Image Source: Pexels

Further moderation of growth should support the idea that the restrictive rates policy is working and that further hikes are unnecessary - all we now need is for inflation to fall...

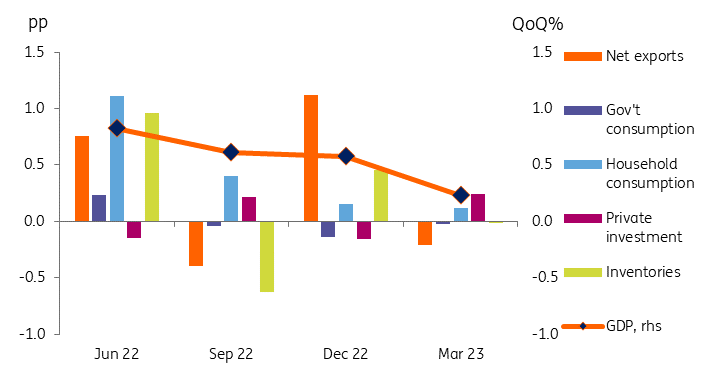

GDP growth slows again

GDP growth in Australia has been slowing since 2Q22 when the reopening of the economy temporarily lifted economic activity dramatically. Since then, the Reserve Bank of Australia (RBA) has been engaged in a battle to try to squeeze rampant inflation out of the economy, while simultaneously trying to avoid tipping the economy into a sharp recession. So far, this seems to be working.

Following a 0.2% quarter-on-quarter increase, the annual growth rate in 1Q23 has slowed to 2.3% year-on-year from 2.6% in 4Q22, and we expect it to slow further. Household consumption has driven the decline in growth, with occasional fluctuations from inventories or net exports adding volatility. But the key observation in the latest set of data is that really nothing, including business investment, is picking up the slack from consumption. There are no obvious factors in the pipeline that could lift the numbers in the coming quarters. So growth will probably slow a little further, or at best pootle along at similar low growth rates over the next couple of quarters. That means that full-year GDP growth should come in at about 1.7% according to our latest calculations, though probably a little lower rather than higher if we consider the balance of risks.

Contribution to QoQ GDP growth (pp)

Image Source: CEIC, ING

If it's slowing, then the RBA policy must be working...

While no one wants to see the economy drifting into recession, the slowdown we are seeing is evidence that the RBA's tightening (which they added to earlier this week taking the cash rate target to 4.1%), is working.

Admittedly, the labor market has yet to show much evidence that it is also cooling sufficiently to help bring wage growth and hence service sector inflation back to a more manageable growth rate. And headline and core measures of consumer inflation are also taking their time to drop back to an acceptable rate. But today's numbers do add ammunition to the view that current policy is working. These other, lagging indicators should fall into line, given time and a little patience.

All of this suggests to us that the current cash rate is probably high enough and that market expectations for further tightening may be a bit overdone. A more rapid rate of inflation decline in the coming months should help support our view.

More By This Author:

Rates Spark: Enough Out There To Nudge Market Rates HigherThe Commodities Feed: China’s Imports Recover

FX Daily: A Close Call On The Bank Of Canada Today

Comments

Log in or sign up to join the conversation.