Headline inflation for June and the second quarter was in line with expectations and did not provide a good enough excuse for leaving rates unchanged in August, but there was some better news in the core numbers and the decision is now very finely balanced.

Some better news, but you have to search for it

If you were looking for reasons to argue against a rate hike at the forthcoming Reserve Bank of Australia (RBA) rate-setting meeting on 6 August, the core figures in today's release provide some, though fairly limited ammunition.

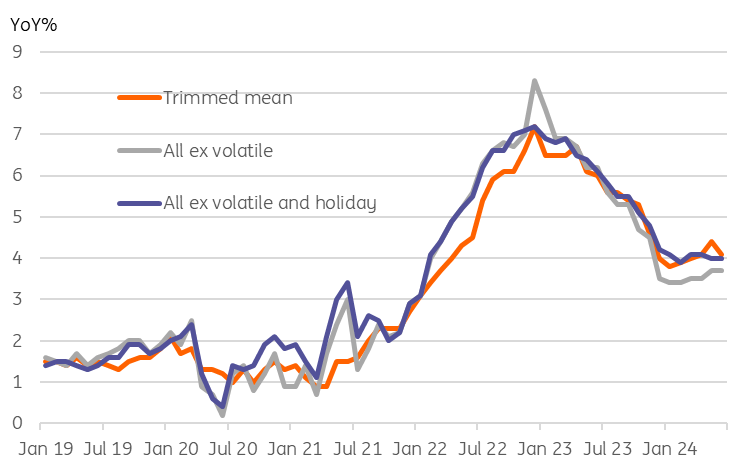

The 2Q24 trimmed-mean CPI rose by 0.8% QoQ, less than the 1.0% expected, resulting in this core measure of inflation dropping 0.1pp to 3.9%YoY.

The weighted median - another core measure - also rose 0.8% QoQ, and helped that core measure of inflation rate to drop from 4.4% to 4.1%.

The core monthly data, however, show far less of an inclination to decline, with two out of the three inflation measures in the chart below remaining unchanged from the previous month.

Monthly core inflation measures

Headline inflation measures are still quite high

That is about the limit of the good news, as the headline measures for inflation for June and the second quarter were in line with expectations. Headline inflation rose 1.0% QoQ, taking the 2Q24 inflation rate up to 3.8% YoY from 3.6% in the first quarter. June inflation dipped slightly to 3.8%YoY. But this was in line with expectations and mainly a base-driven result.

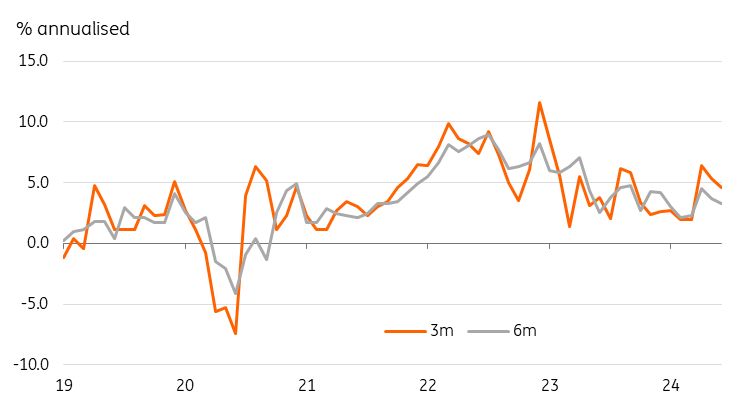

The implied month-on-month increase was 0.53% - it needs to come in at about half that on average to ensure that inflation comes in under the top of the RBA's 2-3% target range, and annualised inflation is running somewhere between 4.6% and 3.3% on 3m and 6m measures. This is coming down erratically, though it is still too high and the low 6m figure will likely move higher again next month in the absence of a sharp CPI fall as the negative January figure will drop out.

Annualized inflation is still high

So what does this mean for the RBA?

If you wanted to find a reason to leave rates unchanged at the 6 August meeting, there is some support in the core numbers published today to say, "Let's give the economy the benefit of the doubt". The August decision is certainly more finely balanced today than it was yesterday.

However, for us, the evidence to suggest that inflation, even if it is trending lower (debatable) is doing so too slowly is more compelling. Add to that, another strong retail sales figure for June (0.5% MoM after the 0.6% May figure) and you get a picture where domestic demand is holding up too well to allow for a satisfactory decline in inflation to the RBA's target range over the medium term. We still favour a 25bp rate hike on 6 August to take the cash rate target to 4.6%.

The initial market response to today's data was for the AUD to weaken sharply, most likely due to the core inflation figures. Markets, which had been pricing about a 25% chance of an August hike priced it back out again. This seems like an overreaction to today's figures, but maybe if the market is not pricing in a hike, the RBA will be less willing to surprise them...? We'll know soon enough.

More By This Author:

Rates Spark: Buffeted By Ongoing Sequence Of Macro DataAsia Morning Bites For Wednesday, July 31

Eurozone GDP Beats Expectations But Remains Weak Behind The Scenes

Comments

Log in or sign up to join the conversation.