Image Source: Pixabay

People on the far left tend to overstate the extent to which all of the world’s problems are caused by nefarious US policies. On the other hand, I suspect that average Americans have no idea as to the extent to which the US bullies smaller nations. For instance, I hear people saying that foreign nations “take advantage” of the US in trade agreements, whereas exactly the opposite is true. We use our economic power to force trade concessions from smaller nations. And with respect to GDP at market prices, all nations are “smaller nations”.

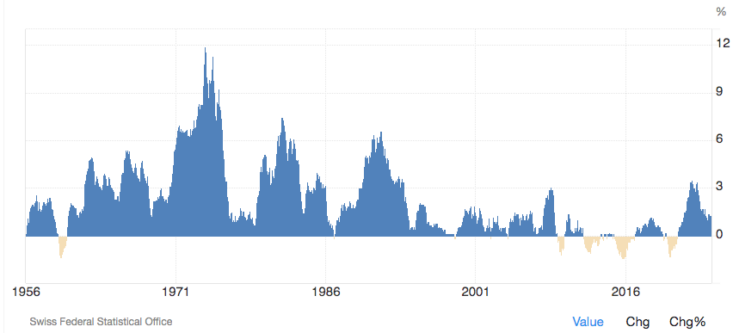

Over the past several decades, Switzerland has repeatedly slipped into deflation, partly as a result of a very strong currency. Here is Switzerland’s inflation rate from Trading Economics:

Because Switzerland has a relatively flexible economy, these brief periods of mild deflation have not caused great macroeconomic damage. Nonetheless, in order to prevent a slide into even deeper deflation, the Swiss National Bank has often been forced to cut interest rates to ultra-low levels, and do asset purchases (QE) that are many times larger than anything done in the US or EU. Here’s the Financial Times:

Serial central bank interventions persisted with the sale of freshly minted electronic Swiss francs in an effort to avoid the deflationary implications of steadfast currency strength. These interventions inflated the SNB’s balance sheet to a peak of around 140 per cent of GDP.

Back in 2022, the SNB suffered a loss equal to 17% of GDP when interest rates rose and bond prices fell. So why doesn’t the SNB adopt a monetary policy that would lead to a weaker currency, in order to avoid being forced to have ultra-low interest rates and an extremely bloated balance sheet? Part of the problem seems to be that the SNB misunderstands the fundamental cause of their dilemma (an issue I discuss in detail in my most recent book.) But one contributing factor is US government bullying, pressing Switzerland to strengthen the franc even further:

With rate cuts unlikely to move the dial, and capital controls unthinkable, the choice is between further intervention and genuine free float. In 2020 the US Treasury — rightly — labelled Switzerland a currency manipulator, putting diplomatic pressure on the SNB to desist.

Stop to think for a moment about the bizarre nature of this state of affairs. Over the past 50 years, no currency has been stronger than the Swiss franc. None. And how does the US government respond to this situation? By bullying Switzerland to make its currency even stronger.

When you’ve done something to an extent greater than any other country on Earth, and you are told that your problem is that you aren’t doing enough of that thing, that’s a telltale sign that you are receiving advice from people with a highly flawed model of the economy.

I frequently argue that low interest rates and big QE programs do not represent easy money, and that many conventional economists confuse cause and effect. But why should anyone believe my contrarian take?

Back in January 2015, I said Switzerland made a mistake when it allowed its currency to appreciate sharply, after successfully pegging it to the euro for more than three years. I suggested that this could push Switzerland back into deflation. Conventional economists suggested that this action was required in order to avoid a big increase in the SNB balance sheet. All of my fears proved true. Switzerland immediately slipped back into deflation, which led to a policy of negative interest rates. As investors perceived that the Swiss franc would likely appreciate against the euro, the demand for Swiss currency soared much higher. The SNB responded by expanding its balance sheet to 140% of GDP.

Switzerland is not the only country that the US has bullied into deflation. Our government also pressured the Japanese to strengthen the yen, with similar results.

PS. It’s interesting to look at some current account surpluses (for 2024), as a share of GDP (from The Economist magazine):

Singapore: 19.7% of GDP

Taiwan: 14.2% of GDP

Netherlands: 8.6% of GDP

Switzerland: 7.3% of GDP

Germany: 6.6% of GDP

Japan: 3.2% of GDP

Euro area: 3.1% of GDP

China: 1.2% of GDP

Which country has the smallest trade surplus of this group, as a share of GDP? Which country’s trade surplus is obsessed over by the US media? Which country has both political parties and much of the media labeled an enemy of the US? Notice a pattern? (The actual Chinese surplus may be somewhat larger than 1.2% of GDP due to measurement errors, but it’s still far below many other nations.)

More By This Author:

Should Monetary Policy Be Implemented By Economists?

Higher Taxes Or Lower Spending?

Immigration And The Business Cycle

Comments

Log in or sign up to join the conversation.