We expect an 8-1 vote in favor of another rate cut next Thursday, though we doubt the Bank will drop too many hints on what comes next. We're looking for three further cuts later this year, but a shaky jobs market and the prospect of lower services inflation may risk pushing the BoE into a more aggressive stance.

Image Source: Pixabay

Four 2025 Rate Cuts is the Path of Least Resistance

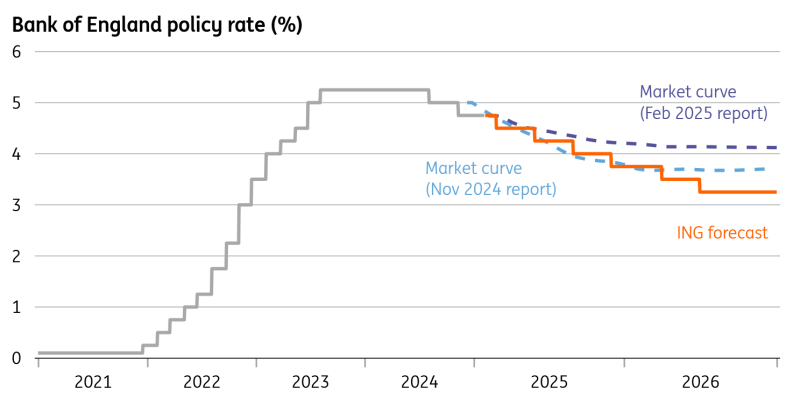

Slowly but surely, financial markets are coming around to the idea of four rate cuts from the Bank of England this year. Policymakers are poised to take rates lower by 25 basis points at its meeting on Feb. 6. And though they’ve not quite said so, it’s heavily implied that the Bank expects once-per-quarter cuts for the rest of this year. That's our base case, and markets are now pricing 78 bp of easing by year-end, up from just 29 bp in mid-January.

February’s meeting is unlikely to rock the boat too much. Though, if anything, we think the risk lies in a more dovish reaction in financial markets. Here’s what we expect.

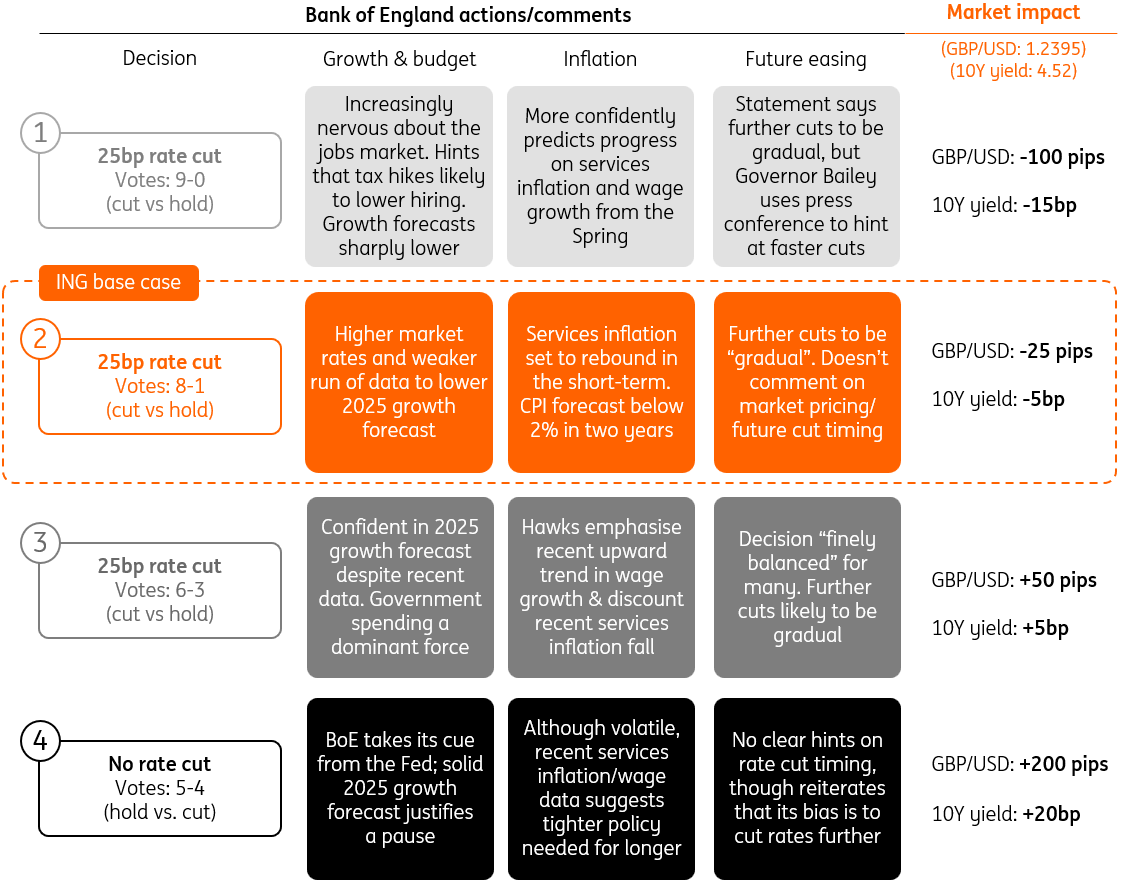

Four Bank of England Scenarios for February's Meeting

(Click on image to enlarge)

Source: ING

Vote Split – Watch Out for Catherine Mann

We expect a 8-1 vote in favor of that 25 bp cut, with arch-hawk Catherine Mann once again dissenting. She has yet to vote for a rate cut and had consistently voted for further hikes, long after the Bank’s tightening cycle had ended.

None of that would be remotely surprising, but if we’re going to get a dovish surprise, then this is where it’s going to come from. Remember at December’s meeting, three committee members voted for a cut, which – while still a minority – was more than many had expected. And the real surprise next week would be if Mann finally throws in the towel and votes for a cut. That feels unlikely, but it would be the single most dovish thing that realistically could happen at February’s meeting.

Could we see at least one official voting for a more aggressive 50 bp cut? Again, possible, but unlikely. The most likely candidate would be Swati Dhingra, who lies at the opposite extreme to Mann. Were she to be a lone voice calling for faster easing, we suspect investors would conclude there’s little read-across to what other committee members might do at future meetings.

The BoE's Data Dashboard

(Click on image to enlarge)

Source: ING

Forecasts Set For Downward Revisions

We’ll get new growth and inflation forecasts this time, and the overall theme is likely to be dovish. Growth is set to be revised down, in part because the recent data has been lackluster. Fourth-quarter GDP will probably be flat where the BoE had previously penciled in 0.3%. That lowers the starting point for 2025 annual growth.

On top of that, market interest rates, which these forecasts are based upon, are up by roughly 50 bp across the curve since November. Higher expected borrowing costs means weaker activity. Where the Bank previously had 2025 growth at 1.5%, it could be revised down to around 1%.

While that’s not hugely important for markets, it would shine a light on the Office for Budget Responsibility, the body that polices the government’s fiscal policy. At the time of the October budget, it expected growth of 2% this year, which looked optimistic at the time and has only grown more so since.

That will inevitably get revised down in the Spring Statement on March 26. If this is also the case for future years, that’s more bad news for the chancellor. Her fiscal “headroom” – the margin of error around the fiscal rules – has already been eradicated by the recent bond sell-off.

Markets are Expecting Higher BoE Rates, Relative to November

(Click on image to enlarge)

Market curves based on a 15-day average ahead of each BoE meeting, which is the methodology used for the official forecasts. Source: Macrobond, ING

Back to the BoE, the news is more mixed on inflation. Headline inflation is likely to be a little higher than expected in November, and it could touch 3% (2.5% now) later this year. That’s mainly down to energy, though. And just as with growth, higher market rates will mechanically lower inflation further out.

The key number, as always, is where inflation is seen in two years’ time, the horizon over which monetary policy has its biggest impact. It’s likely to be at or below 2%, having been seen a tad above back in November. In theory, that tells us the Bank thinks rate expectations are a little too high to deliver inflation at target. In practice, the BoE has downplayed these forecasts as a signal about its future intentions.

Further Gradual Cuts to Come

Much like the Federal Reserve and European Central bank, the BoE is unlikely to be drawn much on what it’ll do next. Expect its policy statement to simply reiterate that further gradual easing is likely, without any comments about timing. Four rate cuts this year feels like the Bank’s base case, and that's our thinking, too.

But don’t ignore the risk of more aggressive easing later this year. Markets have a tendency of lumping the BoE in the same category as the Fed, despite the macro story looking increasingly different in the UK.

Services inflation, the most critical indicator for the BoE, fell sharply in December. That may be a temporary blip – and it’ll likely bounce to 5% in January – but the trend is undoubtedly down. We expect it to slip below 4% in the second quarter, and the progress is likely to look even better when volatile/less relevant categories are excluded.

The jobs market is looking shaky, too. Employment in the private-sector, judging from payroll data, fell gradually in 2024. Vacancies are well down. Wage growth has been proving sticky, but surveys suggest that will gradually change as the year goes on.

Faster cuts aren’t our base case, but they remain more likely than a Fed-style pause later this year.

Shorter-Dated Gilts Could Benefit from Dovish BoE

Gilt yields eased lower from their peak in early January, where the 10-year yield fell from 4.8% to 4.5% currently. Markets remain more skeptical about the BoE’s ability to ease, especially against a backdrop of increased government spending. Having said that, most of the recent gilt yield dynamics were actually dictated by US rate developments.

And similarly to what we see for euro rates, we expect shorter-dated bond yields – e.g., gilts with a two-year maturity – to start moving more independently from US influences. As such, the two-year gilt yield might find itself significantly lower on a more dovish BoE, while the 10-year gilt is kept more anchored at elevated by levels by high 10-year UST yields.

Sterling May Start to Hand Back Recent Gains

The pound made a mini-recovery from its gilt-led sell-off in mid-January. The global bond market rally has helped – as has the introduction of the BoE’s new gilt-crisis liquidity facility, the CNRF. But we doubt sterling has to rally too much further.

We say this because the prospect of UK fiscal consolidation in March should be pushing on the open door of an under-priced BoE easing cycle. This is a bearish combination for sterling.

In terms of the impact of Thursday’s BoE rate decision on sterling, the FX market is very relaxed. The FX options market only priced in an expected 40 US dollar pip trading range for the one-day straddle options structure.

Additionally, the relationship between rate differentials and the GBP/USD pair is far less pronounced ever since the Trump trade dominated market thinking from last October. Before then, an independent 10 bp move in 10-year gilt yields was worth around 120 pips in the GBP/USD pair. The risk premium around tariffs is clearly impacting the GBP/USD currency pair now, as it is for Forex markets in general.

Nonetheless, potential downside risks to sterling are evident in the vote split, or the growth forecast downgrade and what it means for the fiscal position. And through the second quarter, we think the GBP/USD pair will be trading closer to 1.20 and the EUR/GBP currency cross to 0.85.

More By This Author:

President Trump Set To Push Ahead With Tariffs Despite The Risks For The U.S. EconomyUS Inflation Cools Amid Tariff Uncertainty

German January Inflation Brings Some Relief For The ECB

Comments

Log in or sign up to join the conversation.