Image Source: Pexels

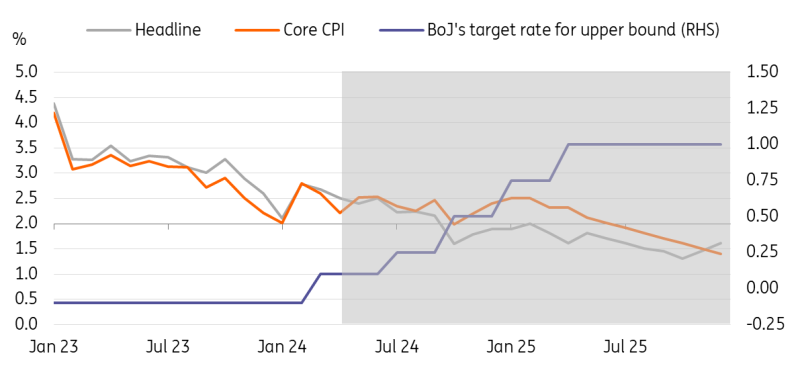

Both headline and core inflation moderated a bit, a touch below market consensus

Consumer price inflation rose 2.7% year-on-year in March (vs 2.8% in February and market consensus). Core inflation excluding fresh food rose 2.6% in March (vs 2.8% in February, 2.7% market consensus). They slowed down mostly due to base effects, the monthly comparison continued to rise by 0.2% month-on-month sa with both goods (0.2%) and services (0.1%) prices up. Fresh food prices increased but durable goods prices continued to decline. Among services, telecommunications and leisure-related fees rose the most.

Furthermore, the early April Tokyo inflation, which will be released on the day of the BoJ meeting, is expected to slow again. However, this also should be mostly due to a high base. We are not particularly concerned about moderation of inflation as both headline and core are running well above the BoJ’s 2% target, so we expect the BoJ’s normalisation efforts to continue throughout the year.

BoJ watch

Markets widely predict no policy change at its upcoming April BoJ meeting, following last month’s decision to dismantle the negative interest rate policy and yield curve control programme. Of more interest next week is the BoJ’s quarterly outlook report. We expect the BoJ to revise up its inflation outlook. We will also see the BoJ’s first forecast for FY26, which is expected to show core inflation at 2%. These will be an important factors in determining when and how much interest rates will be raised.

Given that higher commodity prices combined with a weak yen are hikely to push up both headline and core inflation, the BoJ’s need to raise rates sooner than market consensus is likely to increase in our view. Recent hawkish comments from Governor Ueda also signal a change in tone in the BoJ's response to the currency move. He said that if the impact of the weak yen becomes too big to ignore, it might lead to a change in monetary policy. Currently market consensus is October hike, we have penciled in a 15bp hike in July and a 25bp hike in October.

CPI will stay above 2%, support the BoJ's policy normalisation

Source: CEIC, ING estimates

More By This Author:

The Commodities Feed: Oil Surges On Escalation FearsRates Spark: The Lost Term Premium To Return

Asia Week Ahead: BoJ Meeting And Inflation Readings From Australia, Japan And Singapore

Comments

Log in or sign up to join the conversation.