Deluxe Bonds And Dividend Traps

Image Source: Pexels

Deluxe bonds and dividend traps are often high-yield stocks. Deluxe bonds can play a useful role in your portfolio, but dividend traps can seriously hurt your retirement. It's important to know the difference between them.

After writing at length about the qualities of low-yield, high-growth stocks and the reasons you should have some, it’s time I offer some insight about high-yield stocks.

To be fair, not all high yield stocks are bad investments. Some companies provide a source of high income that is fairly sustainable for investors. Some even outperform the market. Having a few of those in your portfolio might even be a good idea.

What’s a Deluxe Bond?

I coined the term “deluxe bond” to label stocks which I don’t expect to provide much capital appreciation yet still offer a good yield (above 4%) and a dividend growth policy that is enough to keep inflation in check. A “real” bond would give a high yield with no growth, so these companies are “deluxe bonds” because they are mature businesses that still generate enough growth to qualify as a dividend grower.

Finding Deluxe Bonds

To find deluxe bonds, I used our stock screener with the following metric values as filters:

|

Metric |

Value |

|

PRO rating |

minimum of 3 |

|

Dividend Safety Score |

minimum of 3 |

|

Yield |

minimum of 4% |

|

Revenue growth 5-year |

minimum of 1% |

|

EPS growth 5-year |

minimum of 1% |

|

Dividend growth 5-year |

minimum of 3% |

|

Chowder score |

minimum of 8 |

This initial search produced a list of 23 Canadian stocks (down from 28 a year ago) and 74 US stocks (down from 85 a year ago), with some duplicates due to companies trading on both markets. They are all companies with a relatively high yield (4%+) that show minimum growth and a respectable dividend triangle.

To refine the research, I would exclude all companies with a market cap under $2 billion to avoid fluctuations, which goes against the peace of mind one would expect from “deluxe bonds,” and increase the minimum PRO rating to 4 to narrow down the list to fewer than 50 companies.

Canadian Deluxe Bonds

Canadian banks fit the bill as they provide both revenue and growth. The Bank of Nova Scotia (BNS) and the Canadian Imperial Bank of Commerce (CM) are the closest to being deluxe bonds: they have less growth, but higher yield. However, any Canadian bank could be placed in that category right now due to their generous dividend yields.

Telecoms are also another classic, although I personally prefer Telus (TU) by a wide margin. You can’t forget pipelines, either. Enbridge (ENB) and TC Energy (TRP) are not known to generate double-digit returns, but they won’t fail to make generous dividend payments regularly. In the energy sector, Canadian Natural Resources (CNQ) offers a yield barely above 4%.

Labrador Iron Ore (LIFZF) also fits the bill for a deluxe bond. It comes with a bit more volatility, but it certainly has provided investors with some solid dividends in the past. With the recent drop in stock prices, some utilities appeared on that list, too. Fortis (FTS) and Emera (EMRAF) are great companies that recently reaffirmed their dividend growth policies through 2026.

US Deluxe Bonds

If we ignore Canadian companies, the list of interesting deluxe bonds in the US is quite short. Of course, you find a bunch of regional banks and energy stocks, but I see them more as speculative plays.

Target (TGT) makes the list, as its yield is now around 4%. Target lost more than half of its market valuation from its peak in 2022. I didn’t understand the previous hype, and it seems the market came back to its senses. Target will continue to grow inside the US, but don’t expect much growth here.

UPS (UPS) is another entry that recently joined the 4% club. The company will likely face some headwinds and serious competition going forward, but its dividend is definitely safe.

Realty Income Corp. (O) and NNN REIT, Inc. (NNN), with yields of 6.1% and 6.4%, respectively, may be interesting if you want to increase your exposure to REITs.

Caution About Deluxe Bonds

I use the term “deluxe bond” to describe a company with poor stock price appreciation potential but with a decent yield (above 4%) and a minimal dividend growth policy (at least 3%). However, the wind can change quickly, turning these deluxe bonds into dividend traps.

What’s a Dividend Trap?

A dividend trap is a stock that has nothing to offer besides its yield. It would offer little to no capital appreciation potential, and would provide no steady dividend growth in step with inflation.

Often when a company fails with its total return, income-seeking investors may turn a blind eye and focus on their dividends. In other words, the stock price could decline but as long as the dividend is paid, investors would keep smiling.

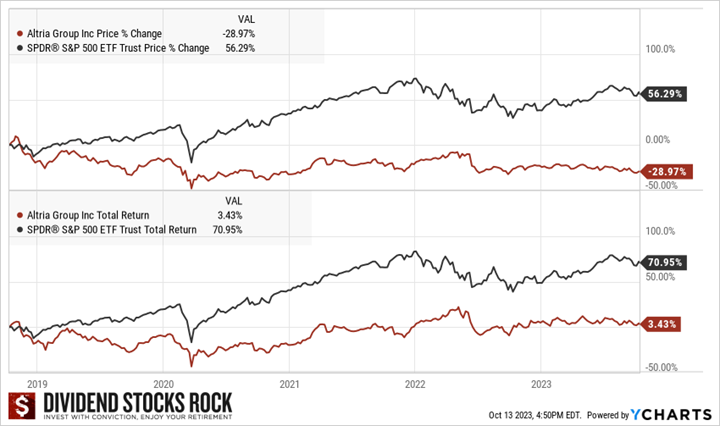

The most pernicious traps are the ones that don’t cut their dividend but instead increase it to keep the hope alive. Think of a stock like Altria Group (MO). Many investors like to say “more money,” but are they really getting more? I’ll let you be the judge.

Over the past five years, the stock price lost almost 30%. However, when you consider the dividend, MO’s total return comes back to positive territory at 3.4%. Maybe you’re tempted to say it’s “okay” since you didn’t lose money. However, if you had invested in the S&P 500 instead, you would be up 71%. That’s a costly choice, in my opinion.

If you want to identify a dividend trap, start by looking at your high-yield stocks and consider their dividend triangle. Is the stock price steadily declining while the dividend is flat or slightly increasing occasionally? Is there any growth? If there is, is it sustained growth in revenue and earnings? Also, consider your investment thesis. If the word “yield” is part of your thesis, you’re on the right track to identify the trap.

Final Thoughts

Having high yield stocks in your portfolio is not a bad strategy as long as they provide dividend growth along the way to cover inflation and modest capital appreciation. Keep an eye on your high yielders to make sure you’re not falling into a dividend trap.

More By This Author:

Sniff Out Dividend Cuts

Why Ignore Low Yield Stocks When Planning Retirement?

The Death Of Renewables? - September Dividend Income Report