Image Source: Pexels

While there has been some speculation about rate cuts, today's cut was not widely expected, and coming just ahead of the monthly activity data suggests that this set of numbers could be very weak.

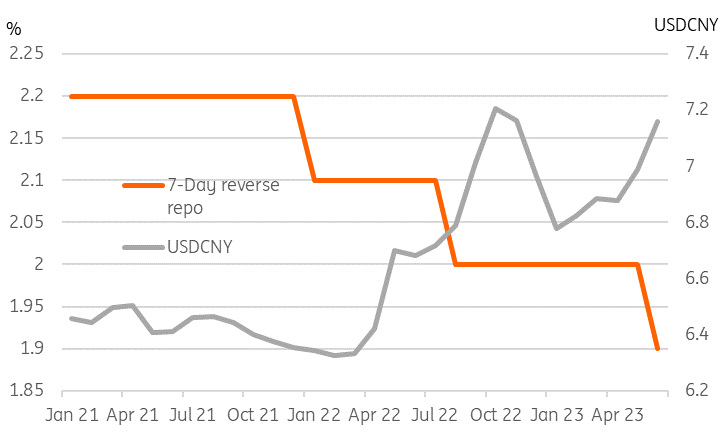

Reverse repo rate cut, 1Y MLF next?

Before today's hike, the received wisdom had been that the People's Bank of China would not use blanket rate cuts as a first resort, but would rather use some of its more focused tools, such as targeted RRR cuts. So the 10bp cut of the 7-Day reverse-repo rate today raises some questions.

The first of which is whether this will be followed by a cut to the 1-Year Medium-Term Lending Facility (1Y MLF) on Thursday. Our first guess on this is, yes, probably. After all, window guidance on deposits was also lowered earlier in the month, so there does seem to be a general easing of policy going on.

The next question is, why now? What has changed? Certainly, China's reopening has been quite tepid, with a catering-led consumer spending surge that already looks to be losing steam and manufacturing still struggling. Activity data on retail sales is also due on Thursday, and it may be no coincidence that rates are being eased only days ahead of this release if it turns out that the reopening is already sputtering.

If the one engine of growth - retail sales - is not delivering what is required of it, and if the other sectors of the economy are failing to pick up the slack, then broader stimulus measures like these would seem appropriate. The consensus forecast for retail sales is for a 13.8% year-on-year rise, which sounds pretty strong. But it translates into about a 1% month-on-month (sa) decline, and the apparent strength is all due to base comparisons.

7-Day reverse repo rate and USD/CNY

Image Source: CEIC, ING

CNY weaker will drag other currencies with it

The Chinese yuan has weakened above 7.16 at times today, adding to the month and a half of weakness it has already experienced. Further stimulus may prompt some short-term reversals, or slow the slide. But it may take a more concerted improvement in the macro data before the CNY turns decisively. Short of a substantial boost from fiscal policy, such as loans from the central government to local governments to spur infrastructure spending, that doesn't look on the cards just yet, though today's move does indicate that the authorities' patience with the weak recovery is wearing thin.

More By This Author:

FX Daily: Jumping On The Inflation Swing

The Commodities Feed: USDA Pushes Up Wheat Supply Estimates

Sticky UK Wage Growth Means No Rate Cuts For The Bank Of England Until 2024

Comments

Log in or sign up to join the conversation.