The euros aren’t the only thing kicking off this week. James Smith looks at how central banks are struggling to avoid political low tackles as he takes you through another packed week ahead

Hat-tricks and own goals

Euro 2024 kicks off today, so brace yourself. Expect tortured football analogies aplenty for the next month. Remember, economists like me don’t get out much. I don’t even know much about football, so this could be painful.

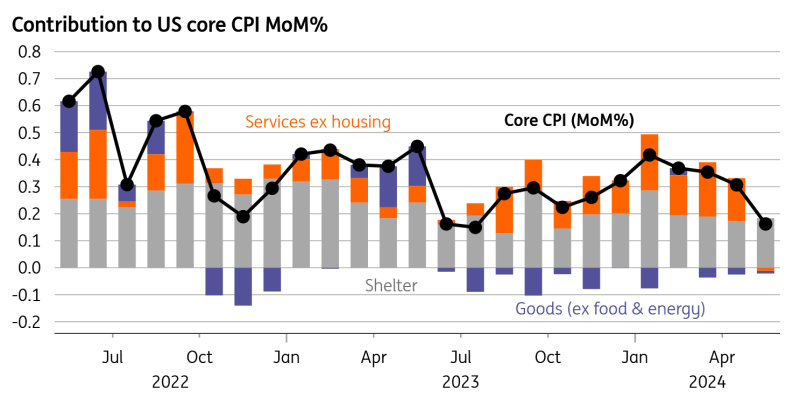

Anyway, some good news at last: both US consumer and producer price inflation came in lower than expected this week. One month doesn’t make a trend, so it’s not exactly a half-time equaliser (am I doing this right?). Fed gaffer Jay Powell was understandably reluctant to sound the all-clear in his post-meeting presser.

Come September’s meeting, however, James Knightley reckons we’ll have seen enough. He expects a hat-trick of rate cuts this year, whatever the latest Fed ‘dot plot’ might tell us.

Still, even if life ‘on the pitch’ is getting slowly easier for central bankers, there are plenty more issues off it. I’m talking about politics, an uncomfortable area for any banker or economist - just ask Andrew Bailey at the Bank of England... he's still suffering from a groin strain after Liz Truss's 2022 mini-budget debacle.

Over in Europe, Christine Lagarde's hoping she can avoid the fallout of last weekend’s political fireworks. Carsten reckons it’s a bit early to call the widening in French spreads either unwarranted or dangerous. But there might be a few officials in Frankfurt dusting off the instruction manuals for the Transmission Protection Instrument (TPI) just in case. It's a bit like the off-side rule, but different.

Carsten doesn’t think the election changes much else for the ECB though. In fact, he reckons a July rate cut is just about as likely as Albania winning the euros this year (he’s obviously feeling confident about Germany’s chances).

Here in London, the BoE hasn’t managed to avoid the election campaign entirely. Politicians have spotted an opportunity to save the Treasury a few quid on reserve remuneration. And when it comes to the meeting next week, markets reckon the election has totally written off a rate cut. Sticky services inflation hasn’t helped.

But I wouldn’t rule anything out entirely. Governor Bailey sounded keen to get on with the job of cutting rates back in May. Other officials seem less convinced, and for now, he seems to have lost the dressing room.

It’s not like much is likely to change after the 4 July election, either. The Labour Party, widely expected to score a landslide, isn’t planning any major changes on tax or spending. An August rate cut is still our base case. I’d say it’s even more likely than England winning the euros. Make of that what you will.

Over in Washington, I’m sure officials wish things were as simple. Rate cuts and their timing will inevitably become politicised, though luckily for the Fed, the November meeting falls two days after the Presidential election. James K thinks that should make it easier for the Fed to cut rates in that month. It might have been a very different story if the meeting came just a few days earlier.

Even so, the result will undoubtedly shape the way the Fed acts in 2025. The Trump campaign has talked about fresh tax cuts, big tariff hikes and tighter immigration. James thinks that’s a mix that could see slightly stronger growth and higher inflation than under President Biden, and that could limit the scope of Fed rate cuts in 2025. As for Chair Powell himself, the risk is that it ends in a last-minute red card depending on who prevails on 5 November.

That’s the final whistle for this week. If you thought that was bad, just wait for the Olympics.

Chart of the week: Finally, some good news on US inflation

Macrobond, ING calculations

THINK ahead in developed markets

US (James Knightley)

-

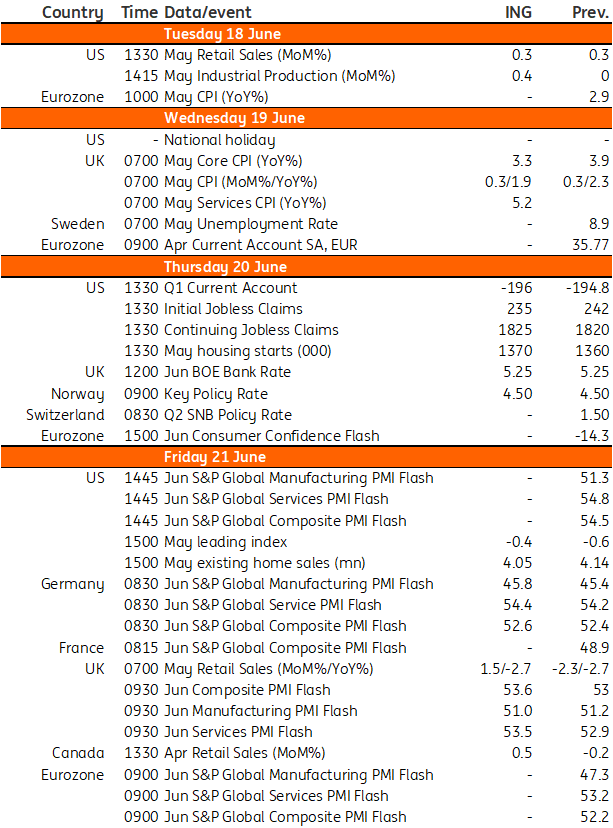

Retail sales and Industrial production (Tue): Softer inflation prints have revived the case for monetary policy easing in the US despite the Federal Reserve scaling back its outlook for monetary policy from the three 25bp cuts it signalled in May to the one it projected last week. In terms of next week, the focus will be Tuesday with the release of retail sales and industrial production and any weakness could put further downward pressure on interest rate expectations.

-

Consumers appear to be becoming more cautious about discretionary spending as financial pressures from weak real household disposable income growth, exhausted pandemic-era savings and high consumer borrowing costs impact more and more households. Lower gasoline prices are also likely to weigh on the dollar value of retail sales. Nonetheless, high-income households continue to spend strongly and we look for 0.3% month-o-month overall growth. Industrial production may also rise modestly, but the underlying trend is flat with business surveys showing little sign of an imminent upturn.

UK (James Smith)

-

UK inflation (Wed): We expect services inflation to dip back after last month’s data came in well above expectations. That was due to annual price hikes at the start of the financial year that won’t be repeated again in May. Headline inflation should dip slightly below the 2% target and stay there or thereabouts for much of this year.

-

Bank of England (Thu): Better news on inflation ahead of the meeting is unlikely to be enough to convince the committee to cut rates this month, though we think markets are wrong to totally rule it out. Investors are minded to think the committee won’t move during an election campaign, but remember in May the Bank did seem very close to the first move. Our base case is for the first cut in August.

Switzerland

-

Swiss National Bank Meeting (Thu): After the surprise rate cut in March, our team’s base case has been for another rate cut this month. Remember the SNB only meets once per quarter. That gives the bank fewer opportunities to move, but the consensus now expects rates to stay on hold. Inflation is low relative to its peers, while the SNB hiked rates less aggressively which some have argued reduces the need to act next week.

THINK ahead in Central and Eastern Europe

Poland (Adam Antoniak)

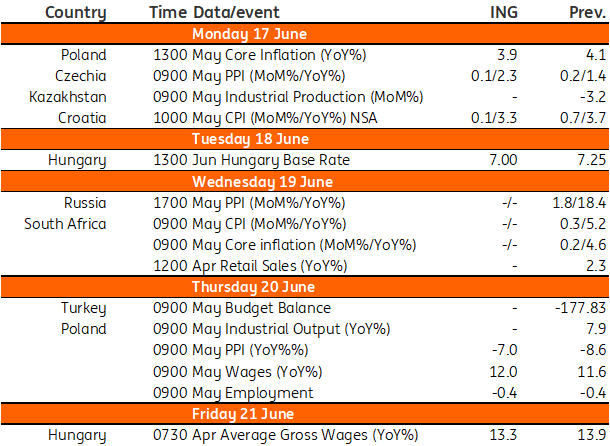

- Industrial Output (Thu): Markets will focus on industrial output data as the recovery in manufacturing is still lacklustre. Recent releases were a real rollercoaster as readings are strongly impacted by calendar effects. The May reading is expected to be soft (1.0% year-on-year vs. 7.9% YoY) due to two fewer working days and two long weekends at the beginning and the end of the month.

- Wages & Employment (Thu): The labour market report should confirm still solid (double-digit) growth in wages and a slight decline in employment.

Hungary (Peter Virovacz)

-

NBH meeting (Tue): Negative month-on-month inflation in May was good news for the National Bank of Hungary. What was less positive was the underlying inflationary pressure, which is heating up on an annualised basis. Add to this the recent underperformance of the forint and the divergence between the Fed and the ECB, and we once again see a cautious central bank that could cut the key rate by only 25bp to 7.00% in our view. Moreover, it may signal even less (or no) room for further rate cuts in the coming months than in its May forward guidance.

-

Wages (Fri): April's wage data could be the ultimate test of the business surveys at the start of the year, which suggested that companies were planning to raise wages in the 5-10% range in 2024. Instead, what we have seen so far is a more lively pace of wage growth. If we see a significant slowdown in the data, this could be good news for monetary policy. Otherwise, still-unfolding wage pressure could increase the possibility of wage-push inflation later this year.

Czech Republic (David Havrlant)

- May PPI (Mon): The PPI will reflect lower Brent crude prices and a stronger Czech koruna in May on the one hand, and increasing wage costs in a tight labour market on the other hand. The cyclical economic rebound driven by both domestic and foreign demand will likely keep the annual dynamic in PPI on an upward trajectory.

Key events in developed markets next week

Refinitiv, ING

Key events in EMEA next week

ING's James Smith, Adam Antoniak, Peter Virovacz, David Havrlant, and James Knightley contributed to this article.

More By This Author:

Battle Of The Bad News Stories – Brazil Or Mexico?3 Things The Fed Needs To See Before It Starts Cutting Rates

Bank Of England To Use June Meeting To Lay The Ground For A Summer Rate Cut

Comments

Log in or sign up to join the conversation.