Net lending to businesses remains weak, but this is largely TLTRO-related, and may improve in the months ahead.

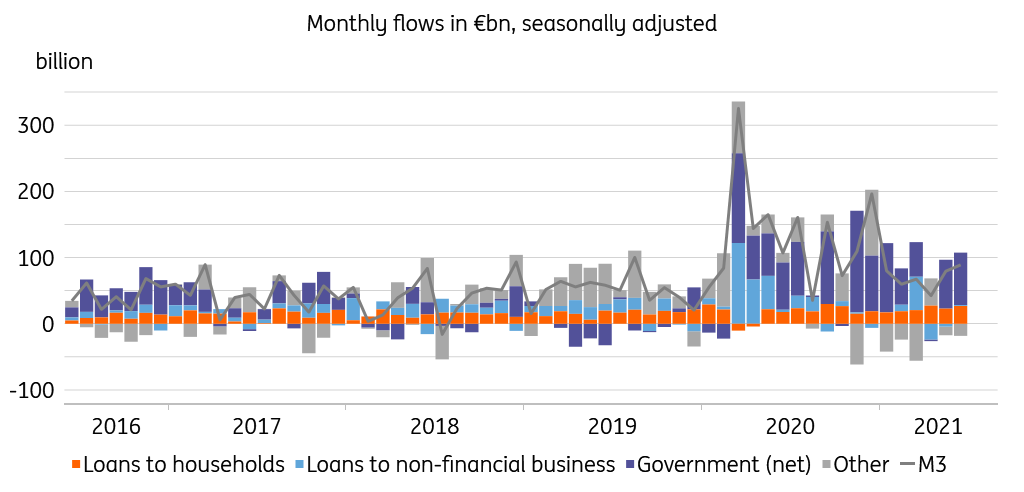

In June, the eurozone M3 money measure increased by €89bn (seasonally adjusted), which is well above the pre-pandemic monthly average, but nothing special since March last year. The main driver continues to be the European Central Bank's asset purchase program, as it has been since March 2020. In net terms, governments (indirectly, as the ECB only buys on secondary markets) borrowed €79bn from the Eurosystem in June, leading to the equivalent sum in money creation.

Drivers of eurozone M3 money growth

Source: ECB, ING-calculations

"Government (net)" is government borrowing from banks (including the Eurosystem) minus government deposits. "Other" includes claims and liabilities outside the Eurozone, longer-term bank liabilities, and loans to non-bank financials.

Turning to bank lending, net bank lending to eurozone households remains strong; in fact June net lending surpassed €25bn, registering the highest monthly increase since September 2007. Low interest rates and returning consumer confidence are contributing to buoyant housing markets and mortgage demand in many eurozone countries, as the ECB’s Bank Lending Survey showed last week.

Meanwhile, bank net lending to eurozone businesses turned positive again in June. After the March TLTRO-related lending peak, April and May saw negative net lending, but the effect is now wearing off. Net lending returned to positive territory in France, Italy and Spain, though Germany and the Netherlands contributed negatively. Indeed, a further recovery of cautious business borrowing is to be expected in the months ahead, as the TLTRO effect recedes in all countries and businesses start thinking about investing again, as last week’s Bank Lending Survey indicated.

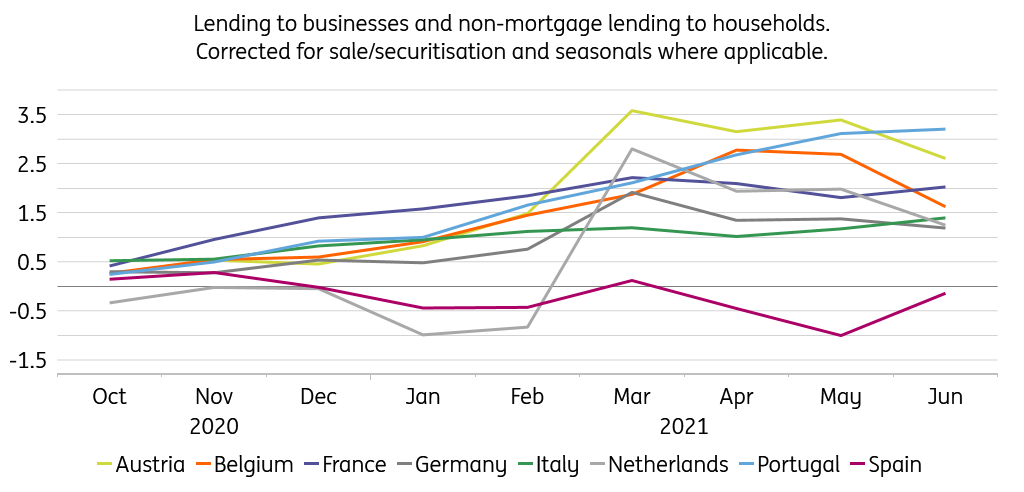

Cumulative TLTRO-eligible bank net lending growth since October '20, %

Source: ECB, ING-calculations

This also means that banks need not worry too much about their TLTRO lending benchmarks just yet. The “additional special reference period”, measuring borrowing to businesses and non-mortgage borrowing to households, runs until December (and then determines the TLTRO rate received by banks from June this year until June '22. At the country level, the main eurozone economies are all at least 1% above the benchmark right now, with the important exception of Spain, where lending has been weak since autumn last year. As Spanish bank lending did stage a recovery in June, the benchmark is now within reach.

Disclaimer: This publication has been prepared by the Economic and Financial Analysis Division of ING Bank N.V. (“ING”) solely for information purposes without regard to any ...

more

Disclaimer: This publication has been prepared by the Economic and Financial Analysis Division of ING Bank N.V. (“ING”) solely for information purposes without regard to any particular user's investment objectives, financial situation, or means. ING forms part of ING Group (being for this purpose ING Group NV and its subsidiary and affiliated companies). The information in the publication is not an investment recommendation and it is not investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Reasonable care has been taken to ensure that this publication is not untrue or misleading when published, but ING does not represent that it is accurate or complete. ING does not accept any liability for any direct, indirect or consequential loss arising from any use of this publication. Unless otherwise stated, any views, forecasts, or estimates are solely those of the author(s), as of the date of the publication and are subject to change without notice.

The distribution of this publication may be restricted by law or regulation in different jurisdictions and persons into whose possession this publication comes should inform themselves about, and observe, such restrictions.

Copyright and database rights protection exists in this report and it may not be reproduced, distributed or published by any person for any purpose without the prior express consent of ING. All rights are reserved. ING Bank N.V. is authorised by the Dutch Central Bank and supervised by the European Central Bank (ECB), the Dutch Central Bank (DNB) and the Dutch Authority for the Financial Markets (AFM). ING Bank N.V. is incorporated in the Netherlands (Trade Register no. 33031431 Amsterdam). In the United Kingdom this information is approved and/or communicated by ING Bank N.V., London Branch. ING Bank N.V., London Branch is deemed authorised by the Prudential Regulation Authority and is subject to regulation by the Financial Conduct Authority and limited regulation by the Prudential Regulation Authority. The nature and extent of consumer protections may differ from those for firms based in the UK. Details of the Temporary Permissions Regime, which allows EEA-based firms to operate in the UK for a limited period while seeking full authorisation, are available on the Financial Conduct Authority’s website.. ING Bank N.V., London branch is registered in England (Registration number BR000341) at 8-10 Moorgate, London EC2 6DA. For US Investors: Any person wishing to discuss this report or effect transactions in any security discussed herein should contact ING Financial Markets LLC, which is a member of the NYSE, FINRA and SIPC and part of ING, and which has accepted responsibility for the distribution of this report in the United States under applicable requirements.

less

How did you like this article? Let us know so we can better customize your reading experience.