Last week, I was super happy because it finally was the week of Canadian banks Q3 earnings reports. Today, we’re starting with Scotiabank and BMO as they were the first to publish their results. Everybody was expecting that because banks have definitely set the tone for the Canadian economy.

Now, what’s going to happen with their dividend payment? I’ll tell you upfront, don’t expect anything out of the ordinary.

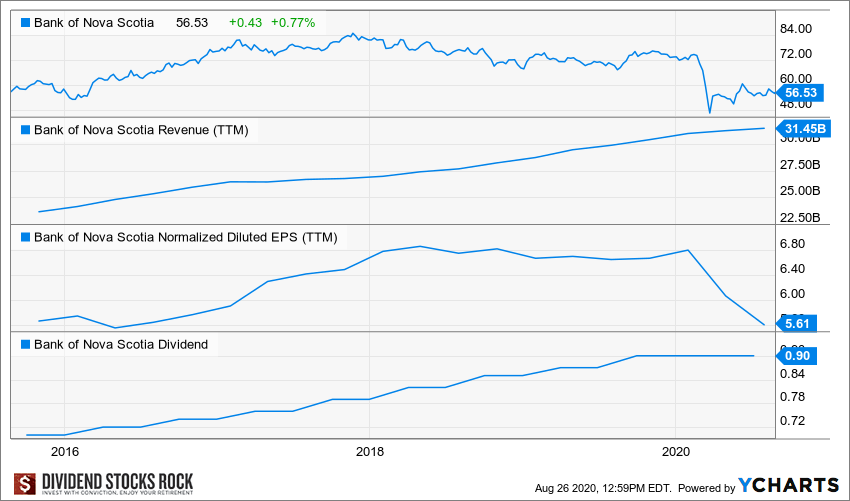

Scotiabank (BNS) (BNS.TO)

Business Model

The Bank of Nova Scotia is known as Canada’s “international bank” and is a global financial services provider. The bank has three business segments: Canadian banking, international banking, and global banking and markets. It is the third- largest bank in Canada. The bank’s international operations span numerous countries and are more concentrated in Central and South America. This is a strength other banks don’t have, especially when the Canadian economy is going through challenging periods.

What’s the Story?

“Scotiabank continues to focus on its customers while remaining operationally resilient during the COVID-19 pandemic. The Bank has strong capital and liquidity ratios and has reserved conservatively for estimated future loan losses. While our retail banking businesses in Canada and international markets were adversely impacted by the pandemic, the Bank’s performance was aided by strong results in Global Banking and Markets and Wealth Management. Focusing on our strategy and making prudent decisions that benefit all stakeholders – our shareholders, customers and employees – will result in a stronger Bank,” said Brian Porter, President and CEO of Scotiabank.

What Scotiabank CEO said is basically about the importance of having well diversified banks. I know that for my fellow American investors, a lot of regional banks are just focusing on savings and loans and those will have a hard time because interest rates are getting smaller and smaller. In other words, their margin is getting thinner, so it gets difficult for banks to improve their revenue. The only way they can do it is by increasing the amount of loans. Considering the pandemic, it also means increasing your level of risk.

In summary, the message could be read as follows: “We are a resilient bank, don’t worry about it, we’re gonna keep moving forward.”

Now let’s dig into the numbers.

- Net income -47%

- Adjusted EPS -45%

- CET ratio is at 11.3 (+40 points)

Obviously, this is because of higher provision for credit losses, about $2.2 billion. In comparison, last quarter, we were at 1.85; and at $700 million a year ago.

From their total loan of $636 billion, about 4% are subject to suffer from COVID-19:

- Energy field at 1.5%;

- Real estate office and retail at 1.3%;

- Travel, air transportation, hospitality and leisure at about 0.5-0.8%.

Overall, the sectors that will be hurt the hardest by COVID-19 are not really in Scotiabank loan portfolio.

Investment Thesis

BNS is the most innovative bank in the industry. It has done lots of business outside Canada and always with an open mind. BNS deserves its international label with 40% of its assets outside Canadian borders. This hasn’t always been an advantage as BNS ran into its share of problems with Latin American economic struggles. Expected GDP growth for these countries is quite interesting (a lot higher than Canada and the U.S.), but it comes with its load of uncertainties and volatility. BNS is now a dominant player in Chile with its most recent acquisition of BBVA Chile in 2018. Unfortunately, the way COVID-19 has been spreading across South America and Mexico is a source of concern. The dividend is safe, but it will be a long road to recovery for BNS.

Potential Risks

The bank ran into several challenges such as the situation in Venezuela. It seems that being present in emerging markets is not always a plus. Overall, diversification is a good strategy, but BNS’ international presence adds more volatility to its business model. We see how the pandemic effects this business segment right now. The bank must take higher provision for credit losses. Following the most recent events, BNS along with all other Canadian banks being watched. Their response to the crisis and how the Canadian government responds will have an important impact on their stock price. Expect lots of volatility until we know the economic impact of the virus.

Dividend Growth Perspective

Management usually offers two dividend increases per year. The total dividend growth per year is usually around 6%. This is quite interesting for any income-seeking investors considering BNS’ current yield. Unfortunately, we don’t expect any other dividend increase for any banks for 2020. After reviewing Q3 2020, we believe the dividend payment is safe. However, we have decreased its dividend safety score to 3 as the payout ratio is higher vs other banks like RY, BMO, and NA.

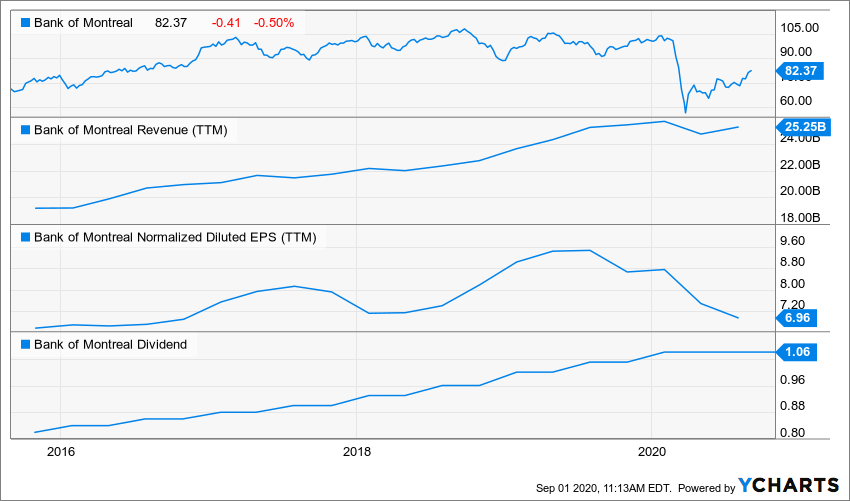

Bank of Montreal (BMO) (BMO.TO)

Business Model

Bank of Montreal is a diversified financial services provider based in North America. BMO conducts its business through three operating groups: Personal and Commercial Banking (P&C), Wealth Management and BMO Capital Markets. The bank’s operations are primarily in Canada, with a material portion also within the U.S. It has a strong presence in wealth management through Harris Bank.

What’s the Story?

“For the third quarter, we delivered very good results in a fluid environment, demonstrating the continued strength and resiliency of our diversified business model. We produced adjusted earnings per share of $1.85, strong pre-provision pre-tax earnings(1) of $2.6 billion, up 12% year-over-year, and provided prudently for loan losses and demonstrated capital strength,” said Darryl White, Chief Executive Officer, BMO Financial Group.

BMO CEO has a different tone. We’re talking about strength and resiliency. At the beginning, I liked the twist about the earnings were up by 12% if you exclude provision for credit losses. It’s kinda cute because if you’re in the business of lending money, you’re also in the business of losing some on bad loans. It’s just part of your business, don’t take those numbers apart.

The second part of his comment was quite interesting because he admits that the pandemic had a disruptive impact; that it was terrible for a lot of people but he’s already talking about being positioned for the next phase of the economic recovery. He’s already looking at how things will get better and that the economy is going to grow potentially in 2021.

You can see the difference of tones between a CEO that has a lot of business in Latin America that will not likely do well in the next 6-12 months, versus one whose business is focused in Canada and the US and has a strong position in capital market and wealth management.

Now let’s dig into the numbers.

- Net income -20%

- Adjusted EPS -22.3%

- CET ratio is at 11.6 (+60 points)

Provision for credit loss is $1 billion which is a lot of money. However, it’s less than what it was in April, which is great because it means they have done a good assessment… even though it’s three times what it was back in July last year. Nevertheless, I think it’s remained under control.

If you compare the loan book from Scotiabank to BMO, we see that this one has a little bit more exposure: about 5.1% on the COVID sensible sectors (hotels, restaurants, recreational and some parts of REITs). They can still continue to move on.

Finally the CT ratio is at 11.6, so similar to Scotiabank, it’s up 60 points versus April. Then again, good news, strong balance sheet there.

Investment Thesis

BMO decided to take the stock market path to ensure its growth. It was the first Canadian bank with its own ETF on the market. Competition is fierce but being among the first Canadian issuers surely helped to build momentum in a growing market. Over the years, BMO concentrated on developing its expertise in capital markets, wealth management, and the U.S. market. BMO also made innovative moves such as the introduction of its own ETFs and a robo-advisor. Growth will happen in these markets for banks in the upcoming years. BMO is well-positioned to surf this tailwind. When you can grab this bank with a 5% yield, you make a good deal.

Potential Risks

Relying on capital markets and wealth management as main growth vectors mean BMO can hit a speed bump. While their fact sheet shows an 8% CAGR over the past 15 years, BMO isn’t that generous anymore. After a pause of 3 years in its dividend growth policy, BMO started to grow its dividend again but lags its peers in that field. We don’t see any dividend increases in 2020 for Canadian banks. They must all deal with higher provisions for credit losses. While they are well capitalized, this also means banks will be less generous. As interest rates would be stable at best in 2020, the interest rate margin spread will tighten limiting the bank’s ability to generate higher profit.

Dividend Growth Perspective

BMO hasn’t been the most generous bank in terms of dividend growth lately. Maybe it’s cautious management as it also shows one of the lowest payout ratios and a healthy yield. In general, Canadian banks should appear on your radar each time they reach a 4% yield. We believe BMO’s dividend is safe for now (to be reviewed each quarter), but don’t expect any increase for the rest of 2020.

Final Thoughts

I believe Canadian banks’ dividens are safe for now. While I review my stocks each quarter, the pandemic forces us to look at earnings reports more closely. As stated above, Canadian banks should continue to thrive in the upcoming years, but investors should not expect much growth this year.

We all expect this big wave coming up from the virus, is it going to happen? Is it not? If you felt insecure while the market took its dive back in March, you might want to review your portfolio NOW.

The market has recovered, but the virus is still around, and its full economic impacts are still not fully known.

Comments

Log in or sign up to join the conversation.