Image Source: Pexels

The 💣 Heard Around The World

The market staged a full-throttle risk-on revival, launching global equities into the stratosphere as oil prices cratered and rate-cut bets gained momentum. With the Middle East truce—however duct-taped and temperamental—holding long enough to calm headlines, traders pulled the ripcord on the fear trade and dove headfirst into equities. Trump’s “F-Bomb” scolding of Israel and Iran added ice water to the fire—or at least enough jawbone to muzzle the Middle East combatants for now.

Stocks didn’t just rally—they revelled. The MSCI World Index notched fresh highs, emerging markets flexed like it was 2021, and Wall Street's big tech darlings surged within spitting distance of all-time peaks.

Oil, meanwhile, did a spectacular swan dive. Brent’s 18% round-trip from post-strike highs felt less like price discovery and more like panic air being let out of a geopolitical balloon that never quite lifted off. From a $90 war-premium mirage to $64 reality check, crude got clubbed like it was caught front-running false intel.

The market’s shrug at surging oil prices was a reality check: crude may no longer be the puppet master of macro it once was—Big Tech and GenAI now hold the reins—but it's still the lit match in the inflation tinderbox. A 20% year-on-year plunge in oil isn’t just headline candy—it’s rate-cut bait. And for Powell, whose policy playbook hinges on whether tariffs stoke inflation, collapsing crude oil prices give him the perfect alibi to start aligning with the doves. At the same time, market rate cut expectations do the heavy lifting regardless.

The Fed chair played his hand with careful ambiguity. “We’re not in a rush,” he told lawmakers—but no more hawkish than last week without opening the rate cut floodgates. The market heard what it wanted. Treasury yields slipped, the dollar took a breather, and swap traders edged closer to pricing in two cuts by year-end. Powell didn’t endorse a July cut, but he didn’t close the door either. His tone didn’t quite echo Vice Chair Bowman’s recent shift, but it was less hawkish enough for markets to triangulate between “wait-and-see” and “If it turns out that inflation pressures do remain contained, then we will get to a place where we cut rates, sooner rather than later.”

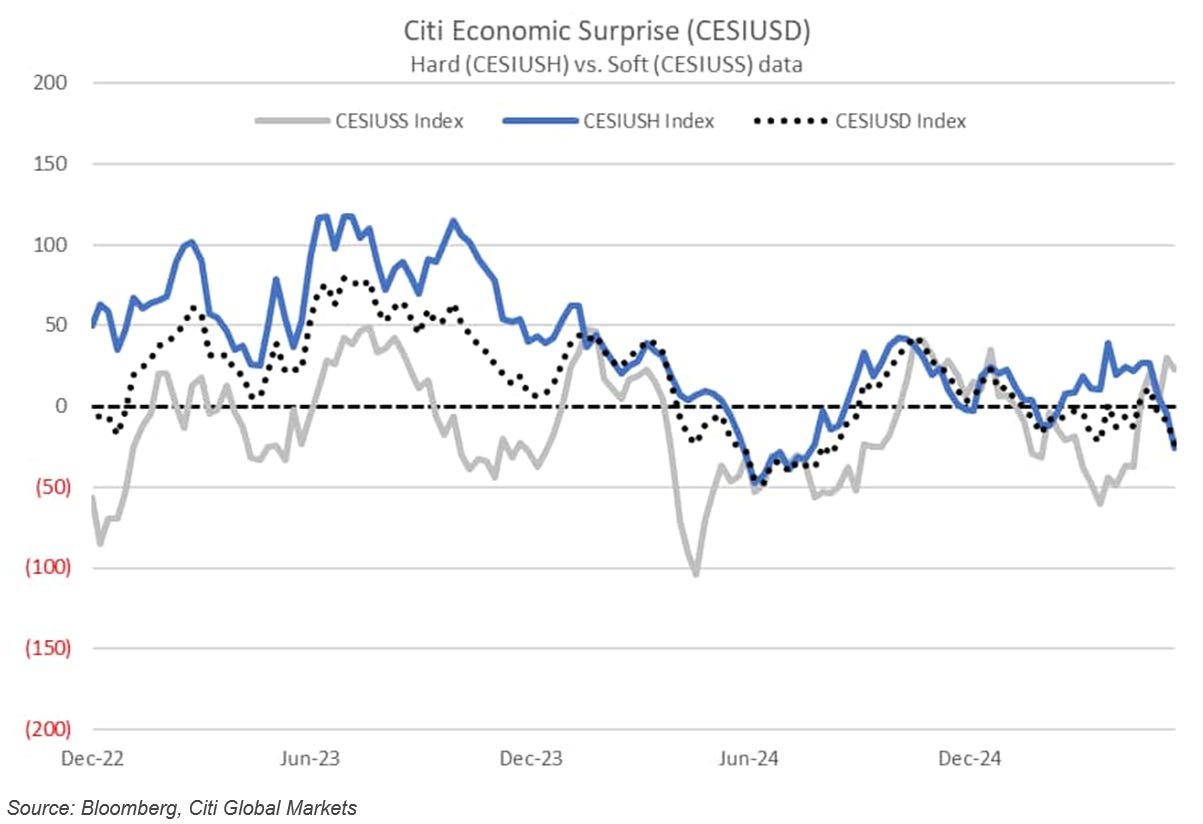

Under the hood, U.S. data’s been losing altitude. Citi’s economic surprise index dipped below zero—signals are flashing amber even as the AI-fueled Nasdaq blitzes past resistance like it’s late to a chip conference. Consumer confidence is waning, job sentiment has hit a four-year low, and the current account deficit has expanded to a record $450 billion. Beneath the AI euphoria lies a macro soft patch, and Powell knows it.

What’s more, the Fed’s own unity is fracturing. While Powell preaches patience, Waller and Bowman are increasingly comfortable flirting with a July pivot. Kashkari and Barr, meanwhile, want more clarity on tariffs before they move. The tug-of-war within the Fed is mirrored in the market’s own split-brain—half chasing the melt-up, half hedging for the tariff fallout.

And yet, equities are partying like the worst is behind us. Volatility’s collapsed, correlations are breaking down, and traders are treating geopolitical risk like just another dip to buy. The Trump-brokered truce may be wobbly, but if it holds—or even just doesn’t fall apart in public—it clears a huge tail risk off the board. That gives AI-mania a free rein to drive the tape.

The market has switched its lenses—from crisis to opportunity, from war risk to rate relief. The question isn’t whether Powell will cut—it’s when, and whether he’ll be dragged there by data or delivered by falling oil, fading confidence, and election-year pressure. For now, the bulls are back in charge, oil’s in a free fall, and Powell’s steady hand—however calculated—is giving this rally legs.

The View

Ceasefire Sparks Melt-Up: Tech Soars, Oil Craters, Powell Grilled While Gamma Runs Wild

What a difference a détente makes. With Iran and Israel apparently shelving their war games (for now), markets hit the afterburners—sending the Nasdaq 100 to a fresh record close, the S&P ripping through 6100, and Bitcoin vaulting higher as geopolitical risk premia got yanked like a rug. Meanwhile, gold and crude both got torched, giving back every ounce of conflict bid and then some. War off, risk on.

The VIX was mugged back to 17, erasing the entire Middle East panic premium, while Treasuries caught a safe-haven bid not out of fear, but because both soft and hard U.S. data are now rolling over in sync. With growth fading and inflation momentum stalling, rate-cut pricing has gone full steam ahead—July’s back in play, September looks baked in, and the dollar is headed south like it’s allergic to Powell’s ambiguity.

And then there’s the Nasdaq. Up 35% from the April lows, it just printed a golden cross for the first time since AI replaced earnings as the primary investment thesis. Every squeezable corner of the market caught fire—non-profitable tech, meme stocks, high-shorted trash, and the Bitcoin-sensitive basket all caught serious upside gamma. Retail's still here, just not in the places CNBC watches.

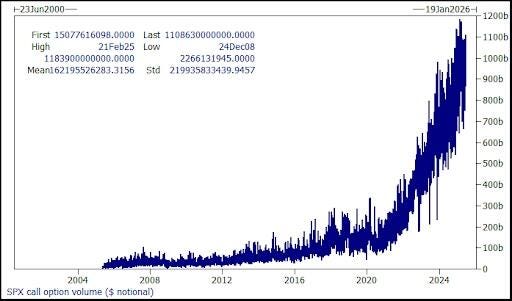

SPX call volumes went vertical—over $1.1 trillion notional traded yesterday alone. Dealers are short gamma, vol-control funds are gearing up to deploy $100 billion in mechanical flows, and the July seasonals are a tailwind. It’s a melt-up cocktail: positioning light, narratives fragmented, yet price action parabolic. No news is bullish, and even bad news now reads like a trigger for looser policy.

Gold tried to find a floor at $3300 but couldn’t attract real love—why hedge when Powell’s stalling, oil’s down double digits, and nobody’s throwing punches in the Gulf? Crude is now trading below pre-war levels as if the Strait of Hormuz never even made the headlines.

Over on Capitol Hill, Powell faced a verbal shanking from Republicans demanding to know why he isn’t cutting rates now like he did for Biden when the data was stronger and CPI was hotter. The response? A masterclass in nothingness, hidden behind tariff theory and a refusal to admit the Fed missed both the transitory call and the political optics.

So now we sit in a feedback loop of lower oil, softer data, easing geopolitical heat, and Powell playing for time—all while stocks float higher on a river of AI euphoria and gamma-fueled momentum. The bears? Pinned under a trillion dollars of call buying.

Welcome to the market’s new default setting.

So why isn’t Powell signing off on a July cut?

Powell’s still playing hostage to the ivory tower crowd that swears tariffs are inflationary death bombs—but said nothing when Biden’s spending spree lit CPI on fire. Remember when “transitory” was the intellectual safe word? Now that inflation is rolling over and crude has been clubbed, rate cuts somehow still require a séance.

Independent? Sure. (sarcastic)

Data-dependent? Only on alternate Tuesdays.

Awkward? Painfully.

As for Tariff Inflation?

The Producer Price Index tracks what producers take home, not just what consumers pay. For wholesalers and retailers, who don’t transform the product, the PPI doesn’t capture end-product prices—it tracks margin moves. Think: it’s not the sticker price, it’s the spread between what they buy and what they sell.

When tariffs hit imports, they jack up acquisition costs. If sellers can’t pass that cost on, margins get squeezed. That shows up in the PPI as a dip in trade service prices. But here’s the kicker: apparel retail trade margins haven’t budged much this year. Translation? They’re either hiking prices behind the scenes or cutting other costs to offset the tariff drag.

Bottom line: Tariffs are margin killers unless retailers pass the costs on to consumers. In this case, someone is eating the cost—and it’s not showing up in PPI, at least not yet, or likely never, since retail was the biggest price gouger during the Covid pandemic. I doubt they want to get caught with their hand in the consumer's pocket again.

More By This Author:

The Lodestar Flinched: Oil’s Panic Pump Ends In A Risk-On Reversal

Havens Light Up, Crude Pops, But Panic Button Stays Untouched

Week Ahead: On A High Wire In A Desert Sandstorm — Markets Brace For The Next Gulf Move

Comments

Log in or sign up to join the conversation.