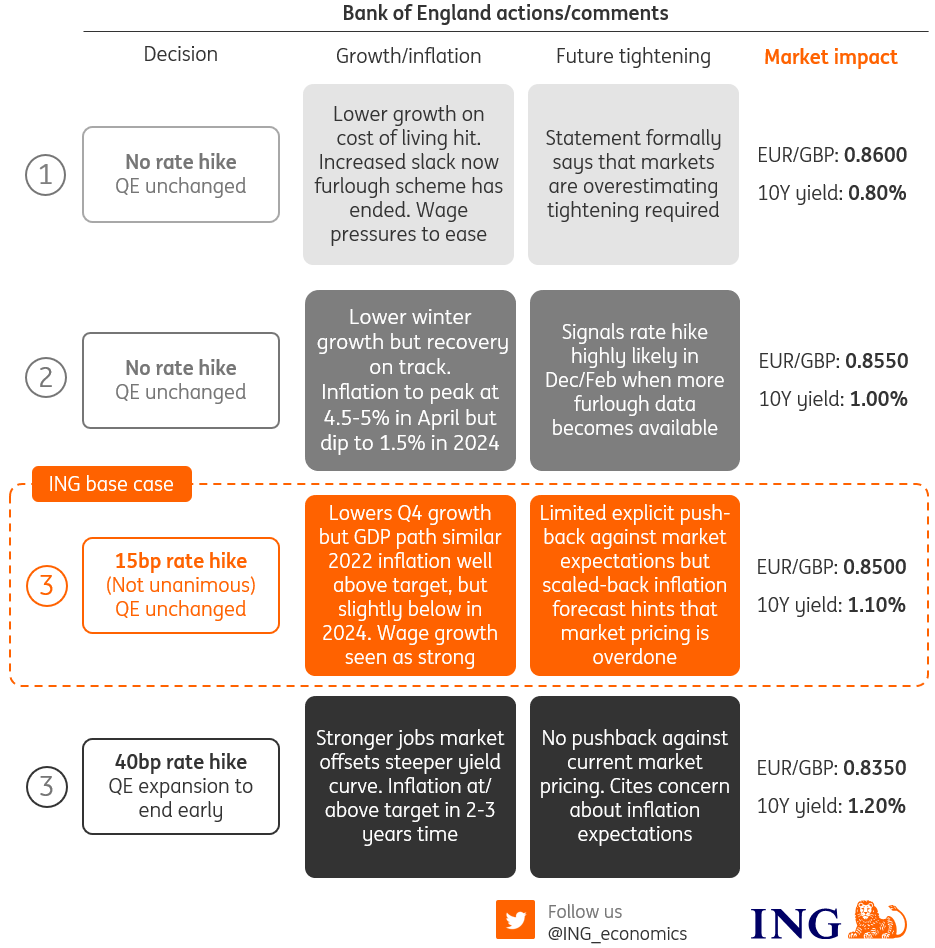

Bank Of England: Four Scenarios For The November Meeting

We expect a 15bp rate hike from the Bank of England next Thursday, following recent hawkish comments. But markets are overestimating the scale of future tightening, and we expect some modest pushback from policymakers in the form of lower medium-term inflation forecasts and a split rate hike vote.

Bank Of England, London

Four Bank of England scenarios for the November meeting

(Click on image to enlarge)

Source: ING

Expect a 15bp rate rise

Markets fully expect a 15bp rate hike at the November meeting, and they’re unlikely to be left disappointed.

Admittedly economists are more divided, and indeed until recently, we’d also assumed that the MPC would prefer to hold off on any rate rises until 2022. That would allow time to assess the impact of the recent ending of the furlough scheme, among other things.

But the recent message from Governor Andrew Bailey has been fairly blunt – he wants to act and sees little point in waiting. This has been epitomized by the lack of pushback against the ever-increasing amount of tightening priced into financial markets over recent weeks.

Waiting until December's meeting would buy time for more data to come through, but it would also mean that policymakers lack a post-meeting press conference or new forecasts to help explain their move to the public, something which the Bank takes seriously. If policymakers are keen to act, then Thursday's meeting seems like a better candidate.

Could the Bank increase rates by more than 15bp this time? Never say never, but it risks opening the floodgates for yet more additional tightening to be priced into financial markets.

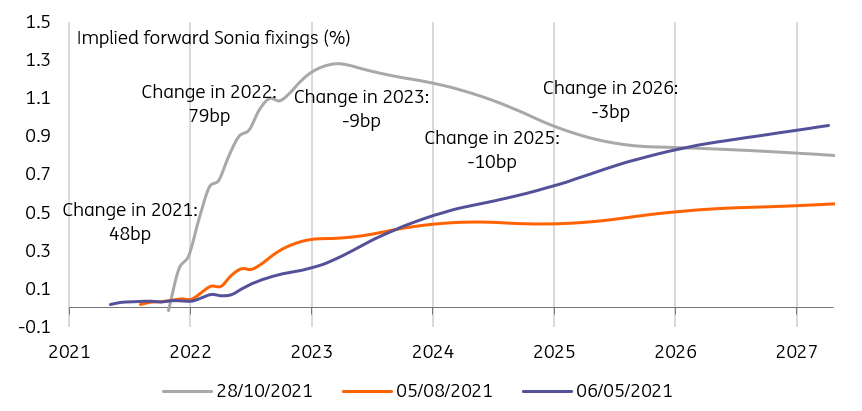

Markets are pricing a November hike, and plenty more besides

Source: Refinitiv, ING

Policymakers are likely to offer some modest pushback against the market's tightening expectations for 2022

That leads us neatly onto whether policymakers will attempt to lean more heavily against market pricing. We think they will, if only subtly.

There seems little doubt now that markets are overestimating the extent of tightening next year. Investors reckon rates will need to go to 1.25% or higher, which is both higher than at any point since the financial crisis, and above what’s priced for the US Federal Reserve, whose inflation challenge is arguably more acute. We expect at most one or maybe two rate rises next year (read why here).

Admittedly we might not get a great deal of explicit pushback in Thursday's policy statement, but there will be a number of clues elsewhere.

For one thing, if the committee does indeed opt to increase rates on Thursday, then it's unlikely to be a unanimous decision. While a handful of committee members will likely take Governor Bailey’s lead and vote for a rise, we know at least one member is likely to dissent (Silvana Tenreyro). This should be a warning sign for markets: if the first – partial – rate rise can’t command a unanimous decision, then it’s harder to see a series of aggressive, future moves gaining similar levels of support.

When it comes to the forecasts, we may well see a downgrade to the inflation projections for two/three years' time. Don't forget that the Bank takes market interest rates and plugs them into its models. Back in August, a modest 40bp of tightening over its forecast horizon neatly kept inflation around 2% in the medium-term. All else equal, the much higher degree of tightening now priced into markets should result in that 2024 inflation forecast moving lower.

If that happens, then it would be an implicit sign that policymakers don’t see a need to act as aggressively as the markets.

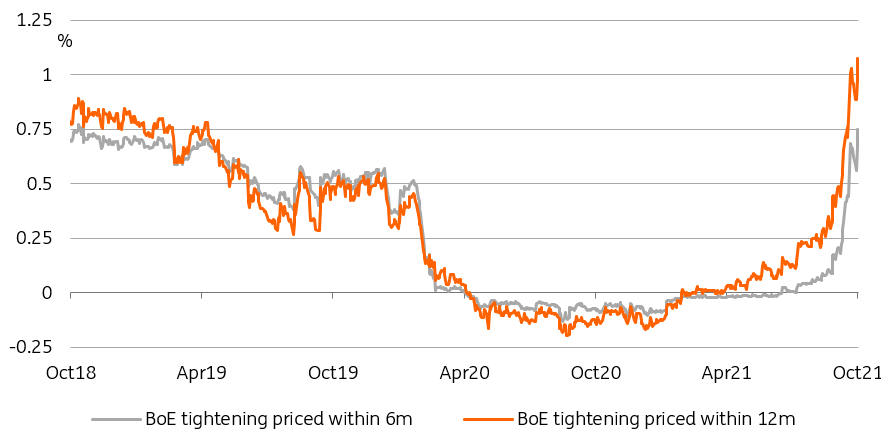

Hawkish BoE comments have seen markets dramatically revise rate hike expectations

Source: Refinitiv, ING

Market Rates: Balance sheet reduction to usher in era of greater volatility

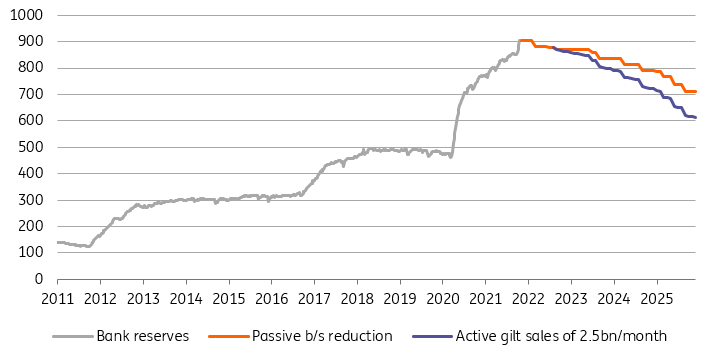

Another key question is whether policymakers offer up any more hints on its plans for its balance sheet. We don't expect policymakers to 'do a Bank of Canada' this Thursday and end its current quantitative easing (QE) programme early. Some of the hawks had been voting for exactly this over recent months, but the current scheme is slated to end in December anyway. And more importantly, it might not be long before the Bank starts putting the QE process into reverse.

Policymakers have said they will stop reinvesting the proceeds of maturing bonds from its QE portfolio when Bank Rate hits 0.5%. Markets expect that to happen as soon as February, and if they're right, the implication is that the £25b March 2022 gilt redemption will not be reinvested by the BoE into other gilts.

The same goes for the £3b July and £6b September redemptions later in the year, and for the £34b and £46b maturing in 2023 and 2024, respectively. The direct effect is that the amount of central bank liquidity, bank reserves, will go down by the same amount. Currently, they stand at £905b. In effect, this will add to upward pressure on money market rates and spreads.

The second less direct effect is that a substantial buyer, the BoE reinvesting its maturing bond holdings, will no longer show up in the gilt market to hoover up new issuance. This is only an indirect effect but a significant one as other types of investors will have to make up for the shortfall in demand. In all likelihood, they will request higher yields to do so. This demand shortfall needs to be put in the context of reduced supply however. At the UK’s autumn budget, the DMO updated its debt issuance forecast by £58b this fiscal year, and by £78b in the four subsequent years.

Another cause for concern is that once Bank Rate reaches 1%, the BoE could actively start selling gilts from its portfolio into the market. The effect on central bank liquidity is comparable as non-reinvestment: it will reduce bank reserves by the same amount. The impact on the gilt market is potentially more dramatic, as the BoE will compete with the Treasury to find buyers for their gilts. In normal times, small regular auctions could work fine. When market volatility picks up however, BoE sales will compound market worries.

The upshot is upward pressure on rates at both ends of the curve, and a higher volatility regime that should cause investors to demand higher compensation for buying sterling-denominated debt.

Possible paths for the Bank of England's balance sheet

Source: Bank of England, ING estimates

GBP: At risk of handing back some hard-won gains

GBP has undoubtedly benefited from the dramatic re-pricing of the UK money market curve since early September. However, the BoE’s broad, trade-weighted measure of GBP is up only 1.1% over the same period, so it seems fair to describe GBP gains as ‘hard-won’.

With a 15bp hike now fully-priced for the 4 November BoE meeting, we suspect that any concern over voting patterns (8-1 or 7-2?) plus some mild rate protest from the BoE through its 2-3 year CPI forecast could prompt a modest correction in GBP. BoE day event risk priced in the FX options market puts the cost of a EUR/GBP straddle at around 50 GBP pips. Based off the current spot near 0.8450, we think some modest disappointment – and a re-pricing lower of the 1.25% Bank Rate for late 2022 – could carry EUR/GBP to the 0.8500 area.

The sharp turn lower in gas prices would also seem to leave GBP a little vulnerable as the surge in late September and into October helped drive BoE tightening expectations higher and this factor is now reversing. Longer term, however, a BoE hike well ahead of the European Central Bank should see EUR/GBP rallies as short-lived. Into early 2022, we expect EUR/GBP to be trading below the 0.84 area.

Disclaimer: This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information ...

more