leaders and havens among the laggards. JPY and CHF are the weakest in G-10, SEK outperforms after hawkish comments in the Riksbank’s minutes. USD/CNH drifts back to flat after a fairly well telegraphed RRR cut materialized early in the London session. The euro fell to a day low of $1.1275 before paring. The pound strengthened against the euro and dollar, following stocks higher. Bank of England deputy governor Ben Broadbent due to speak. Market participants will be watching for his take on the impact of the omicron variant following the cautious tone of Michael Saunders’ speech on Friday.

Treasury yields gapped higher at the start of the day and futures remain near lows into early U.S. session, leaving yields cheaper by 4bp to 5bp across the curve. Treasury 10-year yields around 1.395%, cheaper by 5bp vs. Friday’s close while the 2s10s curve steepens almost 2bps with front-end slightly outperforming; bunds trade 4bp richer vs. Treasuries in 10-year sector. November's mixed U.S. jobs report did little to shake market expectations of more aggressive tightening by the Federal Reserve. Italian bonds outperformed euro-area peers after Fitch upgraded the sovereign by one notch to BBB, maintaining a stable outlook.

In commodities, crude futures drift around best levels during London hours. WTI rises over 1.5%, trading either side of $68; Brent stalls near $72. Spot gold trends lower in quiet trade, near $1,780/oz. Base metals are mixed: LME copper outperforms, holding in the green with lead; nickel and aluminum drop more than 1%.

There is nothing on today's economic calendar. Focus this week includes U.S. auctions and CPI data, while Fed speakers enter blackout ahead of next week’s FOMC.

Market Snapshot

- S&P 500 futures up 0.7% to 4,567.50

- STOXX Europe 600 up 0.8% to 466.39

- MXAP down 0.9% to 189.95

- MXAPJ down 1.0% to 617.01

- Nikkei down 0.4% to 27,927.37

- Topix down 0.5% to 1,947.54

- Hang Seng Index down 1.8% to 23,349.38

- Shanghai Composite down 0.5% to 3,589.31

- Sensex down 1.5% to 56,835.37

- Australia S&P/ASX 200 little changed at 7,245.07

- Kospi up 0.2% to 2,973.25

- Brent Futures up 2.9% to $71.89/bbl

- Gold spot down 0.2% to $1,780.09

- U.S. Dollar Index up 0.15% to 96.26

- German 10Y yield little changed at -0.37%

- Euro down 0.2% to $1.1290

Comments

Log in or sign up to join the conversation.