Image Source: Pexels

London's FTSE 100 rebounded on Wednesday, bolstered by gains in energy stocks and positive corporate updates, as investors awaited the U.S. Federal Reserve's interest rate decision. The blue-chip FTSE 100 index rose 0.9%, rebounding from its worst day in a week on Tuesday. The mid-cap FTSE 250 index increased. Both indexes are on track for monthly gains, with the FTSE 250 aiming for its best performance this year. Investors are now focused on the Fed's monetary policy decision later in the day, which could influence the global outlook on rate cuts. While the Fed is widely expected to hold rates steady, markets are anticipating hints of a potential rate cut in September, following recent data indicating cooling inflation.

InterContinental Hotels Group, the owner of Holiday Inn, saw its shares drop 3.4% to 7,802 pence, making it the biggest loser on the FTSE 100 index, after rival Marriott lowered its full-year forecast for room revenue growth, citing a weaker operating environment in China and expectations of softer demand in North America. Bernstein analyst Richard Clarke commented that "hotels are not immune to the consumer slowdown in China".

HSBC's London-listed shares rise up to 4.25% to 705.7p as the bank announces a $3 billion share buyback and sets a new mid-teens return on average tangible equity target for 2025, after reporting stable first-half profit and narrowing losses in Chinese real estate. The stock is among the top percentage gainers on the FTSE 100 index, which is up 1.4%. HSBC will also pay an interim dividend of 10 cents per share, following 31 cents announced last quarter.

Shares of GSK declined by 2.6% to 1,502 pence, being the top loser on the FTSE 100 index. The drop was attributed to a 9% miss in vaccine sales, primarily due to weaker demand for Shingrix in the U.S., including destocking and lower sales outside the U.S. GSK has adjusted its vaccine sales growth outlook to a low to mid-single-digit percentage, down from the previous expectation of high single-digit to low double-digit percentage growth. However, the company raised its full-year profit and revenue outlook. GSK reported Q2 adjusted earnings of 43.4p per share on sales of £7.88 billion ($10.11 billion), exceeding the consensus. Despite the losses today, the stock is up 3.6% year-to-date.

Energy shares led the broader gains with a 1.8% rise as the index rebounded from Tuesday's losses. Major players like BP and Shell saw increases of more than 1.4% each, following the killing of Hamas' leader, which heightened tensions in the Middle East and pushed oil prices up by more than $1 per barrel.

The Bank of England is expected to announce its decision on Thursday, with markets anticipating a more than 58% chance of a rate cut, which would be the central bank's first since 2020. Additionally, a crucial U.S. jobs report and more quarterly earnings from major U.S. tech companies are on the radar.

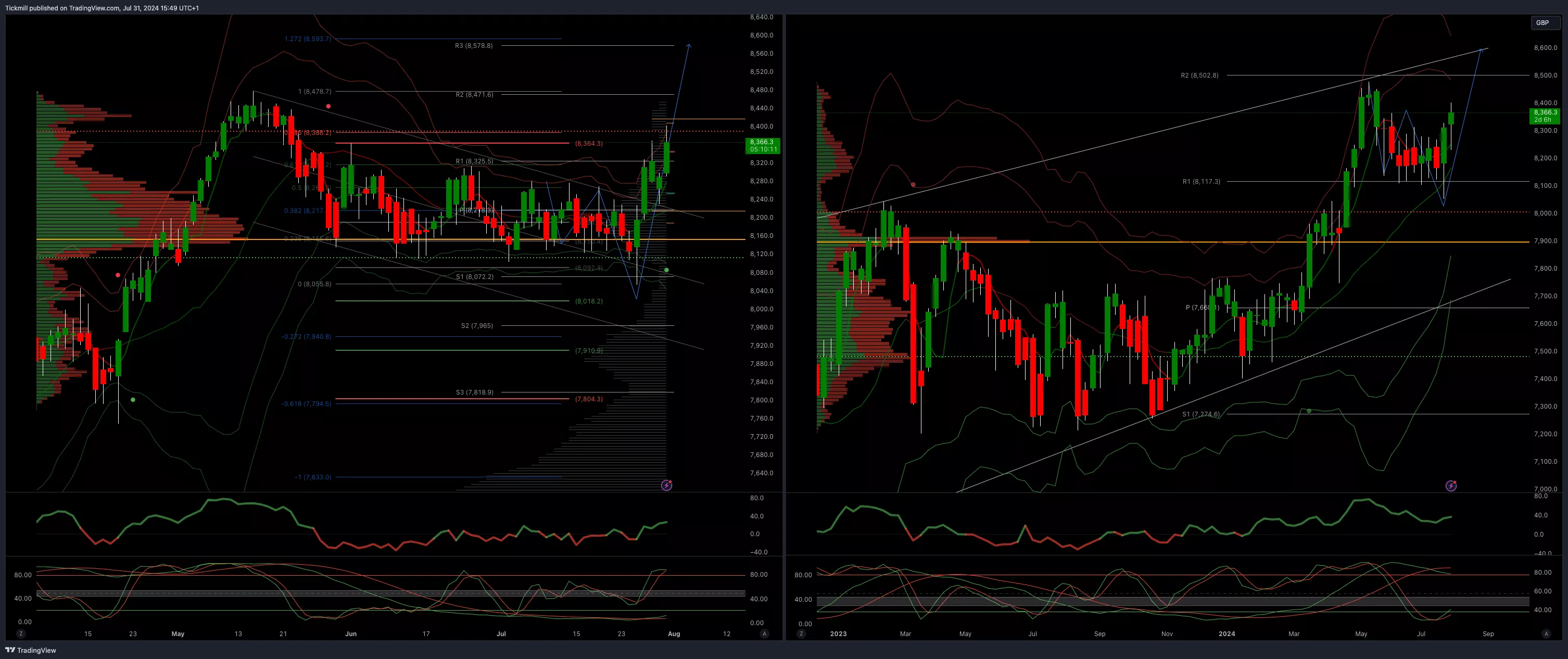

Technical & Trade View

FTSE Bias: Bullish Above Bearish below 8225

- Primary support 8000

- Primary objective 8593

- DailyVWAP Bullish

- Weekly VWAP bullish

(Click on image to enlarge)

More By This Author:

Daily Market Outlook - Wednesday, July 31SP500 Daily Trade Plan - Wednesday, July 31

FTSE Sentiment Remains Subdued Ahead Of Central Bank Meetings

Comments

Log in or sign up to join the conversation.