The European Central Bank (ECB) goes from a net buyer of euro sovereign bonds to a net seller in 2023. Combined with high deficits, this will result in a dramatic increase in sovereign funding needs. We take a look at how markets price this increase in funding and establish a range for sovereign spreads based on our supply forecast.

Image Source: Pixabay

All hunky dory for global markets…

2023 started on a strong note for risk assets and for sovereign bonds alike. Hopes of a rapid decline in inflation has come with reduced central bank tightening fears, most evidently in growing Fed cut expectations. In addition, warmer weather and lower gas prices have boosted Europe’s economic prospects, and China’s post-Covid reopening is firmly priced by markets as non-inflationary. This environment has proved a boon for euro sovereign bond spreads, tightening on both lower base rate expectations and on better sentiment in riskier markets.

There are a lot of problems with this reasoning, however. The first is that the current market read on global macro conditions contains contradictions that are hard to avoid. The better growth prospects greeted by risk assets threatens the low inflation hopes that core bonds are cheering. In short, something has to give, and tight euro sovereign spreads stand to reverse if either risk assets or core bonds are wrong. This is not a comfortable state of play in our view.

Worse still, the spread tightening comes at a time supply conditions materially worsen for sovereign borrowers.

ECB Quantitative Tightening results in a surge in sovereign funding needs in 2023

(Click on image to enlarge)

Source: Refinitiv, Debt Management Offices, ING

… but who’s going to buy all these bonds?

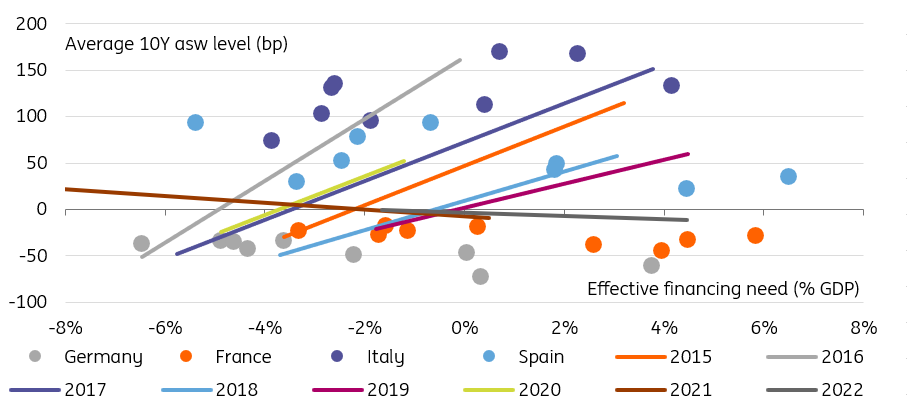

Common sense dictates that as supply increases, prices should drop, and yields rise in the case of bonds. We find this is true most of the time. Comparing effective financing needs (bond supply minus redemptions and ECB intervention) and 10Y asset swap levels (difference between 10Y yields and swap rates) for eurozone sovereigns between 2015 and 2019 shows that supply does have a good explanatory power. The problem is that this relationship has lost in significance since 2021.

Why has bond supply lost relevance for the valuation of sovereign bond spreads in the past two years? The answer is simple, an excessive amount of bond purchases in years prior numbed sovereign bond markets to the effect of supply: in 2021, spreads were already too compressed to react to more central bank purchases. This carried over into 2022 when only a handful of markets properly anticipated future increases in supply.

This increase in supply is now firmly on every investor’s radar (and with this article, ING’s rates strategy team intends to do its share). This means we expect markets in 2023 to become more efficient again in pricing relative supply dynamics.

Bond supply explain sovereign spreads most of the time

(Click on image to enlarge)

Source: Refinitiv, Debt Management Offices, ING

How do sovereign bonds trade relative to their 2023 funding needs

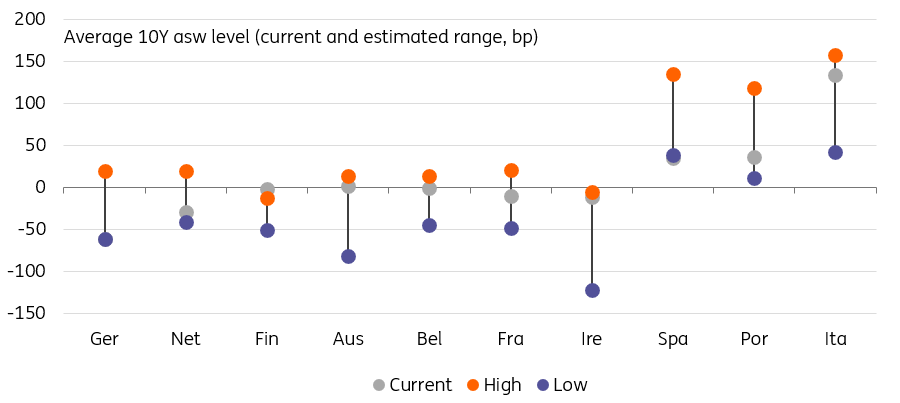

One should note, however, that this simplistic analysis is not the end-all and be-all of pricing relative sovereign yields. However, we find that other factors are stable over time. As a result, the residuals to our method of spread calculation have been relatively stable for each country over time. For instance, Italian spreads have consistently been higher than their funding needs suggested. At the other end of the spectrum, French and German yields have consistently been lower. This allows us to build a range for sovereign spreads in 2023 based on historical ‘forecasting errors’.

The chart below summarises our results. The upshot: they suggest Italian swap spreads are at the top of our estimated range, while German and Dutch ones are at the bottom. Note that one shortcoming of this approach is that it won’t, much like other forecast based on historical data, predict changes in the market’s attitude towards a specific sovereign independent of bond supply. For instance, France has historically traded between 55bp and 2bp lower than our supply-based estimate. There is no guarantee that this won’t change.

Estimated 2023 swap spread trading range based on supply

(Click on image to enlarge)

Source: Refinitiv, Debt Management Offices, ING

More By This Author:

China Reopening Rally To Drive Up Iron Ore Prices

UK Jobs Market Remains Resilient Despite Incoming Recession

Rates Spark: Bond Bull Traps

Comments

Log in or sign up to join the conversation.