Bank Of England Set For Further Hikes Amid Inflation Concern

The Bank of England has hiked rates for a second consecutive meeting and we now expect further moves in March and May. But that might be more or less it.

There’s a growing sense that the UK is past the worst of Omicron. With the exception of young children, Covid-19 cases have decreased markedly from the peak and hospitalizations have fallen too. The UK has benefitted from comparatively high booster vaccine coverage in those age groups most vulnerable to severe disease.

All of this means that the economic damage from Omicron has been relatively contained, at least relative to past waves.

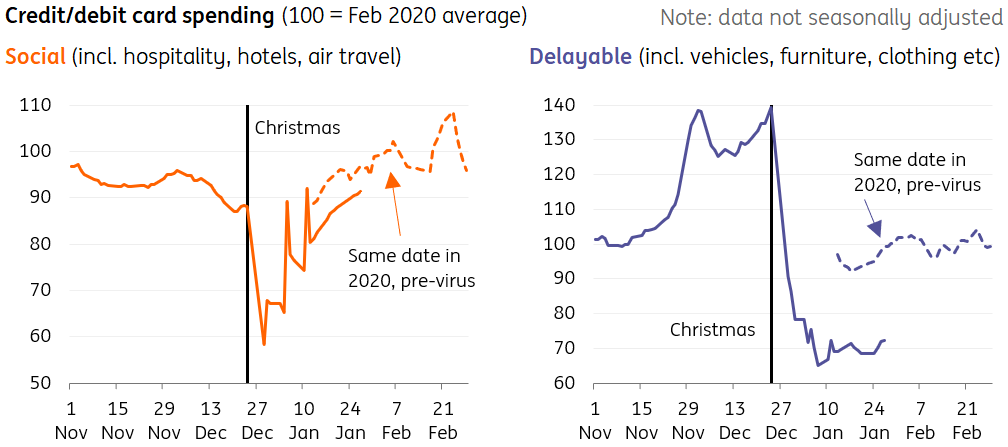

While consumers became decidedly more cautious in the run-up to Christmas – nervous about being in isolation during the festivities – they appear to have become more relaxed as January has progressed. Daily card data shows ‘social’ spending is tracking only slightly below levels seen in January 2020, before the pandemic.

Photo by simon frederick on Unsplash

The recent decline in Covid cases among adults and a recent shortening in self-isolation periods should also go some way to ease staff shortages. Absence rates in consumer services had topped 5% in early January.

In short, the total GDP impact of the latest wave, spread across December and January, is unlikely to top 1%, and most of this lost output will likely be regained within weeks.

Social spending is tracking only slightly below January 2020 levels

(Click on image to enlarge)

Macrobond, ING

Nevertheless, the pace of recovery is likely to slow as we move through the year. The combination of higher inflation and forthcoming tax rises means that real disposable incomes are set to continue falling, even when accounting for further gains in employment over the coming months.

That doesn't necessarily mean consumption will also decline and, to some extent, the excess savings built up through the pandemic, now amounting to roughly 8% of GDP, will help offset the income strain. In December, household deposits rose by their smallest amount since the start of the pandemic, a sign perhaps that consumers are now dipping into savings to sustain spending.

Slower consumption will also be partially offset by a decent year for business investment, having underperformed developed market peers consistently since the 2016 Brexit referendum.

Inflation the central concern for the Bank of England

At the Bank of England, the attention remains squarely on inflation.

Household energy costs are set to rise by roughly 50% in April, and a government-financed £200 discount in October will simply net out a further increase in the price cap forecast for the same month. This means inflation will peak close to 7% in the spring and end the year close to 3.5%. Concerns about headline inflation remaining higher-for-longer have prompted a second consecutive rate hike from the Bank – and in fact four out of nine policymakers voted for an even faster, 50bp move.

The Bank is clearly keen to act pre-emptively, and we now expect a further rate rise in both March and May. But that might more-or-less be it.

Elsewhere, the political drama in Downing Street is unlikely to change the economic policy outlook materially, even were there to be a change in leader. Nevertheless, these latest developments have meant Brexit has taken a back seat and fears of an imminent escalation in UK-EU tensions have subsided. Foreign Secretary Liz Truss has taken over negotiations and while the core disagreements don’t appear to have changed, the atmosphere has improved.

Disclaimer: This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information ...

more