Image Source: Pexels

As expected, the Czech National Bank's interest rates remained unchanged. The new forecast has completely changed the central bank's message, but our view remains stable. The risk of further rate hikes is low and FX interventions play a major role. However, their costs are manageable at the moment and the central bank can avoid raising interest rates.

CNB tries to avoid rate hikes at all costs

As expected, the Bank Board left interest rates unchanged at 7.00% today, in line with surveys and market expectations. In its statement, the phrase "...CNB will continue to prevent excessive fluctuations of the koruna exchange rate" returned after a hiatus in September. As expected, five board members voted in favor of the decision and two members voted for a 75bp rate hike.

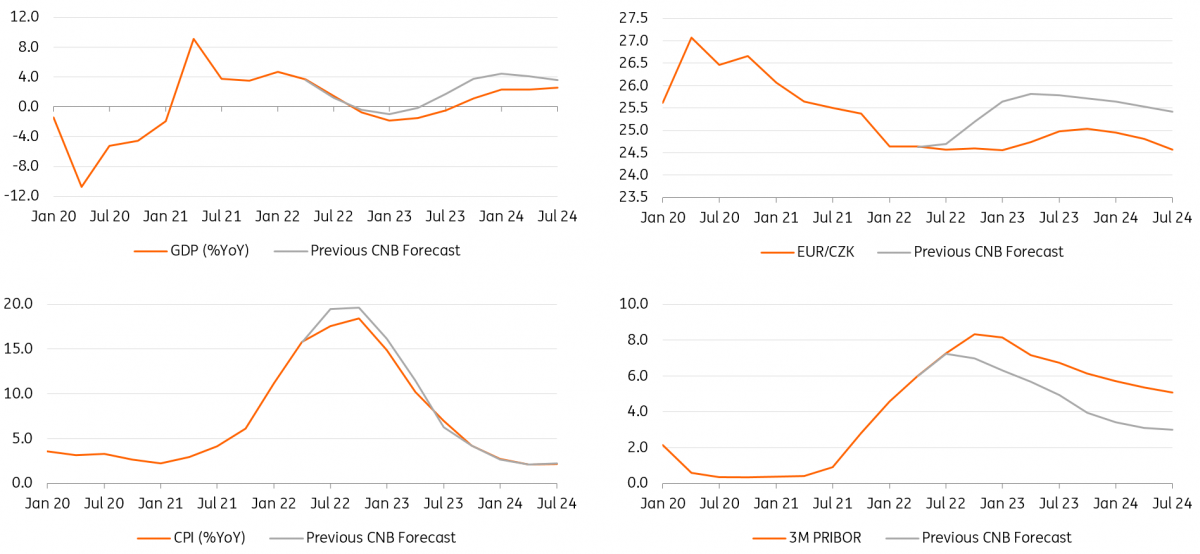

If we are looking for a surprise at this meeting we can find it in the new forecast, which has undergone a significant transformation. Economic growth has been downgraded over the entire forecast horizon especially next year, with the CNB expecting -0.7% on average (vs. the previous 1.1%). The path of inflation is also lower over almost the entire horizon. However, the CNB now expects inflation to peak at 19.1% year-on-year in December this year. On the other hand, the 3M PRIBOR trajectory is surprisingly much higher, projecting 8.35% on average for the fourth quarter of 2022 (vs. 7.31% currently). Moreover, the CNB forecast ends at 5.07% (vs. 3.01% previously). The CNB's projection has shifted significantly to stronger levels, especially next year. Overall, the CNB's new forecast thus shows slower economic growth, including a recession next year and lower inflation, alongside a massive tightening of monetary conditions.

New CNB forecast

(Click on image to enlarge)

Image Source: CNB

Board prefers stability in interest rates

Despite the rate forecast implying a 2W repo rate averaging 8.00% in the fourth quarter of 2022, the governor said the board prefers stability in interest rates. The board sees risks as significant and going in both directions. Their list remained unchanged from the September meeting. The CNB sees faster wage growth, expansionary fiscal policy, higher producer prices abroad, and unanchoring inflation expectations as upside risks. On the other hand, the central bank sees as anti-inflationary the rising likelihood of a recession abroad, a stronger-than-expected decline in domestic demand and investment, the introduction of an energy price cap, and a faster-than-expected decline in core inflation.

The Bank Board assures the public that the CNB’s actions will be sufficient to restore price stability in accordance with its statutory mandate.7th CNB Situation Report on Economic and Monetary Developments

No change in our view

Despite the big changes in the CNB's forecast, nothing has changed in our view of the main story today. The board considers interest rates high enough and FX interventions are doing their job well with no end in sight for now. Thus, we continue to see the risk of additional rate hikes as low and consider the hiking cycle to be closed, the only one in the CEE region. Of course, we will continue to monitor wage developments and the cost of FX interventions, which we identify as the two main risks to a potential additional rate hike. However, in the longer term, we believe the board is more open to cutting interest rates in the event of negative economic developments than the forward guidance picture provided by the CNB.

What to expect in rates and FX markets

In our view, the main message for the market is the significantly higher interest rate trajectory in the CNB's new forecast. We found the entire IRS curve 8-13bp higher with flattening bias after the press conference. One can assume that the market will buy the central bank's "higher rates for longer" narrative and move rates higher in the days ahead. However, the CNB's new forecast also shows a big drop in October year-on-year inflation from 18.0% to 17.4% YoY, which will be released next week. This in our view creates room for an upside surprise and a resurgence in market hopes for additional rate hikes and could open the door to rate receivers at the short end of the curve or to steepens supported by rising core rates.

On the bond side, Czech government bonds remain near their cheapest levels in nominal and relative terms. However, we remain in a wait-and-see mode until the situation on the supply side clears up. Core rates will continue to push CZGBs to sell off further while domestic conditions send mixed signals. Fiscal policy is expanding, while only one auction is scheduled for November after months of heavy supply. This leads us to believe that the additional spending will be covered by means other than CZGBs issuance. However, we lack more clarity for now. Nevertheless, once the global sell-off is over, we believe CZGBs will return to the top of investor interest within the CEE region.

On the FX side, the situation remains unchanged. CNB interventions will continue and the line in the sand is clearly drawn at 24.60-70 EUR/CZK. Given the low central bank costs, we do not expect any changes in the CNB's approach anytime soon. This set-up coupled with relatively high carry may serve as a good base against the Polish zloty or Hungarian forint, which are much more vulnerable in global EM sell-offs, especially ahead of the upcoming winter.

More By This Author:

Spanish Housing Market: Is A Correction Looming?

FX Daily: Bearish Steepening Of Money Market Curve Lifts The Dollar

FX Daily: Dodging The Pivot

Comments

Log in or sign up to join the conversation.