Looking at all the evidence available so far, it looks like the eurozone fell into a shallow recession in the third quarter. For the European Central Bank, this is unlikely to be enough to prompt an immediate dovish pivot given its determination to hike interest rates in the face of double-digit inflation. We still expect another 75bp hike in October.

A recession in the eurozone has now become the near-consensus view, with the IMF being the latest international institution to predict a contraction in the eurozone economy in 2023. The only question seems to be how severe this winter recession will be and when it will start. We take a look at whether the economy actually started to shrink in the third quarter.

Soft data suggests that a recession is likely to have started

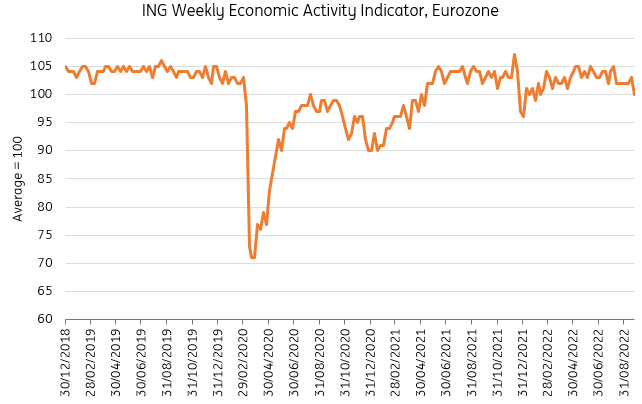

During the pandemic, we developed a nowcast indicator that gave us insight into how the eurozone economy was performing during lockdowns. While it was designed to perform well in the specific circumstances of the pandemic, there is merit in looking at it once again. The big caveat is that electricity use is an important driver of the index, which has of course been subject to large productivity gains as the energy crisis has unfolded. Nevertheless, we see that the direction for most underlying variables is slightly negative at the moment, corresponding to a view that the economy fell into a mild contraction at the end of the third quarter.

The Nowcast tracker suggests that activity has been moderately declining recently

Image Source: ING Research

For more on how this index is constructed, read here: https://think.ing.com/articles/introducing-the-ing-weekly-economic-activity-index-for-the-eurozone/

Mobility indicators are an important part of the nowcast index. When the economy reopened earlier in the year, we saw a strong increase. But except for workplace activity, most mobility indicators normalized during the spring and have remained at these levels over the course of the third quarter. Our average of the Google mobility indicators shows that the second quarter still saw large mobility gains, while the third quarter was flat. While seasonal factors may understate the performance in this regard, it does seem fair to assume that most, if not all, of the post-lockdown rebound, is now behind us.

Adding to meager nowcast data, surveys suggest that a recession is likely to have started already. The composite PMI was below 50 – signaling contraction – for all three months of the third quarter. In fact, it gradually worsened as the quarter progressed, with September showing more serious signs of contraction as the summer months ended. Both services and manufacturing activity are now well below 50. This is a broader indicator of activity, which adds to signs that a shallow recession began in 3Q. Still, some evidence from data not collected from surveys would be useful so as not to miss out on positive surprises.

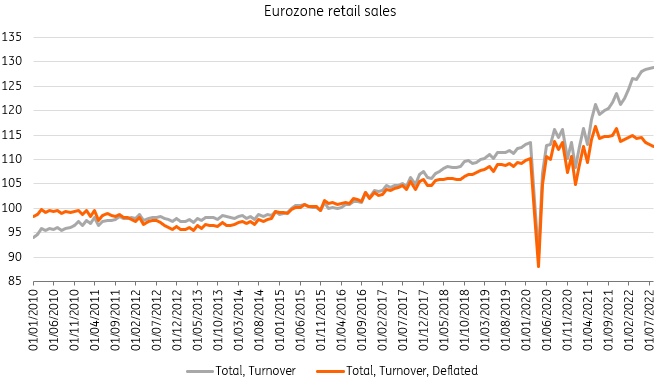

Retail sales are weak and tourism is not expected to make up for it

When looking at consumer spending, we see a clear downward trend in retail sales. November last year was the recent peak in sales activity after which a steady decline set in. This is because of the sharp decline in purchasing power that households have experienced since then, but will also be related to the reopening of certain services. With people returning to restaurants and bars and starting to take holidays again, spending patterns have shifted away from goods. The latter seems to be a smaller part of this though. As chart 2 shows, people are spending more than ever in retail, but volumes are down. So the impact of inflation is that people are forced to spend more and more at the store but take home less for it. Interestingly, car sales have been increasing in August, coming from a very low base.

Consumers pay more in retail, but take home lower volumes than late last year

Image Source: Eurostat, ING Research

The ECB put a lot of emphasis on the positive impact of tourism on third-quarter growth. This is a bit of a blind spot in terms of more frequent data and could indeed add to positive activity this quarter. Looking at overnight stays in the eurozone, we see that July and August were very close to pre-pandemic levels which suggest continued 3Q strength, but businesses are less optimistic. Surveys suggest that the peak in tourism activity was in June and that the summer may have slightly disappointed. Still, tourism is likely to have added positively to the third quarter GDP growth number. All in all, though, it looks like the summer was not strong enough to have kept consumption growth positive overall.

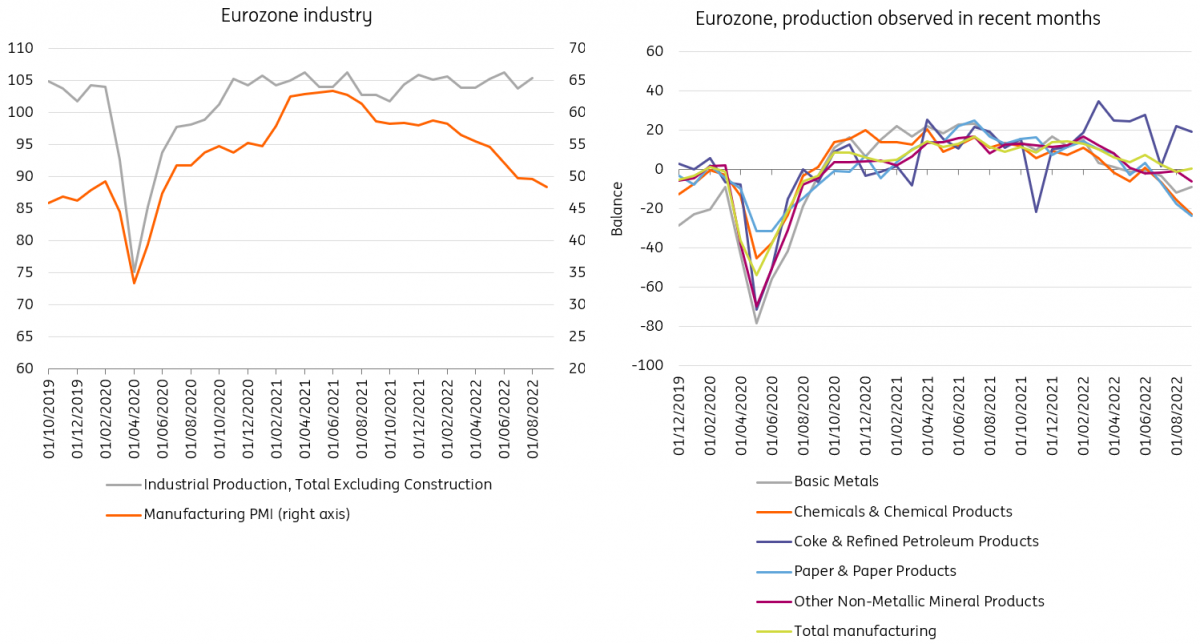

Industry limits losses so far due to improving supply chains, but the trend is down

When looking at the industry, we see a divergence between the survey and hard data so far. While surveys suggest a sizable weakening in activity, August data was better than expected. It seems that the improvement in supply chain problems and the availability of inputs to production are allowing businesses to catch up on backlogs of orders. Still, new orders are falling and survey data suggests a weaker September. Particularly in energy-intensive sectors, the production seems to have dropped again in September. The German statistical office has started to release a new times series for energy-intensive industries, showing that production in these sectors dropped by more than 8% between February and August. If September was indeed weaker than August, industrial production will have been negative on the quarter, adding to expectations that the economy was already in a shallow contraction in 3Q.

Production recovered a bit in August, but energy-intensive sectors look problematic in September

Image Source: Eurostat, Macrobond, European Commission DGECFIN, ING Research

Right chart shows total manufacturing and the most energy-intensive sectors

Interestingly enough, trade is very difficult to judge at the moment. Data on volumes is hard to come by and strongly rising prices for energy have caused nominal imports to soar. It looks like real export growth weakened over the summer, but imports could have fallen even more as energy is such an important component, and energy use is down due to high prices. This means that net exports could have actually contributed positively to GDP growth last quarter. If this makes growth positive, it would mean that a recessionary environment saw positive growth. Just as the US went through a technical recession in the first half of this year when the economy contracted but no real signs of recession were visible, so the eurozone could be in a technical expansion, where the economy expands in a recessionary setting.

Contraction in 3Q, but no smoking gun for a dovish pivot from the ECB

Taking this all together, we find enough weakness in recent data to believe that a recession has already started and stick to our forecast of a -0.2% quarter-on-quarter contraction in 3Q. But shallow negative growth – still held up by temporary recovery factors – is also unlikely to give the ECB the smoking gun for a dovish pivot. In fact, at the next ECB meeting on 27 October, there won’t be any new staff projections, nor will there be hard data for September, allowing the ECB to announce another hike by 75 basis points. It will take until the December meeting before the ECB has a better view of the severity of the recession, which should then be enough to embark on a dovish pivot.

More By This Author:

Can Central Banks Go Bust?Is Quantitative Tightening Really Coming To The Eurozone?

German Economy Weakens In August

Comments

Log in or sign up to join the conversation.