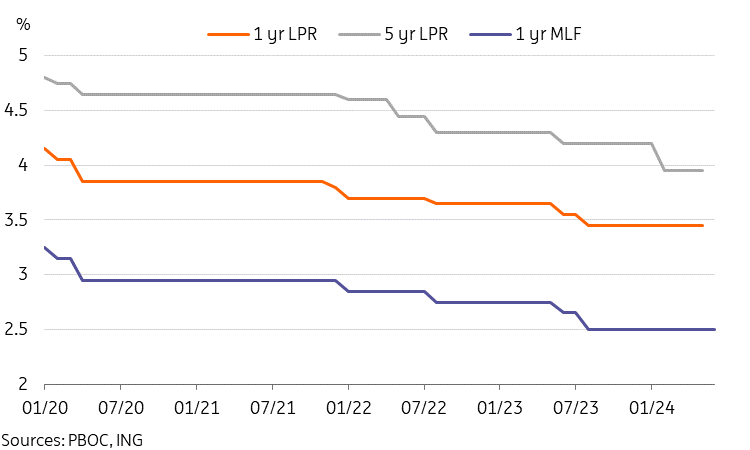

The People’s Bank of China has kept the MLF rate unchanged amid growing pressure from sluggish economic data to further ease policy.

Rates still on hold but likelihood of cuts are rising

The People's Bank of China kept the one-year medium-term lending facility rate unchanged at 2.5% today, in line with market expectations.

Last Friday's May aggregate financing data rebounded from April's but came in softer than market forecasts. RMB 2.06tr of new aggregate financing and RMB 819.7bn of new RMB loans showed weak credit activity continuing. This was of little surprise; we have been repeatedly stating in the past few months that loan demand remains inadequate and real interest rates remain too high given the current state of the economy, and that a rate cut would be beneficial to support the economy at this juncture. Inflation should pick up more toward the second half of the year but is unlikely to be an impediment to rate cuts given how low it has been in the first half of the year.

We believe that in conjunction with today's data releases and the start of rate cuts in other central banks such as the European Central Bank and Bank of Canada, the odds of a PBoC rate cut in the coming months have risen. It is likely that the PBoC has held off from rate cuts to date in consideration of the top level policy priority to maintain currency stability at a reasonable and balanced level. However, economic data developments have continued to add to the case for a rate cut and could cause a PBoC cut even if the Federal Reserve remains on hold. We expect two rate cuts of 10bp each before the end of the year, though this could come in the form of one larger rate cut as well, depending on policymakers' priorities. Two smaller rate cuts could result in less short term depreciation pressure versus one bigger cut.

PBOC kept the MLF unchanged despite mounting pressure

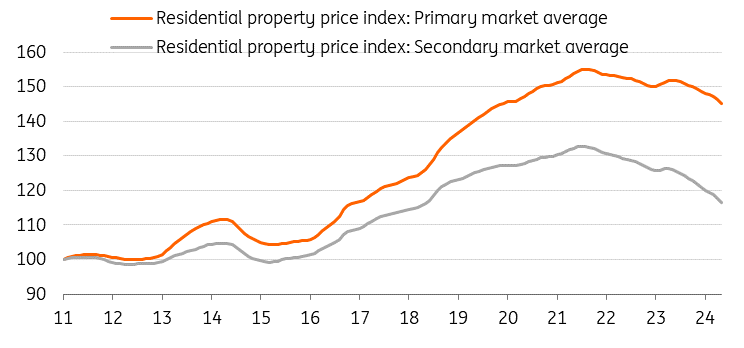

Property market continued to slump despite supportive policy push

China's 70-city housing prices continued to decline in May, with new home and used home prices down -0.7% month-on-month and -1.0% MoM respectively, both seeing the steepest monthly sequential declines of the current cycle. From the peak, new home prices have declined -6.4% and the secondary market has declined -12.3%.

Of the 70 city sample, only two cities (Shanghai and Taiyuan) saw an increase in prices in May for new homes, while none saw an increase in the secondary market. This was notably worse off compared to April, when six cities saw increases in new home prices and one city saw an increase in secondary market prices. Year to date, two cities saw new home prices increase, and none saw secondary market prices increases. 16 and 48 cities within the sample have seen declines of over 3% in primary and secondary markets respectively. New home sales remained well in contraction at -27.9% year-on-year YTD.

Real estate investment fell to -10.1% YoY YTD in the first five months of the year, down from -9.8% YoY YTD in the first four months of the year. Once again, this came in weaker than market consensus expectations, even after economists have turned more pessimistic on this indicator. New home starts fell -24.2% YoY YTD, which was a slightly smaller decline than previously.

This data was certainly on the disappointing side and may ring some alarm bells, as May's policy support package has not yet translated to a slower decline of housing prices, let alone a stabilization. This data further indicates that the property sector will remain a headwind on growth this year. With that said, we caution against overreaction, and it is still worth waiting for a few months of data as some lag could be expected.

May housing prices disappointingly saw a faster decline

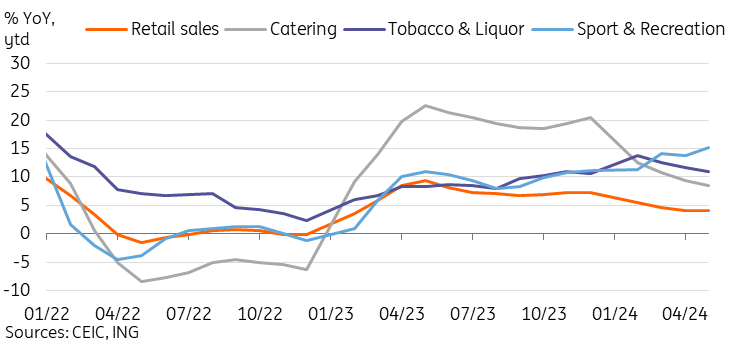

Retail sales rebounded on base effect as categories remained uneven

May retail sales rose to 3.7% YoY, up from 2.3% YoY in April. This was a little weaker than our forecasts for 4.1% YoY growth, but well above market forecasts for 3.0% YoY. The recovery is mostly a base effect story, as last May saw a sharp decline in retail sales, but also showed some positive signs that the impact from trade-in policies may be starting to take effect. Year to date growth remained unchanged at 4.1% YoY.

In terms of subcategories, the biggest movement was in cosmetics, which surged 18.7% YoY after seeing negative or low single digit growth for most of the year. As trade-in policies started to take effect, housing appliances also saw an increase to 12.9% YoY. Given the limited time window for many of these programs, the boost may be relatively short-lived. The "eat, drink, and play" categories which we have preferred continued to outperform the headline in May. Catering (5.0%), tobacco (7.7%), sports & recreation (20.2%) continued to remain well above headline growth despite a high base from 2023. There was very limited appetite for big ticket purchases, as evidenced by negative growth in retail sales of gold and jewellery (-11.0%) and auto (-4.4%).

Consumers continuing to prioritize "eat, drink, and play" over big ticket purchases

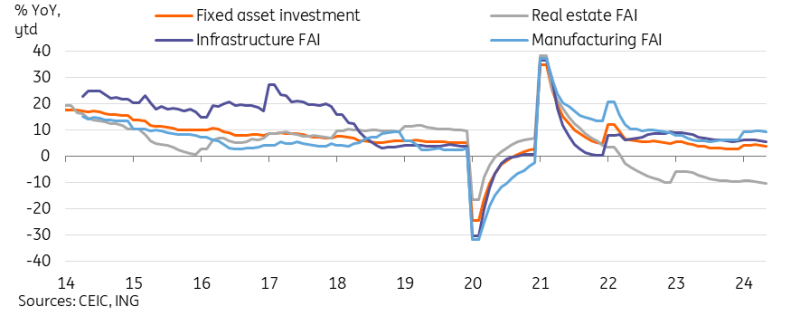

Fixed asset investment continued to slow in May

Fixed asset investment (FAI) growth slowed for the second consecutive month in May, down to 4.0% YoY YTD from 4.2% YoY YTD. This came in weaker than both our and market expectations.

Most major categories slowed slightly across the board in May. Property investment and tepid private sector investment (0.1% YoY YTD) continued to drag overall investment. The public sector (7.1%), manufacturing (9.6%) and infrastructure (5.7%) on the other hand remained the main areas of growth but slowed slightly in May. After the proceeds from the central government's ultra-long term bonds are put to use, we could see some stabilization of investment growth in the second half of the year. It is likely that in the near term, investment growth will continue to be heavily driven by the public sector, as private sector sentiment has yet to recover. It is possible that potential rate cuts could help support private sector investment to an extent, but this recovery will likely take time and a sustained policy rollout.

Investment slowed across the board in May

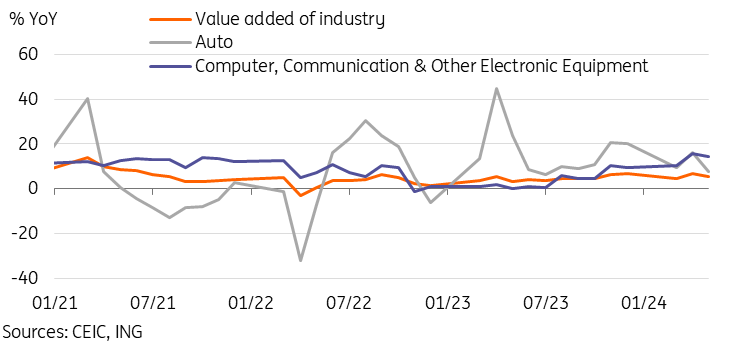

Industrial production slowed by more than expected

May industrial production growth fell to 5.6% YoY down from 6.7% YoY, which was a steeper than expected drop. Manufacturing has so far been the main upside surprise for growth in the year to date but may be coming under more pressure in the coming months as tariff actions against Chinese autos could start to restrict manufacturing demand.

Auto production fell to 7.6% YoY in May, which came in considerably softer than the growth in the previous months. The overall year to date growth slowed to 10.5% YoY as a result. With tariff actions from the US and EU set to take effect in the coming months and likely to impact export demand, auto production could come under more pressure in the second half of the year.

On the brighter side, hi-tech manufacturing continued to show solid growth in May, growing 10.0% YoY. The computer, communications, and other electronic equipment category also exhibited strong growth of 14.6% YoY. Amid a technology self-sufficiency push, these categories are likely to remain strong in the foreseeable future.

Auto manufacturing could slow amid tariff action, but hi-tech to continue outperformance

More By This Author:

FX Daily: Four G10 Central Banks In Action This WeekCentral Banks Take One For The Team

Battle Of The Bad News Stories – Brazil Or Mexico?

Comments

Log in or sign up to join the conversation.