Market Analysis

The USDA’s US/World S&D updates were mixed with this month’s US ending stocks going down in soybeans, up in corn and unchanged for wheat for their 2021/22 balance tables.

On the World stage, Ukrainian corn and Russian wheat were upped, Indian wheat was lowered & S American soybean output were upped slightly impacting both the US & World Balance sheets.

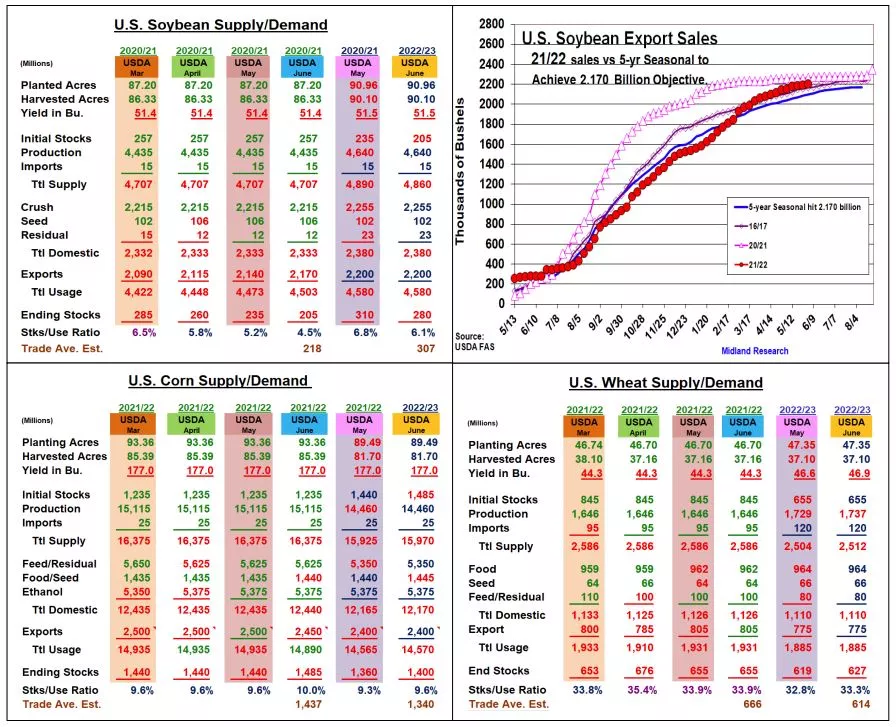

The USDA upped US soybean exports, but their increase was only 30 million bu, Interestingly, US export sales thru June 2 remain 33 million bu above the USDA’s 2.17 billion forecast & 106 million ahead of 5-yr seasonal. The USDA’s 2.3 mmt increase in S America’s crops & demand destruction cancelling sales or exports being rolled over into the 2022/23 US marketing year must be the DC assumption. No other US demand or 2022/23 balance sheet changes were made. This dropped old-crop stocks to 205 million, the lowest stocks/use level of 4.5% since 2013/14.

US corn exports were shaved by 50 million bu to 2.45 billion. Recent sales dipping below their 5-yr seasonal average pace seem to be the reason for this cut that upped US 2021/22 stocks to 1.485 billion bu. No changes in oldcrop feed while industrial use was increased 5 million bu. The USDA jumped Ukraine’s 2022 corn output by 5.5 mmt because a higher plantings. This upped world stocks to 310.5 mmt since Ukraine’s exports were left unchanged.

The USDA’s old-crop wheat balance sheet was left unchanged leaving stocks at 655 million bu, The Ag Department also kept their 2022/23 US demand levels steady with May. This month’s higher US W. wheat output was the surprise. A 12 million increase in white wheat up PNW countered a 8 million lower hard red crop in the Plains and 4 million higher soft red output in the Eastern US this month. Overall, this month’s 8 million rise in w. wheat to 1.182 billion, was the reason for new-crop’s increase in US stocks to 627 million. On the international side, India’s 2,5 mmt smaller crop to 106 was the reason that the world stocks stayed at 267 mmt, the lowest carryover since 2016/17.

What’s Ahead:

June’s USDA crop & supply/demand updates had some twists. However, the ongoing Black Sea conflict impact on its output & trade and US weather’s impact, which is heating up, on the US 2022 crop outputs remain highly important.

Still looking at halving old-crop bean supplies above $18 & increasing new-crop to 30-35% on Nov values above $16. Hold corn & wheat sales with June 30 acreage ahead.

Comments

Log in or sign up to join the conversation.