Eurozone Mobility Plateaus: Delta Impact Or Summer Lull?

The rebound in mobility has stagnated in recent weeks. While the Delta variant does seem to have had some impact on future consumer and business expectations, it looks like the recovery in mobility has stalled mainly because of seasonal effects. We therefore still expect GDP growth to remain strong in 3Q, but Delta does signal a risk to the outlook.

The relationship between mobility and economic activity was very strong during the first wave of the coronavirus in spring 2020 but has weakened over time, as businesses have better adapted to the restrictive measures. Still, it does give some indication of how domestic demand is recovering and therefore is worth revisiting now that economies have opened up further, although we’ve also seen a rise in new cases in many eurozone economies driven by the Delta variant.

The recovery in mobility has stalled

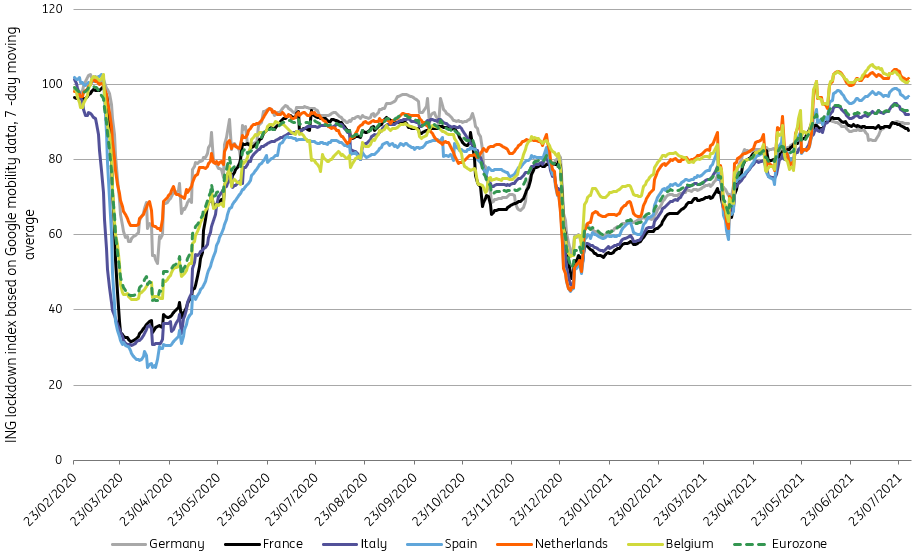

Since early January, mobility in the eurozone has been on the rise, according to our ING mobility index which combines Google mobility data on daily trips to retail & recreation facilities, workplaces and groceries and pharmacies. This has coincided with the economic recovery from the second wave and has brought daily economic movement close to pre-pandemic levels again in June. In recent weeks, the steady rise in eurozone mobility has come to a halt in all eurozone economies.

The rise in mobility has stalled in the major eurozone economies since mid-June

Source: ING Research, Google COVID-19 Community Mobility Reports

Note: index of activity since 15 Feb 2020 for retail & recreation, groceries & pharmacies and workplaces using Google Covid19 Community Mobility Reports with data through 30 July 2021. 100=baseline of activity between 3 Jan and 9 Feb 2020

The plateau in the mobility index comes at a time of another flare up in the virus as the Delta variant is becoming the dominant strain in most eurozone economies. To a limited degree, countries have put more restrictive measures in place again or delayed the easing of measures. Surveys have already shown some impact on confidence for businesses and consumers, with optimism about the months ahead declining. With mobility flattening, it could be that we’re already seeing an impact on behaviour as well.

Delta may have some impact, but seasonal effects are likely to be dominant

The impact of Delta on mobility seems premature though. Last year, there was a seasonal effect on mobility in summer, which roughly started in July. This seems to be in line with developments this year, although mobility this time plateaued two weeks earlier. This implies perhaps some impact from Delta, but to a large degree this will be a seasonal effect. Also, we do see higher levels of mobility this year compared to last. For the eurozone as a whole the difference is not dramatic, at 93 compared to 91 last year, but the Netherlands, Belgium and Spain have seen large improvements. Germany and France lag a bit with mobility readings similar to those of last summer.

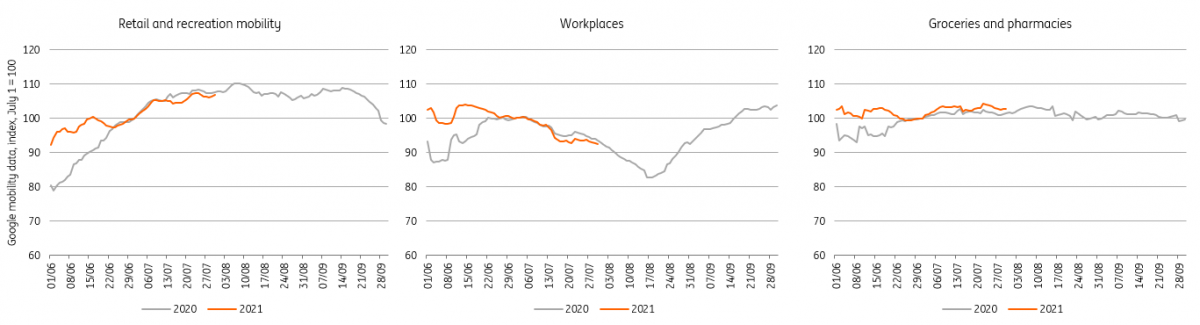

Delving into the numbers a bit, we find that it is mainly the return to work that has yet to recover. Visits to essential shops – grocery stores and pharmacies – have jumped well above pre-crisis levels at this point and retail and recreation visits have also recovered back to pre-pandemic levels. The pattern is very similar to that seen last year though. The fall in workplace visits should be no surprise and if last year can be used as a relevant benchmark, we can expect this to hit bottom in the middle of August. The decline in retail and recreation mobility seen in September was due to the second wave starting, which means that we can count that out as a seasonal pattern.

The stagnation in July follows the same pattern last year, hinting at a dominant seasonal effect

(Click on image to enlarge)

Source: ING Research, Google COVID-19 Community Mobility Reports

Growth is set to be strong for 3Q GDP, but Delta remains a downside risk to the outlook

The rise in mobility has come to a halt for now, but this seems to be more of a summer pause than the end of the economic rebound. With new cases having apparently peaked for now, there should be less concern about a continued economic rebound in the third quarter. Still, last year’s autumn coincided with a second wave and concerns about the Delta variant later in the year remain. As the development of the virus remains hard to predict, we do consider Delta to be a significant downside risk to our outlook for the remainder of the year, but it does seem that the current impact remains moderate.

Disclaimer: This publication has been prepared by the Economic and Financial Analysis Division of ING Bank N.V. (“ING”) solely for information purposes without regard to any ...

more