Strong demand from the electric vehicles and renewables sectors in China has helped to lift demand for aluminium, despite the prolonged crisis in the metals-intensive property market

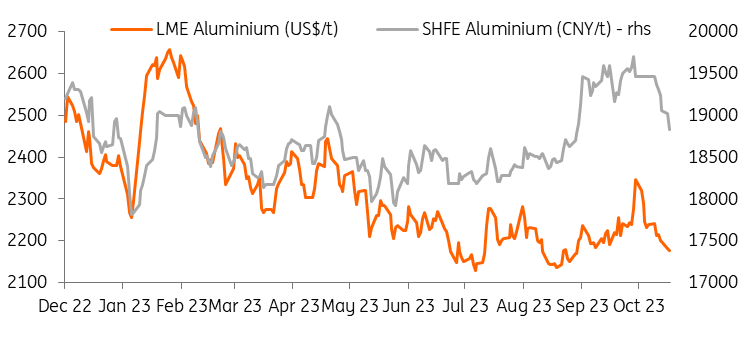

SHFE aluminium prices have remained stronger than LME for most of 2023

SHFE, LME, ING Research

Aluminium prices in China have remained stronger than global prices for most of the year. London Metal Exchange (LME) aluminium prices have slumped more than 8% this year, while prices on the Shanghai Futures Exchange (SHFE) are up more than 1% year-to-date. Chinese demand for aluminium has been resilient throughout the year amid growing demand from the green sector, despite the country’s disappointing economic recovery.

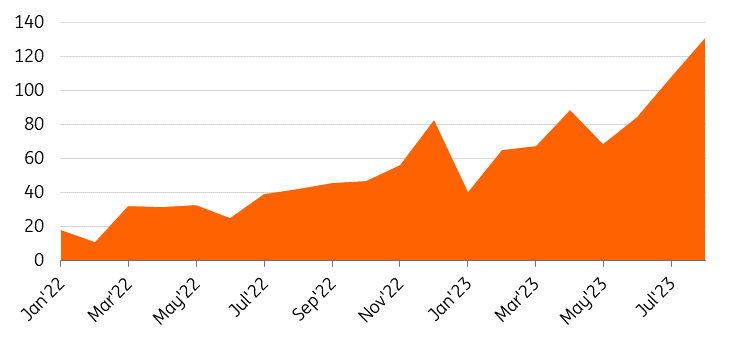

Open arb window boosts aluminium flows into China

An open arbitrage window resulting from SHFE prices outperforming the LME has boosted aluminium flows into China. China’s imports of unwrought aluminium and products jumped 63.2% year-on-year to 331,716 tonnes in September. Cumulatively, imports rose 21.5% YoY to 2.04 million tonnes in the first nine months of the year.

Imports of bauxite, a key raw material for aluminium, totalled 10.02 million tonnes last month, up 23.1% from the previous year. The first nine months saw bauxite imports rise 12.8% YoY to 106.6 million tonnes.

China aluminium total imports (metric tonnes)

China Customs, ING Research

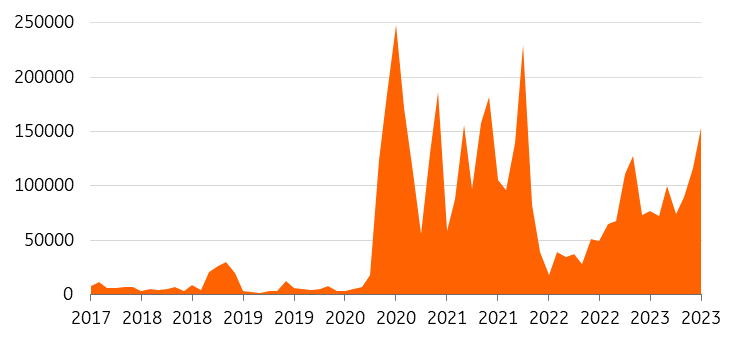

However, many of these imports are from Russia. There are no sanctions on buying Russian material, but many Western buyers have been self-sanctioning since the invasion of Ukraine, with China absorbing a large part of this shunned material.

Imports of Russian aluminium accounted for 87% of China’s total in the first eight months of 2023. This trend is likely to continue as Europe presses on with self-sanctioning.

Primary aluminium imports from Russia (thousand tonnes)

China Customs, ING Research

China aluminium output hits a record in September

Imports are continuing to surge despite domestic output hitting new highs. China’s aluminium production hit a record in September, with smelters in the southwestern province of Yunnan – China’s fourth largest aluminium-producing region – continuing to ramp up production amid improving hydropower supply.

Aluminium output rose to around 119,000 tonnes a day last month, higher than the previous record of 116,000 tonnes set back in August. September’s primary aluminium output was up 5.3% compared with a year earlier at 3.58 million tonnes. Primary aluminium output totalled 30.81 million tonnes in the first nine months of 2023, up 3.3% from the corresponding period in 2022.

Restarts in Yunnan are taking place, but if the upcoming dry season (which usually lasts from December until March) has insufficient rain, Chinese output could disappoint again. Additional supply cuts due to a lack of hydropower could lead to higher imports. Last year, smelters in the province were forced to cut output amid low rainfalls and low water levels, reducing 2 million tonnes of capacity. The capacity cap of 45 million metric tonnes will limit smelter expansion in the country, which could drive the need for more imports.

China primary aluminium output (thousand tonnes)

National Bureau of Statistics, ING Research

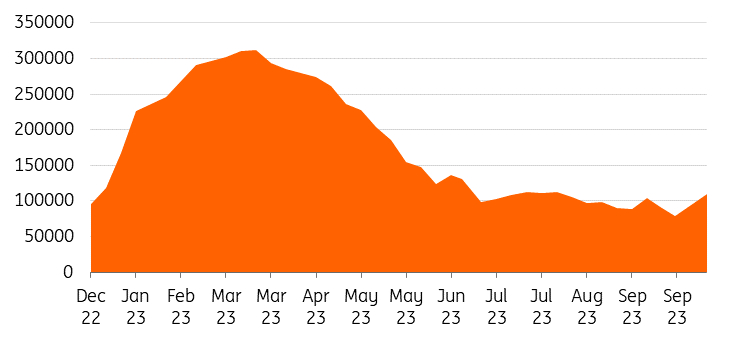

Strong import data was underpinned by low domestic inventories of aluminium. Aluminium stocks on the SHFE sank to a low of 79,194 tonnes last month – the lowest since March 2019 and down from a peak of 311,000 tonnes in March this year, indicating resilient domestic demand for the metal.

SHFE weekly aluminium deliverable stocks (metric tonnes)

SHFE, ING Research

Green parts of the economy are growing

While demand for aluminium in traditional industrial sectors has weakened this year, Beijing’s decarbonisation efforts have boosted the need for metals (including aluminium) that are key to renewable energy-related manufacturing from EVs to solar panels. China’s green energy drive is part of its efforts to meet dual carbon goals set in 2020 when it pledged to achieve peak CO2 emissions before 2030 and carbon neutrality by 2060.

Aluminium is a key component in mobility and transport, buildings, construction, packaging, aerospace, and defence. It is also used in almost all energy generation, transmission, and storage technologies, particularly those that will deliver the energy transition, such as wind and solar power, alternative fuel cells, hydrogen production, high-voltage cables, and batteries.

China’s new energy vehicles (NEV) sector, including battery electric vehicles and plug-in hybrids, is growing rapidly. NEV production in China grew more than 37% per year in the first eight months of the year, reaching 5.44 million, according to China Customs data.

In battery electric vehicles, aluminium is used in e-drive housing, battery pack housings, ballistic battery protection, and cooling plates. Additionally, aluminium plays a crucial role in electromobility infrastructure, including power cables and charging stations. China is also the biggest seller of EVs. In the first eight months of the year, China exported 1.08 million EVs, a 61% increase in export volume compared with the same period in 2022, China Customs data showed.

China has massively pushed EV production and sales in recent years with government policies and incentives for both manufacturers and consumers. As a result, China has become the frontrunner in EV markets, accounting for around 60% of global electric car sales in 2022. More than half of the electric cars on roads worldwide are now in China and the country has already exceeded its 2025 target of 20% for new energy vehicle sales, according to data from the International Energy Agency. As the demand for EVs continues to grow, so does the demand for the minerals inside them. This trend should support aluminium demand looking forward.

Meanwhile, Chinese solar demand is also growing rapidly. Aluminium is the single most widely used mineral material in solar photovoltaic (PV) applications, according to the World Bank. The metal accounts for more than 85% of the mineral material demand for solar PV components, from frames to panels. China leads in terms of solar PV capacity additions, with installed capacity set to cross the 500 gigawatts (GW) mark by the end of 2023, accounting for around 40% of global capacity. For comparison, the US is in second place with 145GW, accounting for about 12%.

China’s new capacity in 2023 is expected to top 150GW, almost doubling the 87GW installed in 2022. About 165GW is expected to be added in 2024 and 170GW in 2025. This growth will see China’s cumulative solar PV capacity reach over 700GW by 2024. It'll then increase to close to 900GW by the end of 2025, before topping one terawatt (TW) in 2026, according to data from Rystad.

The 14th Five-Year Plan for Renewable Energy, released in 2022, has set ambitious targets for deployment which should drive further capacity growth in the years ahead. China is also a major supplier of solar panels to the rest of the world. Chinese export data showed solar panel exports growing by 34% in the first half of the year, with 114GW shipped worldwide, with half of the shipments destined for Europe. This compares to 85GW in the corresponding period last year.

China’s green push to boost green metals demand

China’s construction sector remains under pressure and is adding to short to medium-term challenges for aluminium demand. At the same time, the green parts of the economy will continue to grow, which should offset the weakness from the more traditional sectors and boost the need for green metals, including aluminium.

However, China’s energy transition path is not without its challenges. Droughts last summer forced cities in southwest China to curb power supply to heavy industries, disrupting aluminium production in the country. In Yunnan, that was the second consecutive year that saw the province cut its aluminium output.

As China continues to decarbonise its aluminium industry, and as more smelters move from coal-dominated Shandong to hydropower-dominated Yunnan province, it's left more vulnerable to further disruptions with green energy being heavily reliant on weather conditions and patterns.

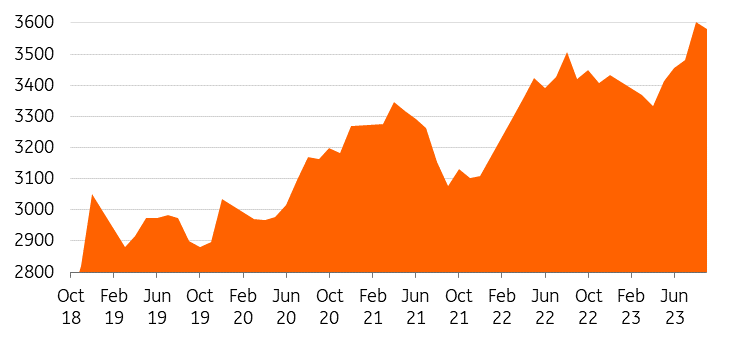

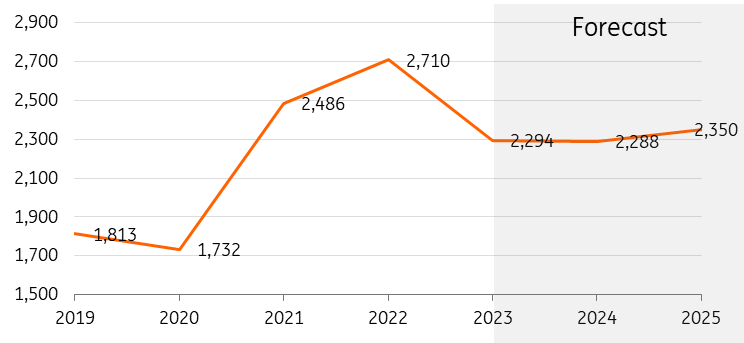

ING forecast

ING Research / LME Aluminium (US$/t)

More By This Author:

Polish Manufacturing Bottoming Out And Producer Prices Starting To StabiliseAsia Week Ahead: Regional Inflation Readings Plus Growth Figures From Korea

Business Sentiment Darkens In France, Signaling A General Loss Of Economic Dynamism

Comments

Log in or sign up to join the conversation.